Steinhoff Informationsforum

Die Profis verkaufen ihre Leerpositionen (oder aus Bestand) schon während des leichten Anstiegs.

Gerne so 1-3 Mio Stück. Dann wird der Kurs leicht hochgekauft und dann gedrückt, damit sich die Durchschnittslinien nach unten kreuzen. Die Algos verkaufen dann automatisch...

Optionen

| Boardmail an "Shoppinguin" |

Wertpapier: Steinhoff International |

Also von mir mein Respekt an ihn. Und bitte verkaufe bloss deine Aktien nicht auf einmal sonst ist der Kurs wiedet bei 5cent LACH

Aber eine Frage umtreibt mich doch :

Ich habe hier vor ca. 2,5 Jahren über 40 Millionen Steinhoffaktien für 4,5 Cent in Blöcken a 900.000,- eingekauft. Wieder und immer wieder !

Über 4 bis 5 Tage lang. Diese Kauforder wurden allesamt in kürzester Zeit bedient, ohne dass es auch nur den geringsten Kursausschlag gab.

Die Erklärung ist dazu für mich relativ einfach : Das sind Profileerverkäufer ( hallo Ryte ) am Werk gewesen, die dachten, dass Steinhoff pleite

gehen würde, und sie diese Aktien letztendlich für einen Cent beispielsweise zurückkaufen könnten. Wäre ja auch ein super Geschäft gewesen.

Wie gesagt : WÄRE !

Aber : Hätte hätte, Fahrradkette. Die Frage ist doch jetzt ? Wann müssen diese Leerverkäufer sich wieder eindecken, oder ist dies bereits schon

passiert ?

Es gibt ein schönes Sprichwort : Unter jedem Dach steckt ein ...Ach... Und so hat jeder Mensch halt sein Päckchen zu tragen.

Ich finde es persönlich nur schlecht, dass hier die ängstichen und Neuaktionäre einfach nur durch irgendwelche komischen bezahlten

Schreiberlinge, die immer gerade dann EXAKT ! auftauchen, wenn es hier um die Wurst geht, und die Kurse in ihre Richtung zu drehen.

Und nein, dass ist ganz sicherlich kein Zufall. Wer das glaubt, der glaubt auch noch an den Weihnachtsmann.

Ich vermute, daß es in Südafrika erst ein paar Leerverkäufer und dann ein paar Banken zerlegen wird.

Mit großer Stückzahl leer zu gehen schien damals ja auch eine ziemlich sichere Sache zu sein; wenn man dann noch die wiederholten Warnungen der (südafrikanischen) Börsenaufsicht bezüglich ungedeckter Leerverkäufe bedenkt, ist die Sache für mich eindeutig.

Das zu beweisen ist allerdings unmöglich.

Moderation

Zeitpunkt: 26.01.22 19:27

Aktionen: Löschung des Beitrages, Nutzer-Sperre für 1 Tag

Kommentar: Beleidigung

Zeitpunkt: 26.01.22 19:27

Aktionen: Löschung des Beitrages, Nutzer-Sperre für 1 Tag

Kommentar: Beleidigung

Bin ja da bei zwei anderen Stocks schon eine harte Sau geworden, aber jetzt auch beim Steini?

Gibt es dazu Zahlen und auch, wer den Short ist?`

Frage für einen Freund meines Nachbarn ;-)

Optionen

| Boardmail an "Bauchlauscher" |

Wertpapier: Steinhoff International |

Identifying the swathe of losers and the sliver of winners in the Steinhoff debacle

Louis du Preez, the current CEO of Steinhoff. (Photo: Dwayne Senior / Bloomberg via Getty Images)

Not to fall too deeply into an old cliche, but for Steinhoff the decision of the Western Cape High Court to approve its settlement plan on Monday constitutes the end of the beginning.

So, the past is now the past, the water is under the bridge, and the spilt milk has been incontrovertibly and fundamentally spilt. We can now, with much more certainty than ever before, count the cost.

It almost goes without saying that the biggest losers were the shareholding public of South Africa. There is a common misconception that only rich people own shares, but almost everybody who has a pension fund owns shares. And almost everybody who owned shares, owned Steinhoff.

https://www.dailymaverick.co.za/article/...-in-the-steinhoff-debacle/

In his book Steinheist, Financial Mail editor Rob Rose records the fact that of SA’s 1,651 pension funds, 948 had Steinhoff shares in their portfolios.

Steinhoff’s peak share price was R96.94 in April 2016. Two years later, it was R1.12. On Tuesday, it closed trading at R4.43. At its peak, the company was worth R355-billion – just before the collapse in December 2017, it was worth about R240-billion.

At its low point, which has lasted four long years now, it has been trading between R3-billion and R8-billion.

So, generously speaking, the cost to the ordinary shareholder was about R230-billion. That is a staggering sum. Yet, recently, there has been a turnaround as punters speculated that the legal process would unfold happily – and it has.

Steinhoff now has a market value of about R20-billion.

What about the settlement offer? The Cape Town court approved the company’s R24-billion settlement offer, a massive reduction on the R180-billion originally claimed. This difference is really a feather in the cap of current CEO Louis du Preez. To convince shareholders to take 13c in the rand must have taken some doing, but in this situation, the tug of war between what shareholders want and what the company can afford was always going to be a tough battle.

So, although shareholders were the biggest losers numerically, both in quantity and value, they were by no means the only losers. Obviously, the senior management of the company, most notably former CEO Markus Jooste, lost their life savings, their reputations and, in due course, may also lose their freedom – although that remains to be seen.

Who else lost? Deloitte, the auditors at the time of the collapse, and, ironically, the auditors to have first questioned the company’s finances, have paid in R1.2-billion, not, it should be noted, for auditing failures, but to help the company settle claims against it. Neat, that.

But there are two other much less obvious, and much more consequential, losers.

The first is South Africa Inc. It may not seem like it, but every SA corporate scandal hurts every South African – not in any abstract way, but concretely. The reason has to do with the calculation of business risk.

It’s simple really. Investors in equities logically require a return over and above what they would get from a riskless asset. There are none of those, sadly, but the closest you can get to it is the return on a 10-year maturity government bond which, in SA’s case, is currently about 9%. Subtract that from a company’s expected earnings growth, or alternately its dividend growth, and you get close to a measure of what return you need to invest successfully.

But there is one other variable, which is, well… very variable, and that is the risk premium. This constitutes the extra compensation investors need in order to invest to compensate them for the risk they are taking. Normally, this varies between 1% and 2% in developed countries to almost anything. But in SA’s case, it’s probably about 5% currently. So, all in, you likely need a return of at least 14% to invest in SA – and that is a pretty high bar.

Every time a corporate scandal happens, the risk premium rises. You can see this very visibly by comparing the average price:earnings ratio of different stock exchanges around the world.

Developed markets tend to have much higher average ratios than developing markets, and one of the big reasons is the risk ratio. It’s one of the reasons SA companies are so desperate to list outside SA; it helps them minimise the risk premium.

The effect of an increase to the risk premium is that it increases the cost of capital, which affects the quantity of investment, which affects the level of business confidence, which affects the cost of capital… and so it goes on.

Successful countries manage this spiral upwards; unsuccessful countries pay the price in lower employment levels and less wealth generation for a spiral downwards. Hello, South Africa.

How much has Steinhoff added to SA’s overall risk premium? Probably not much. Corporate scandals happen everywhere, and all countries can sustain a few. The Enron scandal did practically nothing to the US’s risk premium, and the Wirecard scandal in Germany will probably have little effect. But corporate scandals count for more in developing countries. And if they happen often, the damage is exponentially larger.

There is one other loser, pointed out to me by fellow journalist The Finance Ghost. One of the costs of the Steinhoff saga is that companies that were growing by acquisition have really struggled in its wake. Perhaps the best example here is Long4Life, the company founded by acquisition growth maestro Brian Joffe.

“In the immediate aftermath of the Steinhoff bubble bursting, it was almost impossible for listed groups to do deals other than for cash. Entrepreneurs watched in horror as the Tekkie Town sellers saw the value of their life’s work destroyed. This drove unwinding valuation multiples among highly acquisitive groups who found themselves struggling to grow.

“In turn, this made it less attractive to raise cash in the market to do deals, further compounding the problem. Issues at the likes of EOH and Ascendis made the risks of share-for-share deals even more apparent to entrepreneurs. The loser, overall, has been the market and its participants,” he says.

The problem is that the growth by acquisition strategy is underpinned by the takeoveror offering shares as opposed to cash for the acquisition. If sellers of medium-sized or even smaller companies don’t want to take shares, the only option for buyers is to use cash. And in a high interest rate environment, that is a tough ask.

The doubt injected into the system by the Steinhoff disaster and associated events has really made it hard for buyers. This then hurts the stock exchange, which in turn makes sellers even less keen to take equity in a sale – and so it goes around.

Successful countries manage this spiral upwards; unsuccessful countries pay the price in lower employment levels and less wealth generation for a spiral downwards. Hello, South Africa.

What about winners in the Steinhoff saga? As one lawyer said, the Steinhoff saga has been responsible for the largest movement in history of capital from Stellenbosch to Johannesburg. So, there is that.

Obviously, buyers who took a punt on Steinhoff getting to grips with its legal problems over the past few months have made a tidy packet, more than doubling their money.

What about Steinhoff as a company, its staff, its suppliers and so on? They have emerged on the other side of this disaster, bruised and somewhat worse for wear, but still standing – and there is an enormous virtue in that.

Yet, their future remains uncertain. Survival is one thing, growth is another. But that is an entirely different story. BM/DM

https://www.dailymaverick.co.za/article/...-in-the-steinhoff-debacle/

Optionen

| Boardmail an "silverfreaky" |

Wertpapier: Steinhoff International |

Die große Unbekannte liegt in Südafrika - keine Zahlen *und* es gab (gibt?) die Möglichkeit, ungedeckt leer zu verkaufen. Da könnten ungedeckte Verkäufe von hunderten Millionen Aktien oder noch mehr schlummern. Die Aktie wurde über einen sehr langen Zeitraum in einem niedrigen Bereich ohne Schwankungen gehalten. Martin konnte große Stückzahlen ohne Einfluß auf den Kurs kaufen - entweder, jemand hat sich von seinem großen Bestand getrennt, oder es wurden permanent Aktien aus dem Nichts erschaffen und "nachgefüttert", um den Kurs vollends abstürzen zu lassen (das wäre dann wohl für die LV die einzige Möglichkeit gewesen, ohne aufzufliegen aus den ungedeckten Leerverkäufen herauszukommen).

Aber: Das sind alles Vermutungen, *beweisen* kann ich davon nichts.

Also auch wie so überall in der Grauzone oder einfach nur Beschiss am Privatanleger.

Aber dann binich ja mit Halten udn wenn ich will nachkaufen genau richtig hier :-)

Bleibt geschmeidig.

Optionen

| Boardmail an "Bauchlauscher" |

Wertpapier: Steinhoff International |

4 Millionen Shares.

Wie schaffen die das nur, der Kurs sinkt und die kaufen täglich Millionen Shares ein.

Die müssten doch eigentlich in festen Händen sein!

Und vom täglichen Umsatz verschwinden!

Oder werden die doch zum LV verwendet?!

Zwar leicht mehr als 4,5 Cent - aber alle Käufe hier waren immer zum Wunsch-BID.

Teilweise 1Mio+

Wurden immer alle total sinnbefreit bedient. Der Verkäufer hätte immer locker 1-2% mehr bekommen können. Ich bin daher auch der felsenfesten Überzeugung, dass es mehr Leerpositionen als handelbare Aktien gibt. Der Knall wird kommen. Die Aktien Richtung LSE vermute ich als convern. Bis jetzt ca. 250 Mio Stück. Schätze, dass noch 1 Mrd+ fehlen (richtig gelesen)....

Optionen

| Boardmail an "Shoppinguin" |

Wertpapier: Steinhoff International |

Letztes halbes Jahr knapp 140 Mio.

Off Book ist ohne Registrierung an der jeweiligen Börse mehr als schwierig für Kleinanleger.

Die kleinen LV Buden in ZA sind nur Mittel zum Zweck, Umsatz JSE gestern und heute über 16 Mio, auch nicht schlecht, waren bestimmt einige Klein-LV´s mit am Werk.

Ist halt wie Materie und Antimaterie:

Kleinanleger und Klein-LV´s ;-)

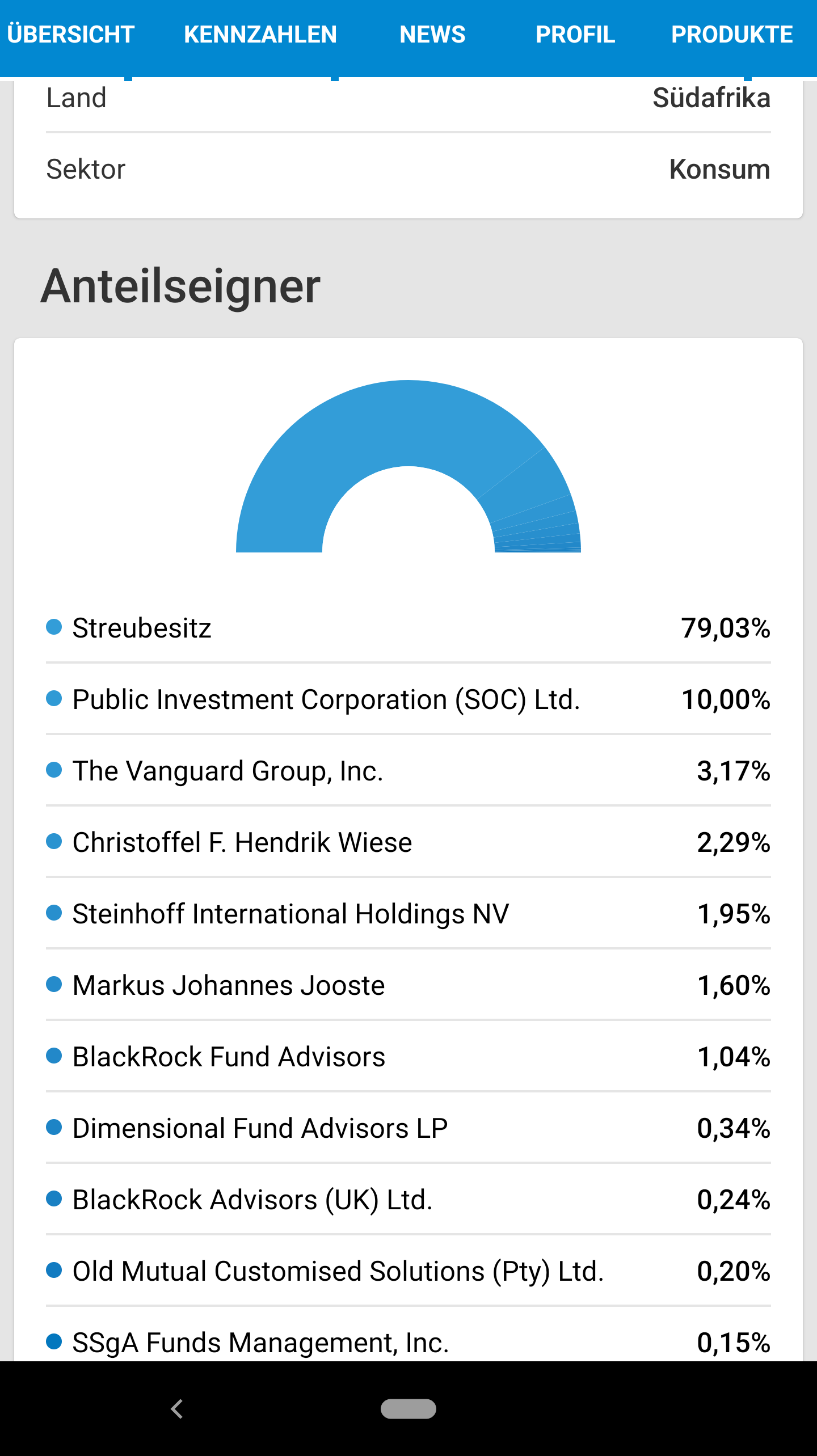

Letztendlich wollen Vanguard, Blackrock, DFA-Dimensional u.a. Verleiher ihre Aktien irgendwann wiedersehen, am Besten mit Aufschlag und da müssen die Klein-LV´s halt Gas geben.

Schwab ist wohl recht stark im LV Bereich unterwegs.

Mal lesen:

https://www.reddit.com/r/Schwab/comments/lp9pza/...s_lending_program/

Optionen

| Boardmail an "Shoppinguin" |

Wertpapier: Steinhoff International |

https://www.finanzen100.de/aktien/...wkn-a14xb9_H1838429818_95206647/

Optionen

| Boardmail an "HAFX55" |

Wertpapier: Steinhoff International |

Angehängte Grafik:

screenshot_20220125-210541.png (verkleinert auf 35%)

screenshot_20220125-210541.png (verkleinert auf 35%)