Uran Forum

1. https://x.com/baelde_jonas/status/1886120532833112539

2. https://x.com/UraniumFrank13/status/1888291097199390758

die doppelte Menge zu durchschn. ca. 0,32 Euro gekauft. Dafür ist mein gehebelter SPUT tiefrot ....

Optionen

| Boardmail an "Armasar" |

Wertpapier: Kazatomprom GDR |

Optionen

| Boardmail an "grafikkunst" |

Wertpapier: Kazatomprom GDR |

aktuellen spotprice Schwäche:

I’m very bullish on uranium... but I must admit that there’s a new wrinkle in the story. No, I’m not worried about reports of a Russian drone hitting the Chernobyl containment dome. It’s the possibility that Trump might set up a new “Megatons to Megawatts” program. He’s just said: “President Putin and I agreed that we were going to do it in a very big way. There's no reason for us to be building brand-new nuclear weapons. We already have so many, you could destroy the world 50 times over, 100 times over. And here we are building new nuclear weapons.” Maybe this is just talk, but the truth is that spot uranium has now fallen lower than I thought it would.

I’m still inclined to see this as an opportunity. But… if a significant amount of weapons-grade uranium is down-blended to create reactor fuel, it would create a new source of secondary supply. This too may be something uranium bulls may not want to hear—but you know what my job is. I’ll need to see what the potential scale is here before I can work this into my model. It may not even happen. But it’s something I’ll be watching closely.

Why is spot down so much if nothing has changed? There are reports that fewer Japanese reactor restarts are bringing more secondary supply to market. I think this is unlikely, even if there are fewer restarts. More likely, in my mind, is companies that bought uranium while it was cheap in order to finance mine construction selling to the spot market to do just that. If so, we will see this documented in future filings.

Optionen

| Boardmail an "zazul" |

Wertpapier: Kazatomprom GDR |

fazit:

rahmenbedingungen bleiben auf lange sicht in takt.

keine panik.

wir bleiben looooooooooooong... ;-)

Optionen

| Boardmail an "zazul" |

Wertpapier: Kazatomprom GDR |

https://www.youtube.com/watch?v=RIE7ruhidus

Optionen

| Boardmail an "zazul" |

Wertpapier: Kazatomprom GDR |

In line with Cameco comments on the topic and general consensus in the sector - very little is likely to materially change. That said, I won’t even guess what investor sentiment would do or how under-informed speculators will behave.

So let’s go over why very little would be likely to materially change:

1. The Prohibiting Russian Uranium Imports Law is not a “Sanction” it cannot be lifted by Executive Order — it would require Congressional repeal of a law that passed with unanimous bipartisan support. A law designed to force the restart of a domestic nuclear fuel supply chain. Passage of that law was required to unlock $3.4B in funds for building and expanding domestic production of LEU and HALEU. It is extremely unlikely that this law is repealed because ending dependence on Russian conversion & enrichment is a national security priority, and a national energy priority (reinforced under Wright’s DoE.) Also, the funds have already been awarded and in the case of both Orano & Urenco - have been met with billions in additional private spending commitments (along w lesser amounts by other vendors eg $60m from Centrus.) And, a reminder, this law prohibits all Russian Uranium Imports as of 12-31-27 even if the fuel buyer is holding one of the five Waivers issued by DoE.

2. Russia’s retaliatory “Temporary Export Ban” is Russian “policy” or counter-sanction (not law) that is set to last through 12-31-25 (and then be subject to renewal) but it could potentially be lifted (or export licenses issued) however, only Waiver holders would be eligible to order material. Now, this is where timing matters: There are only 22 months left until the Import Ban fully kicks-in. How many more months go by until peace is negotiated — if it is at all? The point is that even if Russia is inclined to encourage orders (post war) the window for turnaround shipments is ticking toward closure.

3. In my opinion, even Waiver holders are no longer holding out hope of receiving Russian EUP in the wake of multiple sailings from St. Petersburg that did not contain material. As such, alternative vendors are being contracted - as evidenced by soaring prices for Conversion and Enrichment Services since Nov ‘24.

In the big picture, the requirement for Uranium U3O8, (the feedstock for Enrichment Services) is a worldwide calculation — no matter who performs the Services. As such, the structural supply deficit (inadequate to fuel existing reactors - never mind new demand) hasn’t changed, it was only been temporarily delayed by a year of uncertainties around the likely permanent disruption of a 30-year method of procurement."

https://x.com/leggett_john/status/1892640846811394303

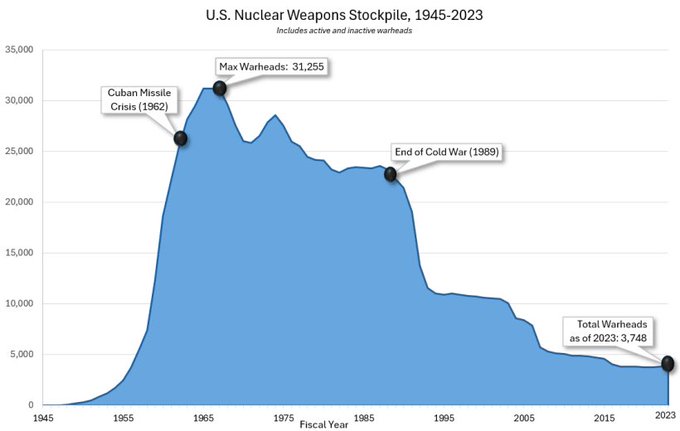

Using chatGPT, cause I’m lazy, ~39Mlbs from the prior megatons to megawatts came from 20,000 warheads.

We’re not at that same level as before. Bring on nuclear disarmament"

https://x.com/UraniumTails/status/1890571828764020942

"Based off the figures on centrus website and at ratio of 8 to 1 natural to leu

20,000 warheads equals 248 million lbs of uranium, it took 18 yrs to complete the program so that's less 14million lbs a year at $870 per lb leu in 2014 dollars"

Angehängte Grafik:

gjypdzhxcaanxtf.jpg (verkleinert auf 75%)

gjypdzhxcaanxtf.jpg (verkleinert auf 75%)

Neither of those is in the current supply/ demand projections."

"US military uranium stockpiles are at/near historical lows. Warheads downblended already feed the HEU needs of the nuclear navy, which consumes ~5+mlbs/yr. The below take is right on, IMO"

https://x.com/uraniuminsider/status/1890498182825541868

"We have and I can tell you, the spot market is not where utilities go to meet their annual run raterequirements. It's completely discretionary and its non-fundamental. Of the 46 million pounds ofuranium that transacted in the spot market last year, only about 15% was bought by utilities. As isthe case every year, a great deal of the spot activity was churn.

Traders, brokers and financial players passing around 100 000 pounds 5 times, which becomes 500 000 pounds of reported volume, that's not a reliable source of supply for the more than 175 million pounds a year needed to fuel the global nuclear fleet annually. And that's not a source ofsupply that can underpin the long-term operation of a nuclear reactor for 60 or more years.Instead, utilities are buying uranium and the fuel cycle services in the long-term market, yearsahead of time, sometimes even for the decade to come or longer. "

https://www.youtube.com/watch?v=ZEXPp_0Qm9Q

https://www.kitco.com/news/off-the-wire/...-if-trumps-tariffs-go-play

Das wird wohl nix mit den AI-Reaktoren. Wenn man dran kommt - es schlägt nun wohl die Stunde für NorNickel, die dürften dieses Jahr weitere 30% steigen. Cameco dürfte hingegen um weitere 30% fallen. Das Ziel der Abwärtsbewegung bei Uran dürfte $50/lb sein.

Optionen

| Boardmail an "Armasar" |

Wertpapier: Kazatomprom GDR |

https://www.chita.ru/text/incidents/2025/02/25/75149675/

Optionen

| Boardmail an "grafikkunst" |

Wertpapier: Kazatomprom GDR |

Link: https://www.youtube.com/@axinocapital/streams

Optionen

| Boardmail an "grafikkunst" |

Wertpapier: Kazatomprom GDR |

Encore:

Financial Highlights for Fiscal Year 2024 and Future Outlook:

Revenue: enCore reported total revenue of $58 million, reflecting a 163 percent increase from the year ended December 31, 2023, primarily due to increased uranium extraction. In 2024, sales were made from a combination of extracted and purchased pounds, while in 2023 all sales were from purchased pounds.

Earnings Per Share: The Company recorded a loss per share of $0.34 for the year ended December 31, 2024, compared to a loss of $0.18 per share for the year ended December 31, 2023, the increase being primarily due to:

https://encoreuranium.com/news/...d-files-annual-report-on-form-10-k/

Optionen

| Boardmail an "Bozkaschi" |

Wertpapier: Kazatomprom GDR |

Angehängte Grafik:

img_3633.jpeg (verkleinert auf 39%)

img_3633.jpeg (verkleinert auf 39%)

OK, sie stellen also ihre Rechnungslegungsmethode auf die US-GAAP-Anforderungen um, aber einige Investoren haben nicht bedacht, wie sich das auf ihren Nettoverlust auswirkt. Hier ist eine Passage aus der oben genannten Pressemitteilung, die diesen Punkt aufschlüsselt:

„Das Unternehmen meldete für das am 31. Dezember 2024 zu Ende gegangene Geschäftsjahr einen Nettoverlust von 61,3 Mio. $, verglichen mit einem Nettoverlust von 25,6 Mio. $ für das am 31. Dezember 2023 zu Ende gegangene Geschäftsjahr. Die Unfähigkeit, bestimmte Explorations- und Entwicklungskosten nach US-GAAP zu aktivieren, die nach IFRS aktiviert worden wären, wirkte sich auf beide Jahre aus und belief sich auf 15 Mio. $ für 2024 und 8 Mio. $ für 2023.“

Das ist also ein hässlicher Nettoverlust von 61,3 Millionen Dollar für 2024, egal wie man es betrachtet. Wären jedoch 15 Millionen Dollar weggefallen, wäre der Verlust mit 46,3 Millionen Dollar etwas weniger hässlich gewesen. Diese Änderung der Rechnungslegungsmethode wurde vom Markt nicht vollständig verstanden.

excelsiorprosperity@substack.com

Optionen

| Boardmail an "grafikkunst" |

Wertpapier: Kazatomprom GDR |

„enCore konzentriert sich auf die Installation von Bohrlochmustern, um die Uranförderung in Südtexas zu erweitern. Seit Anfang 2024 hat das Unternehmen die Anzahl der in Südtexas tätigen Bohranlagen auf 17 erhöht. Die erhöhte Anzahl an Bohranlagen wird Engpässe bei der Erneuerung von Bohrlochmustern, die zu Beginn des Jahres beobachtet wurden und die Ausweitung der Urangewinnung verzögerten, ausgleichen. Das Upper Spring Creek Projekt wird nach der endgültigen Genehmigung, die für 2025 erwartet wird, uranhaltiges Harz für das Rosita CPP liefern.“

In diesem Teil der Nachricht wird beschrieben, dass das Unternehmen einen Plan zur Ausweitung der Produktion und zum Abbau von Engpässen hat. Sobald die Genehmigungen erteilt sind, wird das Unternehmen auch in der Lage sein, die Produktion in Rosita zu steigern. Dies sind Gründe für die Annahme, dass die Bilanz für 2025 besser ausfallen wird als die für 2024. Wenn den Anlegern also das Wertversprechen von enCore Energy im letzten Jahr gefallen hat, dann ist das Unternehmen für das kommende Jahr nur noch attraktiver geworden, da die Bewertung gesunken ist.

„Am 2. März 2025 ernannte das Board of Directors von enCore Robert Willette, den derzeitigen Chief Legal Officer, mit sofortiger Wirkung zum amtierenden Chief Executive Officer. Herr Willette tritt die Nachfolge von Paul Goranson an, der nicht mehr als Chief Executive Officer von enCore oder als Mitglied des Board of Directors tätig ist.“

Diese Nachricht, dass Paul Goranson nicht mehr CEO ist, hat den Markt heute wirklich schockiert und überrascht. Dies wurde nur kurz weiter unten in der Pressemitteilung erwähnt, ging aber im Trubel der Uranschmerzen und Gründe für den heutigen Verkauf von U-Aktien nicht unter. Die Leute kamen vorschnell zu dem Schluss, dass es Probleme im Paradies gab, und vielleicht gab es persönliche Konflikte oder unterschiedliche Vorstellungen über das weitere Vorgehen zwischen dem Vorstand und dem CEO. So etwas kommt in vielen börsennotierten Unternehmen vor und wird in der Regel gelöst, wenn der Vorstand kompetent ist, was meiner Meinung nach bei enCore der Fall ist.

Ich persönlich habe großes Vertrauen in Willam (Bill) Sherriff, der als Executive Chairman das Ruder übernommen hat. Ich habe ihn jetzt schon mehrmals persönlich auf Ressourcenkongressen getroffen und ihn auch in unserer KE Report Show zu Interviews eingeladen. Bill ist eine Klasse für sich, ein direkter Schütze, offen und brutal ehrlich.

Optionen

| Boardmail an "grafikkunst" |

Wertpapier: Kazatomprom GDR |

Optionen

| Boardmail an "grafikkunst" |

Wertpapier: Kazatomprom GDR |