K+S wird unterschätzt

Optionen

| Boardmail an "Terminator100" |

Wertpapier: K+S AG |

Optionen

| Boardmail an "tommi12" |

Wertpapier: K+S AG |

The majority of this decline is due to weather issues in North America, weakness in palm oil prices in Southeast Asia, and customers waiting for the contract settlement. These factors represent short-term challenges not structural changes, with potash affordability remaining high and inventory is expected to be pulled through the channel in the fourth quarter and first part of 2020, we anticipate a strong recovery in demand."

https://seekingalpha.com/article/...s-earnings-call-transcript?page=1

Good morning. Can you comment on your confidence level of your 2020 global potash demand forecast of 67 million tons to 69 million tons? And maybe what are your thoughts, what are the assumptions in China and Brazil in 2020?

Charles Magro

Sure. Good morning, Jacob. So look, the way we're looking at the potash business, if you step back and you look at the long-term history. But the potash market has been growing pretty consistently at 2.5% to 3% per year, but over that period of time, we have seen pullbacks in demand over the years and really that's because of inventory getting build up in the system, which in the potash world we really can't see with great clarity. But the last five years, if you just look at the last five years of the potash market, it's grown at closer to 4% per year. So was this pull back really expected, not really, but I don't think we can even say it was a surprise. So when you look at 2019, there were two really key drivers that pulled back the expected demand now, One is North American weather, which we've talked a lot about and the second was palm oil pricing being so low in Southeast Asia.

So when we look forward to 2020, we expect both of those to correct themselves. We're going to assume normal weather in North America, and when we look at our, as you recall, we bought a company called Waypoint last year, which is the largest soil sampling business in the United States, and the data that we're getting from that is really quite fascinating and what it is showing us is that there are some areas that are quite potash deficient in North America which shouldn't be a surprise considering the weather we had in the spring and even in the last fall. So we do think the underlying demand in North America is going to rebound next year.

When it comes to palm oil, we are seeing prices that are up. There is an increase in demand for biofuels in Asia, and so all of that bodes well for a rebound next year in Southeast Asia. The other markets that we're expecting to grow next year, of course, Brazil, just more acres being put in the production, and then of course, India, which I mentioned, had good rains this year. China, our assumption would be more flat this year, but if you look at the aggregate of all of what I've just described, it is our call today that we would be at the 67 million tons to 69 million tons for 2020, up from the 64 million tons to 65 million tons, and if you just take that number and you go back five years that would put us back on trend point of about a 2.5% annual growth rate. So we are pretty confident with the 67 million tons to 69 million tons today."

https://seekingalpha.com/article/...s-earnings-call-transcript?page=4

Du weißt doch, der Fehler liegt doch ausschließlich bei Dir selbst (und mir)...

:-)

Optionen

| Boardmail an "tommi12" |

Wertpapier: K+S AG |

Beides aktuell sehr negative Schlagwörter und deshalb von Investoren gemieden wie die Pest ...

Der direkte Vergleich von K+S und Lufthansa gibt dies allerdings nicht so wieder.

Sollte etwa doch das Management entscheidend sein ???

Falls der Verdacht aufkommt: Nein, ich trinke nichts zum frühen Morgen :-)

Aber ohne ein bisschen Humor macht das ja alles keinen Spaß mehr...

Habt alle einen schönen Tag!

Jeder ist seines Glückes Schmied, aber im Notfall hat man dann ja wieder einen neuen Schuldigen, falls es nicht so kommt. Aktienkauf ist SPEKULATION und den Kaufbutton drückt man selbst.

Du hättest auch gleich Deinen Satz von gestern kopieren können: "Das sah im März 2019 noch komplett anders aus."

PODCAST: Indian supply settlement brings stability to potash market - for now

Author: Sylvia Traganida

2019/11/07

LONDON (ICIS)--Andy Hemphill, Senior Markets Editor for potash and sulphuric acid, speaks to Sylvia Traganida about a key long-term import contract agreed between Indian importer IPL and muriate of potash (MOP) producers, including Russia’s Uralkali, and Belarusian Potash – and what it could mean for the global potash trade in the year ahead.

https://www.icis.com/explore/resources/news/2019/...sh-market-for-now

ICL EPS beats by $0.01

ICL Reports Q3 2019 Results $ICL

https://seekingalpha.com/pr/17690411

Der Lebensmittelriese Nestlé arbeitet ab sofort mit Corbion zusammen, einem niederländischen Hersteller biochemischer Produkte. Gemeinsam wollen sie Inhaltsstoffe auf Mikroalgenbasis entwickeln und vermarkten.

Klare Leseempfehlung

K+S: How Hard Will The Potash Downcycle Bite? $KPLUF

https://seekingalpha.com/article/4304197

Von meinem iPhone gesendet

„LONDON/BEIJING (Reuters) - China is scouring the world for meat to replace the millions of pigs killed by African swine fever (ASF), boosting prices, business and profits for European and South American meatpackers as it re-shapes global markets for pork, beef and chicken.“

https://www.reuters.com/article/...as-swine-fever-rages-idUSKBN1XI0OT

NOVEMBER 8, 2019 / 11:14 AM / A DAY AGO

Three dozen rescued after blast in east German potash mine

https://www.reuters.com/article/us-germany-mine/...mine-idUSKBN1XI162

Der Autor erwartet für 2020 ein EBITDA von 650 Mio Euro und bei einem 8x Verhältnis zum EV (Marktkapitaliseirung + Schulden) einen Kurs von 5,5 €. Das ist wahrscheinlich das Worstcase-Scenario, aber es ist interessant zu sehen, wie stark der Rückgang der Verkaufspreise bei MOP den Kurs beeinflussen kann (wenn er tatsächlich 2 Jahre dauert).

Ein einziges Aspekt ist meiner Meinung nach in dieser Analyse nicht berücksichtigt: Der europäische Markt ist geschützt im Bereich Kali - die Konkurrenten (z. B. Belaruskali, Uralkali und Canpotex) können hier nicht ohne Weiteres Marktanteile gewinnen.

" (...) Ein einziges Aspekt ist meiner Meinung nach in dieser Analyse nicht berücksichtigt: Der europäische Markt ist geschützt im Bereich Kali - die Konkurrenten (z. B. Belaruskali, Uralkali und Canpotex) können hier nicht ohne Weiteres Marktanteile gewinnen. (...)"

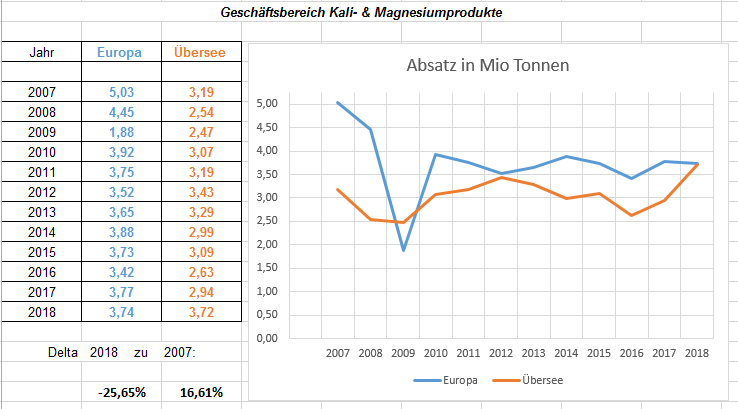

Aber leider ist der Absatz in Europa seit 2007 um rd. 26 % gefallen und der Anteil in Übersee nur um rd. 17 % gestiegen (vgl. GB 2007 bis 2018):

Angehängte Grafik:

screenshot_(698).png (verkleinert auf 69%)

screenshot_(698).png (verkleinert auf 69%)

Moderation

Zeitpunkt: 14.11.19 13:25

Aktionen: Löschung des Beitrages, Nutzer-Sperre für 1 Tag

Kommentar: Provokation

Zeitpunkt: 14.11.19 13:25

Aktionen: Löschung des Beitrages, Nutzer-Sperre für 1 Tag

Kommentar: Provokation

http://www.mosaicco.com/documents/2-20191108-125855.pdf

"...und der Anteil in Übersee nur um rd. 17 % gestiegen "

Ist die Steigerung des Marktanteils in Übersee etwa ungünstig für K+S? :O

Du und deine Grafiken und Tabellen mit den dazugehörigen sehr freien Interpretationen...

Die Wahrheit ist, dass der Anteil in EUR zuletzt relativ stabil blieb und der in Übersee nach einem Einbruch bis 2016 von Lohr wieder zu einem neuen Spitzenwert in den letzten 12 Jahren geführt wurde. :))

Optionen

| Boardmail an "Torsten1971" |

Wertpapier: K+S AG |

" (...) Oder so: Aber Gott sein Dank ist der Absatz in Europa seit 2009 um rd. 100 % gestiegen...(und da hätte man immerhin noch den wesentlich sinnvolleren 10 Jahresvergleich) (...)"

Es ist Ihrer Meinung nach aussagefähiger einen einmaligen Einbruch als Basis heranzuziehen als die vergleichbaren Werte?! Da würde ich den Vorschlag machen, K+S stellt für ein Jahr den Absatz und Sie können im folge Jahr - ganz im Sinne des Vorstands - posten, K+S hat seinen Absatz verdoppelt. Merke Sie eigentlich, wie lächerlich Ihr Versuch ist gegen die Faktenlage zu posten.....

" (...) "...und der Anteil in Übersee nur um rd. 17 % gestiegen "

Ist die Steigerung des Marktanteils in Übersee etwa ungünstig für K+S? :O (...)"

Was wollen Sie uns nun wieder damit sagen?

Ich habe erwartet, dass Sie sich - wie jeder logisch denkende Anleger fragt - , warum hat K+S seinen Absatz in Europa um 1.290.000 Tonnen reduziert, aber in Übersee leider nur 530.000 Tonnen hinzugewinnen konnte. Und das obwohl doch die Weltbevölkerung stetig steigt.

Sehen Sie da keinen marginalen Widerspruch? Oder ist die Halbwertzeit für dieses vom Vorstand wiederholte publizierte Argument auch schon wieder abgelaufen?! (Dann würde er ja wenigsten einmal einen Seitenblick wagen.)

" (....) Die Wahrheit ist, dass der Anteil in EUR zuletzt relativ stabil blieb und der in Übersee nach einem Einbruch bis 2016 von Lohr wieder zu einem neuen Spitzenwert in den letzten 12 Jahren geführt wurde. :)) (...)"

Spitzenwert, aha. Dann rechnen wir doch einmal gemeinsam:

2007 = Europa 5,03 + Übersee 3,19 = 8,22 Mio Tonnen

2018 = Europa 3,74 + Übersee 3,72 = 7,46 Mio Tonnen

Nach meiner Schulkenntnis sind das 760.000 Tonnen oder 10% weniger! Ein neuer Spitzenwert? Ja will sich denn K+S aus dem Markt gänzlich zurück ziehen und somit neue negativ Werte präferieren oder wie soll man das nun verstehen?

" (...) Die Wahrheit ist, dass der Anteil in EUR zuletzt relativ stabil blieb (...)"

Aber halt, SIE wollten ja ganz geschickt über den Währungseffekt ablenken. Ganz wie es die IR machen würde? Nur zeigt die Grafik die von K+S veröffentlichten Absatzmengen und die werden nun einmal nicht in EURO sondern in Tonnen zum Ausdruck gebracht.

Alles in allem also ein echter Torsten. Und das vor dem Hintergrund eines ungebrochenen fallenden Kurstrend. Sie sind mir ja einer, Torsten.

Fast könnte man Mitleid haben, zu beneiden sind Sie jedenfalls nicht....