Quo Vadis Dax 2010 - Das Original

das war das TH vom Freitag,

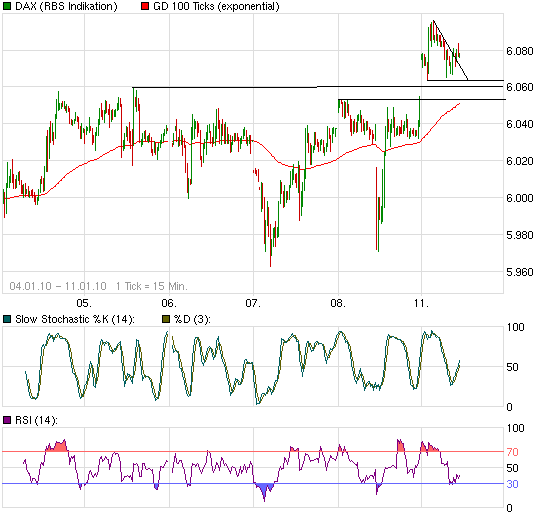

da dann durch die Unterstützung,

sind auch 6026 machbar

und die bullen pennen auf ihren longs

und warten auf die auflösung der bullflag im 60er

6055-60 sup bereich der halten sollte, mit dem

nächsten sup bei 6035, dem 20er ma

allerdings über 6100 sollte es auch schwer werden

na dann warten wir weiter auf die amis

Angehängte Grafik:

dax_60er.gif (verkleinert auf 83%)

dax_60er.gif (verkleinert auf 83%)

Ohne Amerika geht es offensichtlich weder rauf noch runter. Meine vor 15 Jahren verstorbene Großmutter hat noch mehr Eigenleben als der Dax

Optionen

z.zt flat

warte auf die amis und häng mich darauf

such nen longeinstieg am sup

Lufthansa + 1,6% - ich kapiere es nicht, ich bin ja auch kein Lufthansaaktionär

Tatsächlich seit letztem Jahr sehe ich hier vielleicht 15 Leute noch. Der Rest alles neue Namen die wieder weg sein werden.

Optionen

Commentary: The secrets of Wall Street aren't so secret

By David Weidner, MarketWatch

NEW YORK (MarketWatch) -- Regular readers of this column know that it rarely, if ever, dispenses investment advice. That's a big reason why it's still around after all these years.

There is, however, a difference between investment advice and investing principles.

After hanging around Wall Street for so long, I've learned a few investing principles that stand the test of time. They're just as true in bear markets as they are in bull markets.

Some are maxims you hear every quarter from your broker. Some aren't talked about very much. Maybe it's because Wall Street wants us to believe the markets are something they're not.

This brings us to our first investing principle:

The markets are a dangerous place.

The markets are little more than legitimized casinos. They aren't safe. If investors really wanted safety, they would invest in FDIC-insured savings accounts, certificates of deposit or municipal bonds.

Sure, many of those "safe" investments carry risk, but they are the modern-day equivalent of mattress-stuffing compared to investing in stocks, bonds, commodities, mutual funds, exchange-traded funds and all of their derivatives.

Some people will tell you that you can hedge these bets. You can invest in options or futures or take short positions. But insuring trades has never made sense to me. If you have to spend money to hedge a bet, it probably means you can't afford to invest the money.

Most of us who invest in the stock market are well aware of the risk. We take that risk because we want to beat inflation or the anemic returns of some of the aforementioned safer investments. Wall Street makes investing sound complicated, but it really comes down to our second principle:

Greed and fear drive the markets.

When the Dow Jones Industrial Average (INDEX:INDU) soared above 14,000 and the S&P 500 Index (INDEX:SPX) climbed to 1,500, they did so because investors got greedy.

Through the middle of the last decade, real gross-domestic-product growth was around 3%. Yet, in just a span of seven years, the Dow rose 40%. It was speculative greed. Investors didn't want to miss the easy money. It was 1928 all over again.

Reuters

Warren Buffett

So, what happened to cause the collapse? A massive decline in industrial output? Of course not.

When the first few subprime loans began to go sour, everyone rushed to the exits. It wasn't just fear -- it was panic. The market sold off 50%.

Again, output didn't fall anywhere near that much, just 6.4% at its worst during the first three months of 2009. And, of course, it's recovered some of that ground.

The bottom line is this: Greed made the market go up, and fear made it go down. Even Warren Buffett's Berkshire Hathaway Inc. (NYSE:BRK.A) , up just 2.3% last year compared to 23% for the S&P 500, couldn't get that right. And that brings us to the third principle:

Technical analysis does not work.

Take a look at a price graph of your favorite investment during the last year. Now, look at the graph using a time span of two years, a decade and, finally, since inception.

SPX 1,145, +3.29, +0.29%

1,5001,0005000SSSSSSSSSSSSSSSSSSSSSSSSSSSSSee a pattern that doesn't require you to keep an investment for more than a quarter-century and doesn't shrink to near-zero when accounting for inflation?

Me neither.

When it comes to markets, what can go wrong will, and bubbles happen. The problem is we never know which is which until it's too late.

And one more point on this: Anyone who tells you a stock is overvalued or undervalued is full of baloney. As R.O.I. columnist Brett Arends wrote recently, "The price something used to be is irrelevant." His evidence: tech stocks from 2000 to 2002 and bank stocks from 2007 to 2009. See his column on the decade's investing lessons.

That's why it's essential to adhere to the fourth principle...

Stay liquid and diversify.

And by that, I don't mean buying balanced mutual funds. I mean balancing your life. Investors should broaden their idea of what an investment is. Sure, real estate, stocks, bonds and commodities are investments, but so are education, art, spirituality, vacations, health and children. These are opportunities, too. Your broker may not talk about them much, but that doesn't make them potentially any less rewarding or beneficial.

Indeed, you might want to find someone else to guide you if your adviser doesn't acknowledge that:

You should never invest with money that will be or could be needed right away. If you have a tuition payment due next fall, don't bet it on Google Inc. (NASDAQ:GOOG) now, no matter what you think the company's prospects are. Investing is a long-term game; gambling is a short one.

Money you may need in the next couple of years should be in a savings account or the equivalent. Unless you pay off your credit card every month, it shouldn't be used in anything but an extreme emergency.

Investments are always priced at their worth. Forget price-to-earnings ratios, return on equity, value relative to peers and that other gobbledygook Wall Street uses to rationalize trading. If a stock is $10, it's worth $10 because that's what someone is willing to pay for it, and that -- not the underlying company's prospects or earnings -- is what matters.

Actively managed mutual funds rarely, if ever, beat their benchmarks consistently. Factor in management fees and other costs, and there's no compelling reason to invest in them as opposed to exchange-traded or index funds. See report on mutual fund fees and performance.

All of these principles are so simple -- some so ingrained in us -- that I'm fully confident most of us could manage our own portfolios with as good or better success than the pros.

The problem is that most of us don't have time to manage high-risk investments or big investment portfolios. What good is a principle if you're too busy with work and life to employ it?

That's where Wall Street comes in, of course. For a fee, they'll take care of your investments.

But be warned: There's a different set of principles at work.

Optionen

30 punkte bewegung, total seitwärts auf neuen hochs.....

Klar ist kurzfristig -innerhalb der nächsten 60 Minuten- nichts aufregendes zu erwarten, mir ging es aber darum, abzuklären, wo wir sind "Status Quo", um die Frage nach dem "Quo Vadis" zu klären.

Aber , wenn daran hier keine Interesse mehr besteht, sage ich leise "servus" und lese nur noch ab und an.

Optionen

indikatoren abgebaut, und könnten ein retest des

tageshochs möglich machen

unter 6050 6020 und 6000

Angehängte Grafik:

chart_week_daxperformance.png (verkleinert auf 93%)

chart_week_daxperformance.png (verkleinert auf 93%)

ein bischen längere blick zeigt einen soliden trenkanal,

der erst unter 10250 gebrochen wird

mal sehen wie sich die berichtssaison entwickelt

glaube das wird die richtung für das 1.qu vorgeben:

korrektur oder weiter rauf

Angehängte Grafik:

dow_daily.gif (verkleinert auf 83%)

dow_daily.gif (verkleinert auf 83%)