der USA Crash Thread ...

-> Totaler crash, nix geht mehr, dow 3.000 dax 1500, gold 10.000

-> Dollar ist Abfall

Angehängte Grafik:

dollarnote.jpg

dollarnote.jpg

First, this is the worst housing recession in US history and there is no sign it will bottom out any time soon. At this point it is clear that US home prices will fall between 20% and 30% from their bubbly peak; that would wipe out between $4 trillion and $6 trillion of household wealth. While the subprime meltdown is likely to cause about 2.2 million foreclosures, a 30% fall in home values would imply that over 10 million households would have negative equity in their homes and would have a big incentive to use "jingle mail" (i.e. default, put the home keys in an envelope and send it to their mortgage bank). Moreover, soon enough a few very large home builders will go bankrupt and join the dozens of other small ones that have already gone bankrupt thus leading to another free fall in home builders' stock prices that have irrationally rallied in the last few weeks in spite of a worsening housing recession.

Second, losses for the financial system from the subprime disaster are now estimated to be as high as $250 to $300 billion. But the financial losses will not be only in subprime mortgages and the related RMBS and CDOs. They are now spreading to near prime and prime mortgages as the same reckless lending practices in subprime (no down-payment, no verification of income, jobs and assets (i.e. NINJA or LIAR loans), interest rate only, negative amortization, teaser rates, etc.) were occurring across the entire spectrum of mortgages; about 60% of all mortgage origination since 2005 through 2007 had these reckless and toxic features.

So this is a generalized mortgage crisis and meltdown, not just a subprime one. And losses among all sorts of mortgages will sharply increase as home prices fall sharply and the economy spins into a serious recession. Goldman Sachs now estimates total mortgage credit losses of about $400 billion; but the eventual figures could be much larger if home prices fall more than 20%. Also, the RMBS and CDO markets for securitization of mortgages - already dead for subprime and frozen for other mortgages - remain in a severe credit crunch, thus reducing further the ability of banks to originate mortgages. The mortgage credit crunch will become even more severe.

Also add to the woes and losses of the financial institutions the meltdown of hundreds of billions of off balance SIVs and conduits; this meltdown and the roll-off of the ABCP market has forced banks to bring back on balance sheet these toxic off balance sheet vehicles adding to the capital and liquidity crunch of the financial institutions and adding to their on balance sheet losses. And because of securitization the securitized toxic waste has been spread from banks to capital markets and their investors in the US and abroad, thus increasing - rather than reducing systemic risk - and making the credit crunch global.

Third, the recession will lead - as it is already doing - to a sharp increase in defaults on other forms of unsecured consumer debt: credit cards, auto loans, student loans. There are dozens of millions of subprime credit cards and subprime auto loans in the US. And again defaults in these consumer debt categories will not be limited to subprime borrowers. So add these losses to the financial losses of banks and of other financial institutions (as also these debts were securitized in ABS products), thus leading to a more severe credit crunch. As the Fed loan officers survey suggest the credit crunch is spreading throughout the mortgage market and from mortgages to consumer credit, and from large banks to smaller banks.

Fourth, while there is serious uncertainty about the losses that monolines will undertake on their insurance of RMBS, CDO and other toxic ABS products, it is now clear that such losses are much higher than the $10-15 billion rescue package that regulators are trying to patch up. Some monolines are actually borderline insolvent and none of them deserves at this point a AAA rating regardless of how much realistic recapitalization is provided. Any business that required an AAA rating to stay in business is a business that does not deserve such a rating in the first place. The monolines should be downgraded as no private rescue package - short of an unlikely public bailout - is realistic or feasible given the deep losses of the monolines on their insurance of toxic ABS products.

Next, the downgrade of the monolines will lead to another $150 of writedowns on ABS portfolios for financial institutions that have already massive losses. It will also lead to additional losses on their portfolio of muni bonds. The downgrade of the monolines will also lead to large losses - and potential runs - on the money market funds that invested in some of these toxic products. The money market funds that are backed by banks or that bought liquidity protection from banks against the risk of a fall in the NAV may avoid a run but such a rescue will exacerbate the capital and liquidity problems of their underwriters. The monolines' downgrade will then also lead to another sharp drop in US equity markets that are already shaken by the risk of a severe recession and large losses in the financial system.

Fifth, the commercial real estate loan market will soon enter into a meltdown similar to the subprime one. Lending practices in commercial real estate were as reckless as those in residential real estate. The housing crisis will lead - with a short lag - to a bust in non-residential construction as no one will want to build offices, stores, shopping malls/centers in ghost towns. The CMBX index is already pricing a massive increase in credit spreads for non-residential mortgages/loans. And new origination of commercial real estate mortgages is already semi-frozen today; the commercial real estate mortgage market is already seizing up today.

Sixth, it is possible that some large regional or even national bank that is very exposed to mortgages, residential and commercial, will go bankrupt. Thus some big banks may join the 200 plus subprime lenders that have gone bankrupt. This, like in the case of Northern Rock, will lead to depositors' panic and concerns about deposit insurance. The Fed will have to reaffirm the implicit doctrine that some banks are too big to be allowed to fail. But these bank bankruptcies will lead to severe fiscal losses of bank bailout and effective nationalization of the affected institutions. Already Countrywide - an institution that was more likely insolvent than illiquid - has been bailed out with public money via a $55 billion loan from the FHLB system, a semi-public system of funding of mortgage lenders. Banks' bankruptcies will add to an already severe credit crunch.

Seventh, the banks losses on their portfolio of leveraged loans are already large and growing. The ability of financial institutions to syndicate and securitize their leveraged loans - a good chunk of which were issued to finance very risky and reckless LBOs - is now at serious risk. And hundreds of billions of dollars of leveraged loans are now stuck on the balance sheet of financial institutions at values well below par (currently about 90 cents on the dollar but soon much lower). Add to this that many reckless LBOs (as senseless LBOs with debt to earnings ratio of seven or eight had become the norm during the go-go days of the credit bubble) have now been postponed, restructured or cancelled. And add to this problem the fact that some actual large LBOs will end up into bankruptcy as some of these corporations taken private are effectively bankrupt in a recession and given the repricing of risk; convenant-lite and PIK toggles may only postpone - not avoid - such bankruptcies and make them uglier when they do eventually occur. The leveraged loans mess is already leading to a freezing up of the CLO market and to growing losses for financial institutions.

Eighth, once a severe recession is underway a massive wave of corporate defaults will take place. In a typical year US corporate default rates are about 3.8% (average for 1971-2007); in 2006 and 2007 this figure was a puny 0.6%. And in a typical US recession such default rates surge above 10%. Also during such distressed periods the RGD - or recovery given default - rates are much lower, thus adding to the total losses from a default. Default rates were very low in the last two years because of a slosh of liquidity, easy credit conditions and very low spreads (with junk bond yields being only 260bps above Treasuries until mid June 2007). But now the repricing of risk has been massive: junk bond spreads close to 700bps, iTraxx and CDX indices pricing massive corporate default rates and the junk bond yield issuance market is now semi-frozen.

While on average the US and European corporations are in better shape - in terms of profitability and debt burden - than in 2001 there is a large fat tail of corporations with very low profitability and that have piled up a mass of junk bond debt that will soon come to refinancing at much higher spreads. Corporate default rates will surge during the 2008 recession and peak well above 10% based on recent studies. And once defaults are higher and credit spreads higher massive losses will occur among the credit default swaps (CDS) that provided protection against corporate defaults. Estimates of the losses on a notional value of $50 trillion CDS against a bond base of $5 trillion are varied (from $20 billion to $250 billion with a number closer to the latter figure more likely). Losses on CDS do not represent only a transfer of wealth from those who sold protection to those who bought it. If losses are large some of the counterparties who sold protection - possibly large institutions such as monolines, some hedge funds or a large broker dealer - may go bankrupt leading to even greater systemic risk as those who bought protection may face counterparties who cannot pay.

Ninth, the "shadow banking system" (as defined by the PIMCO folks) or more precisely the "shadow financial system" (as it is composed by non-bank financial institutions) will soon get into serious trouble. This shadow financial system is composed of financial institutions that - like banks - borrow short and in liquid forms and lend or invest long in more illiquid assets. This system includes: SIVs, conduits, money market funds, monolines, investment banks, hedge funds and other non-bank financial institutions. All these institutions are subject to market risk, credit risk (given their risky investments) and especially liquidity/rollover risk as their short term liquid liabilities can be rolled off easily while their assets are more long term and illiquid. Unlike banks these non-bank financial institutions don't have direct or indirect access to the central bank's lender of last resort support as they are not depository institutions.

Thus, in the case of financial distress and/or illiquidity they may go bankrupt because of both insolvency and/or lack of liquidity and inability to roll over or refinance their short term liabilities. Deepening problems in the economy and in the financial markets and poor risk managements will lead some of these institutions to go belly up: a few large hedge funds, a few money market funds, the entire SIV system and, possibly, one or two large and systemically important broker dealers. Dealing with the distress of this shadow financial system will be very problematic as this system - stressed by credit and liquidity problems - cannot be directly rescued by the central banks in the way that banks can.

Tenth, stock markets in the US and abroad will start pricing a severe US recession - rather than a mild recession - and a sharp global economic slowdown. The fall in stock markets - after the late January 2008 rally fizzles out - will resume as investors will soon realize that the economic downturn is more severe, that the monolines will not be rescued, that financial losses will mount, and that earnings will sharply drop in a recession not just among financial firms but also non financial ones. A few long equity hedge funds will go belly up in 2008 after the massive losses of many hedge funds in August, November and, again, January 2008. Large margin calls will be triggered for long equity investors and another round of massive equity shorting will take place. Long covering and margin calls will lead to a cascading fall in equity markets in the US and a transmission to global equity markets. US and global equity markets will enter into a persistent bear market as in a typical US recession the S&P500 falls by about 28%.

Eleventh, the worsening credit crunch that is affecting most credit markets and credit derivative markets will lead to a dry-up of liquidity in a variety of financial markets, including otherwise very liquid derivatives markets. Another round of credit crunch in interbank markets will ensue triggered by counterparty risk, lack of trust, liquidity premia and credit risk. A variety of interbank rates - TED spreads, BOR-OIS spreads, BOT - Tbill spreads, interbank-policy rate spreads, swap spreads, VIX and other gauges of investors' risk aversion - will massively widen again. Even the easing of the liquidity crunch after massive central banks' actions in December and January will reverse as credit concerns keep interbank spread wide in spite of further injections of liquidity by central banks.

Twelfth, a vicious circle of losses, capital reduction, credit contraction, forced liquidation and fire sales of assets at below fundamental prices will ensue leading to a cascading and mounting cycle of losses and further credit contraction. In illiquid market actual market prices are now even lower than the lower fundamental value that they now have given the credit problems in the economy. Market prices include a large illiquidity discount on top of the discount due to the credit and fundamental problems of the underlying assets that are backing the distressed financial assets. Capital losses will lead to margin calls and further reduction of risk taking by a variety of financial institutions that are now forced to mark to market their positions. Such a forced fire sale of assets in illiquid markets will lead to further losses that will further contract credit and trigger further margin calls and disintermediation of credit. The triggering event for the next round of this cascade is the downgrade of the monolines and the ensuing sharp drop in equity markets; both will trigger margin calls and further credit disintermediation.

Based on estimates by Goldman Sachs $200 billion of losses in the financial system lead to a contraction of credit of $2 trillion given that institutions hold about $10 of assets per dollar of capital. The recapitalization of banks sovereign wealth funds - about $80 billion so far - will be unable to stop this credit disintermediation - (the move from off balance sheet to on balance sheet and moves of assets and liabilities from the shadow banking system to the formal banking system) and the ensuing contraction in credit as the mounting losses will dominate by a large margin any bank recapitalization from SWFs. A contagious and cascading spiral of credit disintermediation, credit contraction, sharp fall in asset prices and sharp widening in credit spreads will then be transmitted to most parts of the financial system. This massive credit crunch will make the economic contraction more severe and lead to further financial losses. Total losses in the financial system will add up to more than $1 trillion and the economic recession will become deeper, more protracted and severe.

A near global economic recession will ensue as the financial and credit losses and the credit crunch spread around the world. Panic, fire sales, cascading fall in asset prices will exacerbate the financial and real economic distress as a number of large and systemically important financial institutions go bankrupt. A 1987 style stock market crash could occur leading to further panic and severe financial and economic distress. Monetary and fiscal easing will not be able to prevent a systemic financial meltdown as credit and insolvency problems trump illiquidity problems. The lack of trust in counterparties - driven by the opacity and lack of transparency in financial markets, and uncertainty about the size of the losses and who is holding the toxic waste securities - will add to the impotence of monetary policy and lead to massive hoarding of liquidity that will exacerbates the liquidity and credit crunch.

In this meltdown scenario US and global financial markets will experience their most severe crisis in the last quarter of a century.

Can the Fed and other financial officials avoid this nightmare scenario that keeps them awake at night? The answer to this question - to be detailed in a follow-up article - is twofold: first, it is not easy to manage and control such a contagious financial crisis that is more severe and dangerous than any faced by the US in a quarter of a century; second, the extent and severity of this financial crisis will depend on whether the policy response - monetary, fiscal, regulatory, financial and otherwise - is coherent, timely and credible. I will argue - in my next article - that one should be pessimistic about the ability of policy and financial authorities to manage and contain a crisis of this magnitude; thus, one should be prepared for the worst, i.e. a systemic financial crisis.

Der Fall

Käsch

sieht ihn

den

crash.

aus dem Band II der gesammelten schriften "Die gefallenen Banken"

Optionen

| Boardmail an "käsch" |

Wertpapier: Dow Jones Industrial Av |

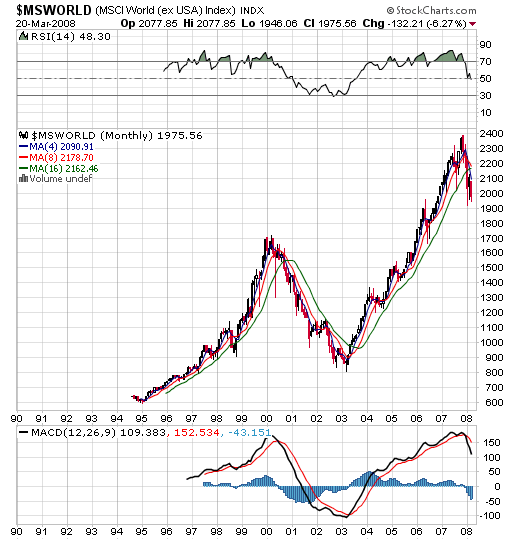

Angehängte Grafik:

_msworld1990m.png (verkleinert auf 98%)

_msworld1990m.png (verkleinert auf 98%)

Ich denke du meinst wohl eher Greenspan. Denn Bernanke muss den ganzen scheiss jetzt ausbaden. Auch wenn du es nicht glaubst. Bernanke handelt genau richtig. Es wird Liquidität im wahrsten Sinne des Wortes hergestellt und billiges Geld für die Banken bereitgestellt, um das Vetrauen der Banken untereinander herzustellen.