Ballard Power Systems lebt noch (Wieder)

Seite 524 von 607 Neuester Beitrag: 28.01.25 08:32 | ||||

| Eröffnet am: | 08.01.09 15:04 | von: Lapismuc | Anzahl Beiträge: | 16.166 |

| Neuester Beitrag: | 28.01.25 08:32 | von: Klimawandel | Leser gesamt: | 6.758.445 |

| Forum: | Hot-Stocks | Leser heute: | 983 | |

| Bewertet mit: | ||||

| Seite: < 1 | ... | 522 | 523 | | 525 | 526 | ... 607 > | ||||

Der Markt nimmt in 2020 erstmal fahrt auf. Ballard hat das richtige Produkt zur rechten Zeit fertig und kann liefern.

Viele entwickeln noch. Zb. Bosch will 2022 seine Brennstoffzelle in Serie bringen. Wir haben hier also 2-3 Jahre Vorsprung.

Angehängte Grafik:

2b7c0aa2-7e43-4d18-8b5d-d7344eb6e6bf.jpeg (verkleinert auf 44%)

2b7c0aa2-7e43-4d18-8b5d-d7344eb6e6bf.jpeg (verkleinert auf 44%)

Die Branche fängt doch erst an. In zwei bis drei Jahren können wir abrechnen ob sich die neuen Technologien durchsetzen. 2020 wird das Übergangsjahr.

Gestern gab es über den Tag einzelne Positionen von Aktion Käufe in Höhe zwischen 500 bis 1 Millionen $

Auch in € gab es Stückzahlen bis 75.000 Stück. Deshalb bin ich zuversichtlich über die Entwicklung.

Man darf doch nicht blauäugig sein. Es wird mit einzelnen Meldungen, für die sich hier im blog noch bedankt wird, so getan, als ob Ballard der einzige Spieler auf dem Brennstoffzellenmarkt wäre. Was bringt die Hausse des Brennstoffzellen-/Wasserstoffmarkts, wenn "unsere" Bude auf Sicht nur Miese macht.

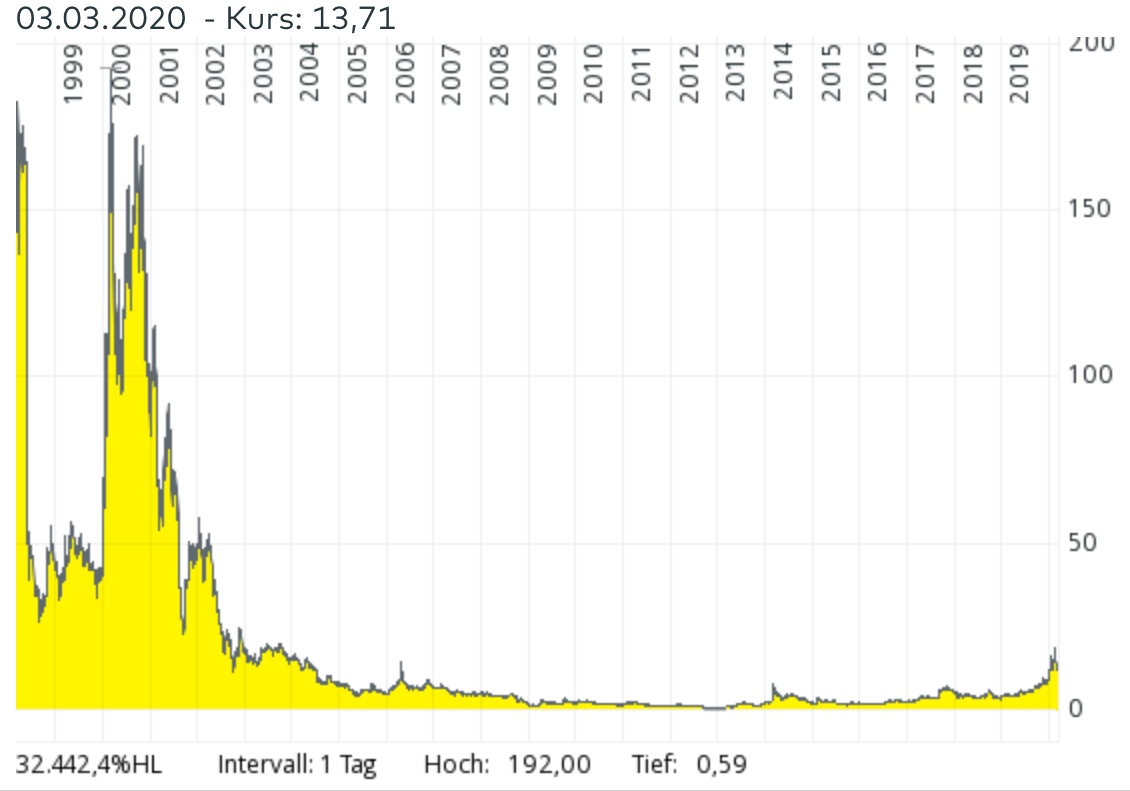

Damals war der Kurs bei ca. 5€ . Bis zur Spitze waren es ca. 14€ in 2020.

Also 9€ Plus seit Nov 2017. Bei 3000 Aktien wären dies heute 27.000€ Gewinn. Und dies, wie du sagst aus solch einer „ Bude“ Wo ist dein Problem ??? Oder warst du schon im Jahr 2001 investiert???

Dann hätte ich natürlich Verständnis :)))))

Angehängte Grafik:

028d4847-4d71-4a38-8265-be63b112622c.jpeg (verkleinert auf 45%)

028d4847-4d71-4a38-8265-be63b112622c.jpeg (verkleinert auf 45%)

Optionen

| Boardmail an "ede.de.knipser" |

Wertpapier: Ballard Power Systems I |

Obwohl es niemanden etwas angeht, bin ich "seit dem Urschleim" dabei und hatte damals bei 40 (!) verkauft und mich grün und blau geärgert, dass ich nicht noch sechs Wochen länger bis 143 gewartet hatte. Zuletzt war ich aber sehr zufrieden, nicht bis 45 Cent dabei geblieben zu sein.

Was mich nervt und ärgert, ist, dass die Kälber, die damals im Hype um den Neuen Markt unendlich viel Geld verbrannt haben, letztlich die Verantwortung dafür tragen, dass sich in Deutschland nur bedingt eine Aktienkultur entwickeln konnte. Praktisch jeder kennt nicht nur einen, der damals -aufgrund seiner Gier, es könne ja nur aufwärts gehen- seine Finger eingeklemmt hat. Keiner von damals will solches wieder erleben, aber es wird wieder passieren, wenn man hier liest ...

Man muss dem Ganzen nur die Chance für eine gesunde Entwicklung geben. Gerade zu einer Zeit, wo es nur wenig vernünftige Anlagemöglichkeiten gibt.

Produktionsstätte in Hobro, des Joint Ventures in China, kosten natürlich Geld. Das sind

große Investitionen in die Zukunft - für Schiffsantriebe liegen bereits Aufträge vor - die jüngsten

Kurssteigerungen sind vielleicht nur ein Vorgriff auf erwartbare Erfolge. Ich jedenfalls bin zufrieden,

nach 328 Transaktionen seit 2005 habe ich einen negativen Durchschnittskurs.....

Ich nicht mehr, meine war die Commerzbank. :((( Da habe ich alle Hoffnungen aufgegeben.

Hier hat man die Chance bei einer neuen Technologie dabei zu sein. Und nicht vergessen....

Jeder ist an der Börse für sein Handeln verantwortlich und nicht die Firma wo man investiert ist.

Ich sehe die ganzen player die im H2 Business sind doch recht überbewertet aufgrund des Hype.

Entweder weit streuen oder die Zeit abwarten, wer sich gut entwickelt.

NmM.

P.S.: @Asiat: Die LH hat vorn einigen Jahren auch die Milliarde Gewinn angestrebt. Als nur 0,7 dabei rauskamen, wollte uns die Geschäftsleitung dieses auch als 300 Mil. Verlust verkaufen...Smiley

Optionen

| Boardmail an "Ab dafür" |

Wertpapier: Ballard Power Systems I |

[PR Newswire]

PR Newswire•March 5, 2020

Record quarterly revenue of $41.9M in Q4

$106.3M full year revenue exceeds 2019 outlook

$147.8M cash reserves at year-end

2020 outlook for revenue of approximately $130 million, supported by 12-month order book of $110.3M at year-end 2019

VANCOUVER, March 4, 2020 /PRNewswire/ - Ballard Power Systems (NASDAQ: BLDP; TSX: BLDP) today announced consolidated financial results for the fourth quarter and full year ended December 31, 2019. All amounts are in U.S. dollars unless otherwise noted and have been prepared in accordance with International Financial Reporting Standards (IFRS).

Randy MacEwen, President and CEO said, "We closed out 2019 with high activity levels, record quarterly revenue of $41.9 million in Q4, and full year revenue of $106.3 million, exceeding our full year outlook. Gross margin for the full year was 21%, Adjusted EBITDA was ($28.2) million and year-end cash reserves were $147.8 million. In 2019 Ballard also delivered continued progress in the execution of our strategy: we launched our next-generation LCS fuel cell stack and FCmoveTM power module, offering lower cost and enhanced performance; we received purchase orders for fuel cell products from the Weichai-Ballard joint venture in China, with construction of the joint venture facility moving toward commissioning by mid-year 2020; we announced our membership in the H2Bus Consortium in Europe as well as the creation of a Marine Center of Excellence at our Denmark facility."

Mr. MacEwen continued, "In 2019 the hydrogen and fuel cell industry experienced remarkable momentum. A total of 18 countries, representing 70% of global GDP, announced hydrogen and fuel cell roadmaps. Major mobility players, including Weichai, Bosch, Cummins, Faurecia, Michelin, CNH, Hyundai and others, committed to significant investments in fuel cells. There is growing consensus in the financial community regarding a reallocation of capital as a direct result of global climate change. And, deployments of fuel cell electric buses and trucks also increased significantly in 2019, led by China."

Mr. MacEwen added, "I believe there is now a consolidated industry view that the most attractive near-term markets for fuel cell electric vehicles, or FCEVs, are in Medium- and Heavy-Duty Motive use cases that feature heavy payload, long daily range and a need for fast refuelling. Two important studies released in January 2020 underscore the expectation that FCEVs will be the most competitive zero-emission option from a total-cost-of-ownership perspective for numerous medium and heavy vehicle use cases, as well as the most environmentally attractive: a Hydrogen Council report, prepared in conjunction with McKinsey, entitled "Path to Hydrogen Competitiveness: A cost perspective"; and a white paper prepared jointly by Deloitte China and Ballard entitled "Fueling the Future of Mobility: Hydrogen and fuel cell solutions for transportation"."

Mr. MacEwen concluded, "Looking ahead to 2020, we anticipate total revenue of approximately $130 million as we address Medium- and Heavy-Duty Motive demand in key global markets. Ballard will continue to invest in world-leading technology and product development, including product cost reduction, while also completing our planned expansion in MEA production capacity at Ballard's Vancouver facility. We will also invest in our Weichai-Ballard joint venture in China, as this facility transitions from construction to operation. In 2020, we will deepen our exposure to the European market as signals further strengthen to decarbonize mobility with hydrogen fuel cell solutions. We anticipate significant longer-term growth in China, Europe and California, setting the stage for attractive returns for Ballard and our shareholders."

Q4 2019 Financial Highlights

(all comparisons are to Q4 2018 unless otherwise noted)

Ballard Power Systems Q4 2019 Financial Highlights (CNW Group/Ballard Power Systems Inc.)

Ballard Power Systems Q4 2019 Financial Highlights (CNW Group/Ballard Power Systems Inc.)

Total revenue was $41.9 million, a 47% year-over-year increase and a record quarter.

Gross margin was 21%, down 4-points to $8.6 million, due primarily to a shift in revenue and product mix.

Cash operating costs2 were $13.6 million, an increase of 21%, due primarily to higher program development and engineering expenses incurred by Ballard Power Systems Europe A/S to support marine market applications.

Adjusted EBITDA2 declined 43% to ($7.4) million, due primarily to higher equity in loss of investment in joint ventures and associates.

Net loss3 was ($10.3) million or ($0.04) per share, improvements of 10% and 21%, respectively, driven primarily by the decrease in loss on sale of assets and by higher finance and other income. Net loss in the fourth quarter of 2018 also included a loss on sale of assets of ($4.0) million, related to the divestiture of Power Manager

Adjusted net loss2 was ($10.3) million or ($0.04) per share, declines of 37% and 22%, respectively.

Cash provided by operating activities was $4.1 million, an improvement of 2,081%, reflecting cash operating loss of ($3.9) million, more than offset by net working capital changes of $8.0 million largely related to lower inventory to satisfy Q4 shipments.

Full Year 2019 Financial Highlights

(all comparisons are to full year 2018 unless otherwise noted)

Ballard Power Systems Full Year 2019 Financial Highlights (CNW Group/Ballard Power Systems Inc.)

Ballard Power Systems Full Year 2019 Financial Highlights (CNW Group/Ballard Power Systems Inc.)

Total revenue was $106.3 million, a 10% year-over-year increase.

Gross margin was 21%, down 10-points to $22.6 million, due primarily to a shift in revenue and product mix, including lower shipments of MEAs to Synergy JVCo and lower Portable Power/UAV revenues resulting from the disposition of Power Manager assets in Q4 2018.

Cash operating costs2 were $40.6 million, a decrease of 6% due primarily to lower expenses as a result of the disposition of Power Manager assets and associated personnel reduction in Q4 2018.

Adjusted EBITDA2 declined to ($28.2) million, due primarily to higher equity in loss of investment in joint venture and associates attributed to the ongoing establishment of Weichai-Ballard JV operations.

Net loss3 increased to ($39.1) million or ($0.17) per share, declines of 43% and 14%, respectively. The increase in net loss was driven primarily by the increase in Adjusted EBITDA loss including higher equity in loss of investment in joint venture and associates.

Adjusted net loss2 was ($37.1) million or ($0.16) per share, declines of 59% and 27%, respectively.

Cash used in operating activities was ($14.2) million, an improvement of 55% reflecting cash operating loss of ($14.1) million and net working capital changes of ($0.1) million.

Cash reserves were $147.8 million at December 31, $44.4 million lower than at the end of 2018.

The Order Backlog at end-2019 was $178.7 million, down from $199.6 million at end-Q3, reflecting $41.9 million in shipments and $21.0 million in new orders in Q4. At end-2019 the 12-month Order Book was $110.3 million, a decrease of $13.3 million from end-Q3, and an increase of $41.3 million from $69.0 million at end-2018.

2020 Outlook

Ballard intends to maintain focus throughout 2020 on Heavy- and Medium-Duty Motive applications – including bus, commercial truck, train and marine segments – to increase penetration in the key markets of China, Europe and California. We will continue to invest in next-generation products and technology, including MEAs, stacks, modules, and system integration, as well as advanced manufacturing processes, technologies and equipment. We will also continue to invest in technology and product cost reduction and in production capacity expansion.

At the present time the Company's 2020 outlook does not reflect any material impact of the coronavirus disease (COVID-19). It is currently too early to accurately project any impact, since the duration and scope of the outbreak is not yet known with any certainty. If the outbreak continues for an extended period of time, Ballard and the Weichai-Ballard JV may experience supply chain disruptions, a decline in sales activities, and reductions in operations and workforce.

Consistent with the Company's practice, and in view of the early stage of hydrogen fuel cell market development and adoption, Ballard is not providing specific financial performance guidance for 2020. However, directionally the Company anticipates total revenue of approximately $130 million in 2020. This growth is expected to primarily result from commercial progress in the Heavy-Duty Motive segment, underpinned by increasing demand for FCEVs in China and Europe. Ballard's 12-month Order Book of $110.3 million at the end of 2019, together with a robust sales pipeline, establishes a strong foundation for our projected full year 2020 revenue outlook.

In China, the Company continues to expect the Weichai-Ballard JV facility to be commissioned and operating by mid-year 2020. Ballard anticipates delivery of membrane electrode assemblies to the Weichai-Ballard JV for the production of next-generation LCS fuel cell stacks and FCmoveTM fuel cell modules. During 2020 the Company has a commitment to make contributions totaling approximately $20 million towards its pro rata ownership share of the Weichai-Ballard JV. This is in addition to $20.9 million contributed in 2019 and $14.6 million contributed in 2018, as part of Ballard's total capital commitment of approximately $78 million. The Company also expects to report equity losses of approximately $10-15 million in connection with the Weichai-Ballard JV in 2020.

In Europe, during 2020 Ballard plans to continue execution of its automotive program with Audi, and to deliver a significant number of modules to support deployments of Fuel Cell Electric Buses (FCEBs) in a number of countries. The Company also expects increased market activity for FCEBs, which can be expected to result in additional module purchase orders.

Within North America in 2020, Ballard expects continued market activity in California for FCEBs and fuel cell-powered trucks, which can be expected to result in additional module purchase orders. In addition, the Company expects a volume contraction of fuel cell stack sales for material handling applications.

Technology Solutions revenue is expected to be relatively flat in 2020, compared to 2019, primarily reflecting ongoing work on our technology transfer programs with Audi and Weichai-Ballard JV. In addition to the Audi and Weichai-Ballard JV programs, Technology Solutions engineering services activity is expected with existing and new customers in a variety of markets.

Ballard intends to establish an At-The-Market equity program ("ATM Program") and to issue up to $75 million of common shares from treasury to the public from time to time at the Company's discretion, subject to favorable market conditions. The ATM Program will be conducted under the Company's existing $150 million Base Shelf Prospectus and will be used to fund growth and strategic opportunities.

Q4 & Full Year 2019 Financial Summary

Optionen

| Boardmail an "luxi1" |

Wertpapier: Ballard Power Systems I |

$106.3M full year revenue exceeds 2019 outlook

$147.8M cash reserves at year-end

2020 outlook for revenue of approximately $130 million, supported by 12-month order book of $110.3M at year-end 2019