against all odds

Seite 95 von 117 Neuester Beitrag: 08.04.20 16:14 | ||||

| Eröffnet am: | 22.03.13 19:18 | von: Fillorkill | Anzahl Beiträge: | 3.904 |

| Neuester Beitrag: | 08.04.20 16:14 | von: Fillorkill | Leser gesamt: | 346.089 |

| Forum: | Börse | Leser heute: | 161 | |

| Bewertet mit: | ||||

| Seite: < 1 | ... | 92 | 93 | 94 | | 96 | 97 | 98 | ... 117 > | ||||

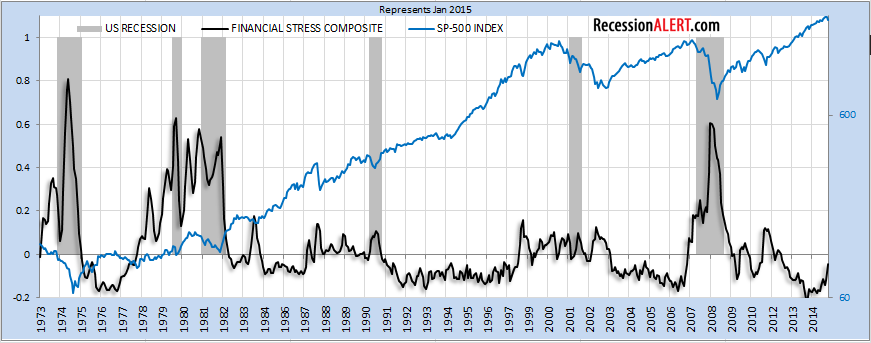

It is evident that the rise of the Financial Stress Composite above zero is a long-leading indicator for economic recession, but it also signifies a period of stock market volatility punctuated by frequent incidences of nasty stock market corrections. It is also clear that sustained periods when the Financial Stress Composite is below zero are mostly accompanied by low volatility U.S stock market “melt-ups”, with the recent 2012 to 2015 melt-up accompanied by historically low financial stress, being no exception.

It is probably premature to hit the panic button now. Also, a rise of the Financial Stress Composite above zero does not necessarily mean stock market gains are not possible, it just means that those gains are most likely going to come attached with considerable volatility, against a background of heightened risk for a non-trivial correction.

Optionen

Angehängte Grafik:

stress.png (verkleinert auf 58%)

stress.png (verkleinert auf 58%)

Die Arbeitnehmer können Dank einer guten Konjunktur sehr hohe Lohnsteigerungen durchsetzen,die die Firmen jedoch nicht mehr in Form von höheren Preisen für die produzierten Güter und Dienstleistungen weiterreichen können. Um die Gewinne dennoch zu steigern bleibt nur die Steigerung der Produktivität. Dies führt idR zu Personalabbau.

In der Folge trifft ein entweder gleich großes oder größeres Angebot auf eine schwächere Nachfrage. Preise sinken und die Gewinne ebenfalls.

Angehängte Grafik:

yardeni.png (verkleinert auf 41%)

yardeni.png (verkleinert auf 41%)

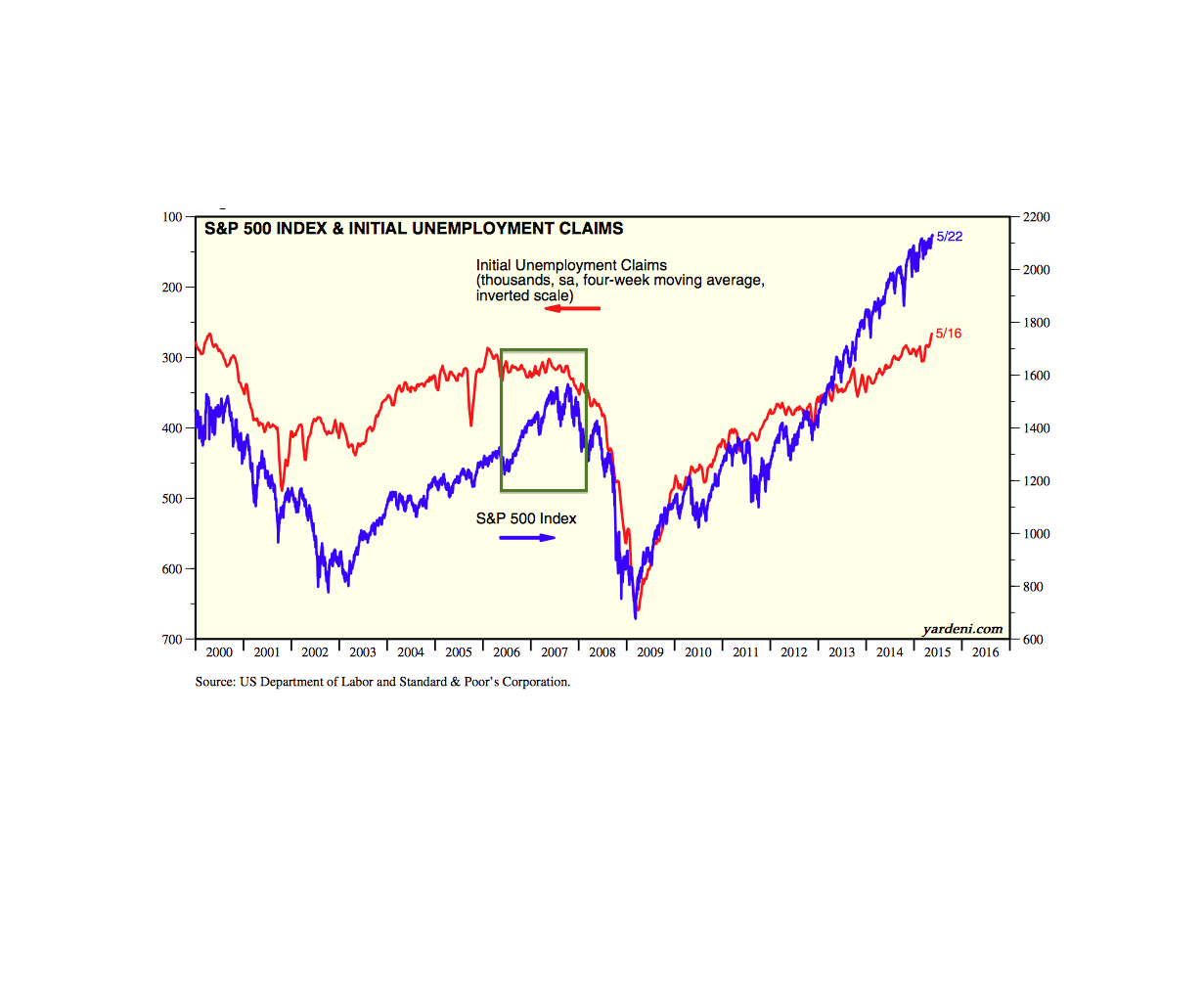

Wenn es so weiter geht, sehe ich auch für Aktien etwas schwärzer.

Aktuell sehe ich zwar noch keinen Crash, aber wenn Anleihen in den nächsten Wochen weiter so drastisch fallen, sehen Aktien im direkten Vergleich nicht mehr so günstig aus.

www.daxtrend.blogspot.de

To understand U.S. federal debt, you first must understand money, specifically the dollar. There is no physical entity called a “dollar.” You never have seen, smelled, touched or tasted a dollar. In today’s economy, a dollar is nothing more than a number in an accounting balance sheet.

The dollar bill in your wallet is not a dollar; it is a title to a dollar. It merely is evidence you own a dollar, much like a house title is evidence you own a house, or a car title is evidence you own a car or a patent is evidence you own an invention.

But unlike a house or a car, a dollar is no more physical than is, for instance, the number six. Although the number six and a dollar are real, you can’t see, smell, touch or taste either of them.

Is it possible to own something that is not physical? Consider a copyright. It demonstrates ownership of a book. But that book is not a physical thing. If I go to a store and I buy your book, who owns the book? I own the physical representation of the book, but your copyright gives you ownership of the non-physical book.

DOLLARS ARE ONLY NUMBERS

Your bank checking account and savings account do not contain dollars. They contain numbers that tell how many dollars you own.

Imagine you are one of the lucky employed, and you have a bank checking account and a bank saving account. Today, your boss gives you your first paycheck: $1,000. What exactly has your boss given you? Money? No, that paycheck is not money.

That paycheck is a set of instructions to your bank, telling your bank to increase the number in your checking account by 1,000. So, for instance, if your checking account number had read 3,476, now that number reads 4,476.

Although for convenience, you might say you now have 4,476 dollars in your checking account, you really have nothing in your checking account but the number, 4,476.

Let’s say you give someone your check for 3,000 dollars. Your check instructs your bank to reduce the number in your account by 3,000 and to increase the number in your creditor’s checking account by the same amount. Although, for convenience, you say you have transferred dollars from your account to your creditor’s account, there really has been no transfer. It’s just that your bank has reduced the number in your account and your creditor’s bank has increased the number in his account.

DOLLAR TRANSFER IS AN ILLUSION

When you wait at a railroad crossing, you see a red light moving back and forth, back and forth. Except the red light really isn’t moving. It’s two lights that blink alternately, and give the illusion of motion, an illusion so powerful that though you know it’s a illusion, you won’t be able to see it as two lights, blinking alternately. Try it.

Similarly, the illusion that dollars move from one account to another is so powerful, we all (including me) talk about dollars moving. But dollars, being non physical, cannot move.

Let’s say that the number in your checking account is 4,476, and you write a check for 6,000 (i.e. send instructions to reduce your account, and increase your creditor’s account by 6,000) Your creditor’s bank will follow your instructions, and increase his checking account number by 6,000. Then his bank will route the check to your bank for “clearing.” But, because your checking account number is too small, your instructions won’t “clear,” and your bank will return the check to your creditor’s bank, i.e the check will “bounce.” Your creditor’s account will be reduced 6,000.

ALL BANK DEPOSITS ARE BANK DEBTS

When you deposit dollars in your bank accounts, you actually lend to your bank. Those dollars are loans, not gifts. Your bank owes you those dollars, and if you want them, your bank is obligated to give them back to you. If you tell your bank you want the dollars in your savings account transferred to your checking account, will this be a problem for your bank? No, your bank simply will debit your savings account and credit your checking account.

By depositing dollars into your checking or savings account, you have forced your bank into debt. All bank deposits are bank debts. Banks love to be in debt. They actively solicit debts (deposits). Being in debt is the mission of a savings bank.

Bank deposits are not “unsustainable,” nor do they cause bankruptcies. Though a bank can become bankrupt, the fault is not deposits, but rather poor business practices. No bank ever went bankrupt because its deposits were too large.

ALL FEDERAL DEBTS ARE BANK SAVINGS ACCOUNTS

All federal debt is just the total of T-security deposits (T-bills, T-notes, T-bonds) in accounts at the Federal Reserve Bank (FRB).

Today, the total federal debt is about 12 trillion dollars. This means the total of deposits in T-security accounts at the Federal Reserve Bank, is about 12 trillion dollars. When you buy a T-bond, you “lend” dollars to the Federal Reserve Bank. You deposit dollars into your T-bond account at the FRB. You are a creditor to the FRB.

Your T-security account at the FRB is essentially identical with your savings account at your local bank. You put dollars in (credit); you take dollars out (debit), and meanwhile you earn a bit of interest.

Whenever you want your dollars back from your “loan,” you merely wire or mail instructions to the FRB to reduce the number in your T-bond savings account, and increase the number in your checking account. The FRB can do this all day long, in any amount. It’s a simple exchange of existing balances.

WHAT IF OUR CREDITORS WANT THEIR MONEY BACK?

Debt hawks worry about what will happen if all our creditors – China, Japan, European nations et al – suddenly want their dollars back. No problem. The FRB simply would debit all their T-security accounts and credit all their checking accounts. Instantly, all federal debt would disappear.

So, why can’t you and I pay off our loans that way? Why are our debts a burden to us, while the FRB’s debts are not a burden to the federal government?

There is a fundamental difference between a loan and a deposit. You aren’t the Federal Reserve Bank. When you borrow, you are not accepting a deposit. If someone lends you dollars, he is not opening a savings or checking account with you.

You borrow in order to spend, so if your creditor wants his money back, you may have spent it. But the FRB does not spend depositors’ dollars. It holds 100% of those dollars in T-security accounts. The FRB always can debit T-security accounts and credit checking accounts. There never has been a time when the FRB was unable to credit checking accounts, and there never will be.

So to all you people who worry that the federal debt is too large, the debt/GDP ratio is too large, the debt is “unsustainable,” China “owns” us, or somehow the U.S. government will not be able to pay its debts, I have some good news. The FRB could pay off 100% of all federal debt tomorrow, simply by transferring already existing dollars from T-security savings accounts to checking accounts.

If you are a lender to the federal government, your money is all there, right in your T-security account at the FRB. All of it. Every cent. So is China’s money, Europe’s money, Japan’s money – every one of those 12 trillion dollars of federal “debt,” all sit safely in FRB T-security accounts.

And despite what the fear mongers tell you, you don’t owe a penny of it. Nor do your children, nor do your children’s children. The FRB owes it all, and it’s all there in T-bill accounts.

So stop worrying about the size of the federal debt. Stop worrying that the U.S. Federal Reserve Bank has too many dollars on deposit. It’s not possible for the FRB to have too many dollars on deposit.

WHY DOES THE GOVERNMENT BORROW DOLLARS?

It doesn’t. It allows interest paying deposits in T-security accounts at the FRB. Why then, does the federal government issue T-securities? It’s an obsolete process based on an obsolete law that, very simply says: The total of T-securities issued each year, must equal each year’s total federal deficit.

Not that there is any functional relationship between deficits and T-security accounts (There isn’t.) It’s just that by law the two numbers must be equal. So, for instance, if the federal government spends $10 million and receives only $3 million in taxes, it runs a $7 million deficit, and is required by law to issue $7 million worth of T-securities, though T-securities have no relationship to deficits.

It’s almost like having a law stating for every car there also must be a horse – a meaningless relationship.

Years ago, there was a reason for this strange law, but no more. Change the law, and the government could run that deficit without issuing a single T-security. The dollars in T-security accounts are not used for federal spending. They just sit there, at the FRB, waiting to be paid back.

WHY ARE GREECE AND ILLINOIS GOING BROKE?

The U.S. “debt” is 100% in dollars, our sovereign currency. Being the sovereign creator of dollars (aka Monetarily Sovereign), we never can run short of dollars. So anyone wanting dollars from the FRB, will have no trouble getting them. The U.S. does not spend the dollars it “borrows.” Those dollars are kept in T-security accounts at the FRB.

When the U.S. spends, it send instructions to creditors’ banks to increase the dollar numbers in those banks. These instructions are cleared by the FRB. This is how the U.S. government creates dollars.

But Greece and Illinois are monetarily non-sovereign. They do not have a sovereign currency. Greece uses euros, which it does not have the power to create. It cannot store borrowed euros in its central bank. Greece needs to spend the euros it receives from borrowing.

Illinois too, uses dollars, but dollars are not its sovereign currency. Like Greece, Illinois has no sovereign currency. It spends the dollars it borrows, rather than being able to store them in a bank account.

BOTTOM LINE

Federal debt is not like non-federal debt. Same word; two different meanings. Federal debt is the total of deposits in T-security accounts at the Federal Reserve Bank. The Federal Reserve Bank has more that $12 trillion in deposits. Many private banks have billions in deposits.

Bank deposits are a sign of strength, not weakness.

Federal “debt” is a myth, promulgated by people whose agenda is to reduce federal spending for the poor and middle classes. Pay no attention to these evil people. Growing federal debt is a sign of strength, not weakness.

http://mythfighter.com/2012/10/23/...l-debt-a-primer-for-politicians/

Optionen

Cash, in a brokerage account or any account, is always an asset and a liability. Physical cash, the type you have in your wallet, is a liability of the US government and an asset for the holder. Cash, on a corporate balance sheet or a brokerage account isn’t physical cash. It is usually just short-term liabilities like Treasury Bills or Money Market funds made up of short duration debt instruments. This “cash” account is made up of instruments that are always someone’s asset and liability just like physical cash. T-bills, for instance, are a liability of the US government and an asset of the holder. So, when “cash” balances rise so too do both the asset side of the balance sheet and the liability side of the balance sheet. We can’t talk about “cash” assets increasing in the economy without also acknowledging that this necessarily means the liabilities have also increased. An increase in cash (usually as a result of borrowing) can be both good and bad depending on its use.

When someone says there is “cash on the sidelines” they are generally misunderstanding both the accounting described above and the transactional dynamics that occur in markets. For instance, when you decide to buy stocks you are also deciding to sell your cash. In a brokerage account this actually means that your short duration instrument (called cash) is being sold and exchanged for the stock. So, you are buying stock, but someone else is buying your cash. This results in a clean swap of financial assets. There isn’t more or less cash on the sidelines after this transaction. There is the exact same amount of cash on the sidelines before and after this transaction.

Of course, the price that is arrived at during the course of this transaction is a function of the eagerness of the buyer and seller to transact. If you have $100 in cash and are very eager to buy $90 worth of stock, but I am holding $95 worth of stock and am not eager to sell then you might be more inclined to purchase my stock for $95 than I will be eager to sell it at $90. Although the quantity of cash relative to stocks is a factor in driving demand for stocks it is not the dominant factor that drives value. That, after all, is a function of profits.*

Importantly, cash levels can rise as a function of balance sheet expansion. If I take out a loan my cash/deposit balances will increase. So too will my liabilities (the loan). And while this might give me more purchasing power to buy stocks it does not necessarily mean that prices must move higher because, as I described above, the sellers might actually be more eager to sell than the buyer’s eagerness to buy. So, next time you hear the “cash on the sidelines” myth remember that it’s important to maintain the right context. If you don’t you might be fooled into thinking that this is a necessarily bullish or bearish argument when it’s not.

* A good way to think about this is to consider what happens when a corporation implements a stock buyback. Let’s say company A has 100 shares outstanding and earns $100 in year 1. In year 2 they decide to buyback 10 of those shares, but they earn the same $100. This should boost the value of the stock because the current outstanding shares are worth more per share. There is, in essence, more money per share in this case if we assume that the quantity of cash in the system has not changed (because there are fewer shares for that cash to bid on). But consider this alternative. Let’s say the company buys back 10 shares and earnings fall to $50 because the company employees decide to go on vacation for 6 months. In this case the number of shares has fallen relative to year 1, but the value of those shares has actually declined even though the quantity of money relative to outstanding shares has increased. This means the price of the stock will very likely decline even though the quantity of money relative to outstanding stock has increased.

http://www.pragcap.com/...-on-the-sidelines-myth-is-still-haunting-us

Optionen

und was machen die ostschweizer bogenschützen?

schweigen... aktuell keine hilfe.

Optionen

Angehängte Grafik:

image.jpg (verkleinert auf 85%)

image.jpg (verkleinert auf 85%)

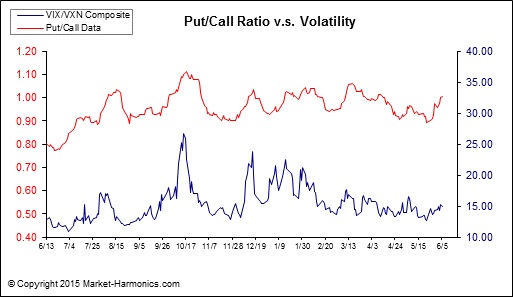

v.a. ist die p/c ratio oft früh dran, konnte man zuletzt wiederholt beobachten

Optionen

Angehängte Grafik:

image.jpg (verkleinert auf 99%)

image.jpg (verkleinert auf 99%)

Optionen

Optionen

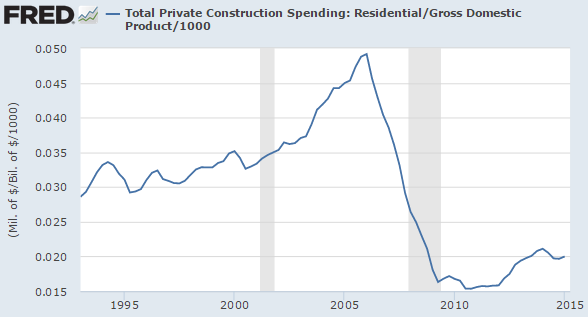

Angehängte Grafik:

residential_construction_spending_as_percentage....png (verkleinert auf 86%)

residential_construction_spending_as_percentage....png (verkleinert auf 86%)

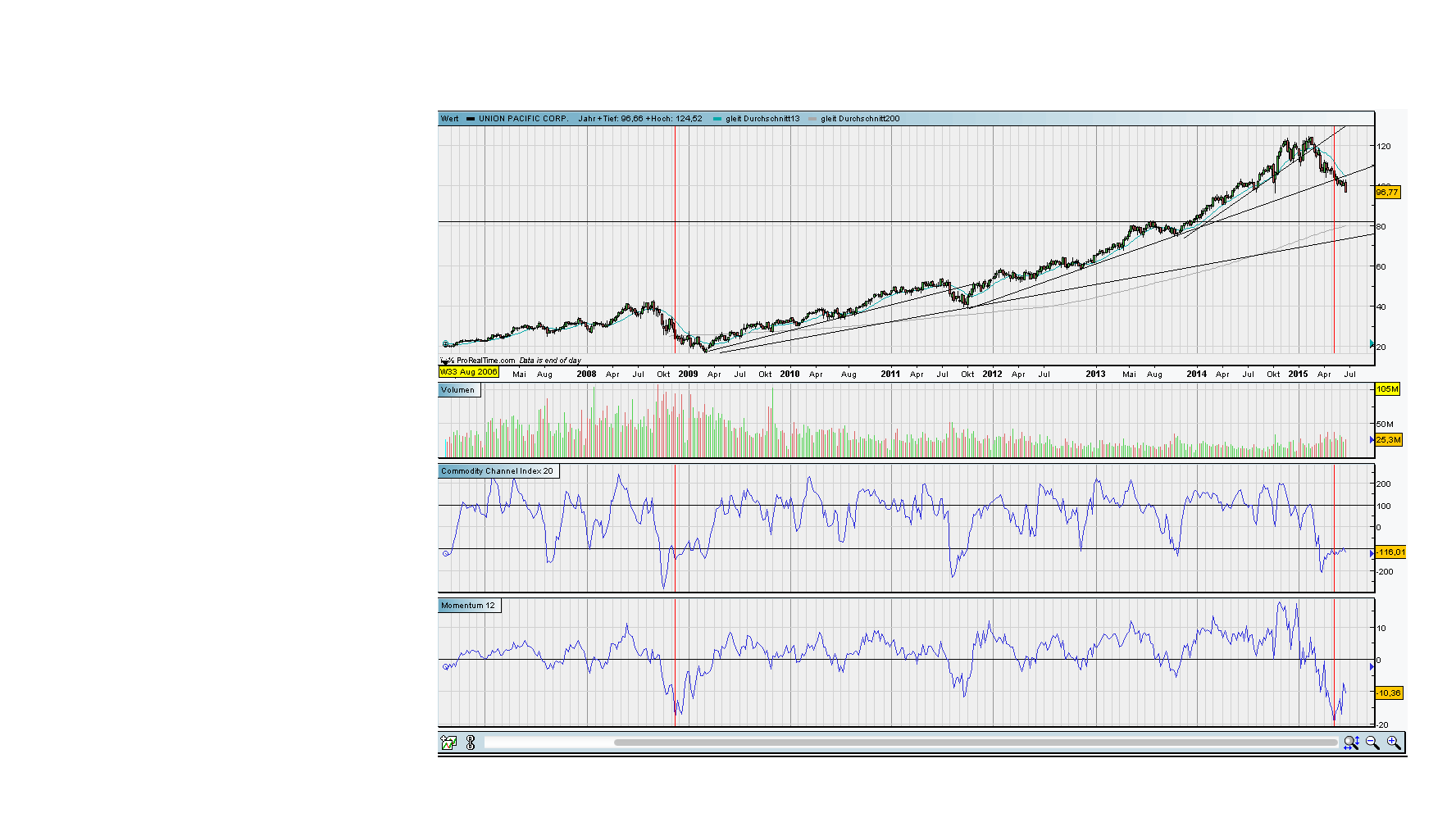

Mitgebracht habe ich den Chart von Union Pacific, der Aktie mit dem perfekten Up-Trend! Dieser ist erst einmal gebrochen was sich ja auch im Tran spiegelt. Langfristig bedeutet das jedoch noch nichts. Könnte jetzt auch seitwärts laufen.

Vom Momentum her könnte es noch ne Weile so weiter gehen, wenn man 2008/9 als Blaupause nimmt. Natürlich bin ich nicht Short. Bin zur Zeit wenig aktiv.

Angehängte Grafik:

union_pacific.png (verkleinert auf 28%)

union_pacific.png (verkleinert auf 28%)

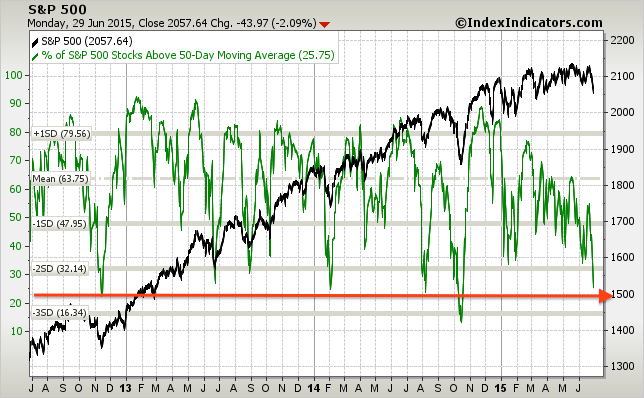

Angehängte Grafik:

sp500-vs-sp500-stocks-above-50d-sma-params-....png (verkleinert auf 79%)

sp500-vs-sp500-stocks-above-50d-sma-params-....png (verkleinert auf 79%)

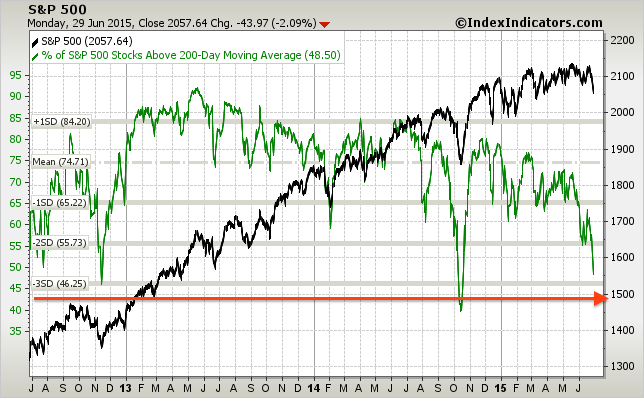

Angehängte Grafik:

sp500-vs-sp500-stocks-above-200d-sma-params-....png (verkleinert auf 79%)

sp500-vs-sp500-stocks-above-200d-sma-params-....png (verkleinert auf 79%)

Aufgrund der negativen Erwartungen und den Stand der Indikatoren habe ich eine Spielposition auf Long gesetzt. Kann natürlich auch in die Hose gehen, da Trades in solch politischen Umfeld kein besseres CRV als 50% haben.

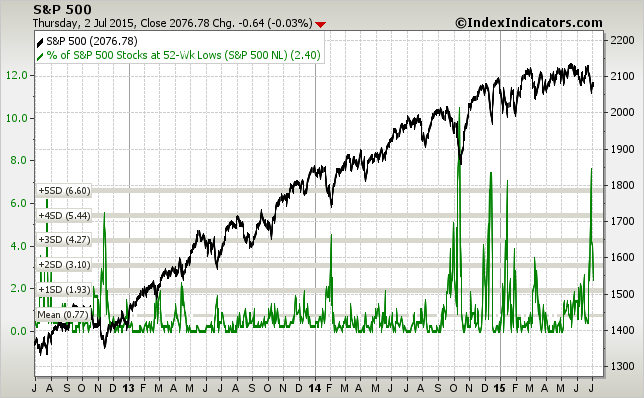

Anbei die 52-Wk Lows, die bei der Annahme, dass wir uns weiterhin im Hausse-Modus befinden, ihren Spike gesehen haben könnten.

Angehängte Grafik:

sp500-vs-sp500-stocks-new-lows-params-3y-x-....png (verkleinert auf 79%)

sp500-vs-sp500-stocks-new-lows-params-3y-x-....png (verkleinert auf 79%)

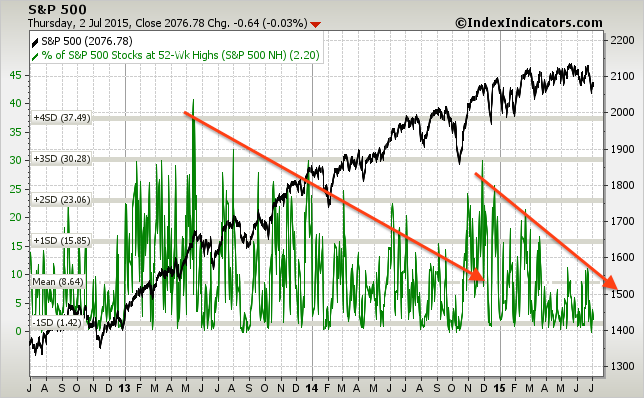

Ob bei den aktuell schwachen Makrodaten neue Hochs erreicht werden können ist jedoch sehr fragwürdig. Vielleicht bei den Amis?!

Angehängte Grafik:

sp500-vs-sp500-stocks-new-highs-params-3y-x-....png (verkleinert auf 79%)

sp500-vs-sp500-stocks-new-highs-params-3y-x-....png (verkleinert auf 79%)

Angehängte Grafik:

nasdaq-vs-nyse-stocks-above-200d-sma-params-....png (verkleinert auf 79%)

nasdaq-vs-nyse-stocks-above-200d-sma-params-....png (verkleinert auf 79%)

Angehängte Grafik:

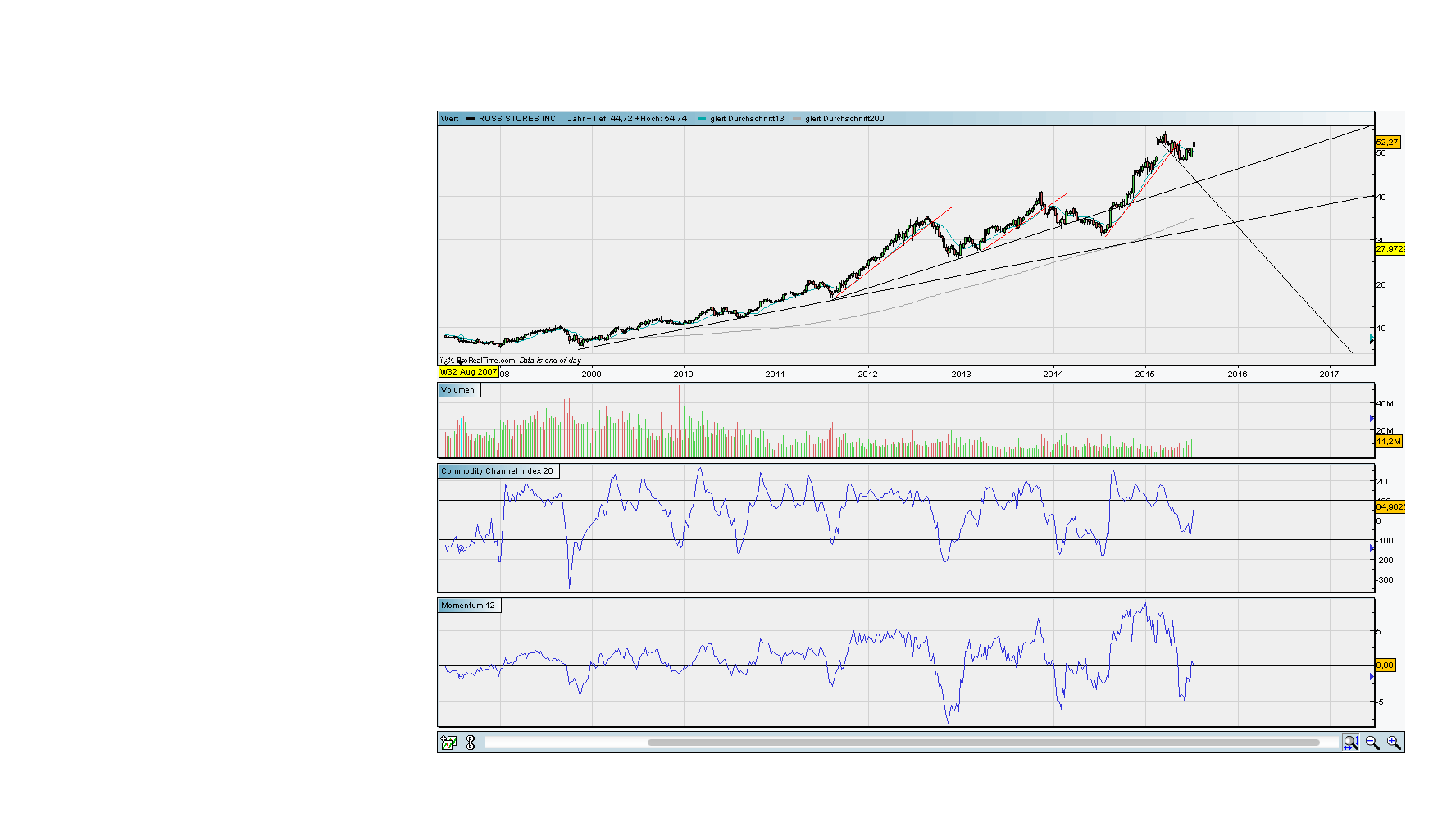

ross_stores.png (verkleinert auf 28%)

ross_stores.png (verkleinert auf 28%)

Angehängte Grafik:

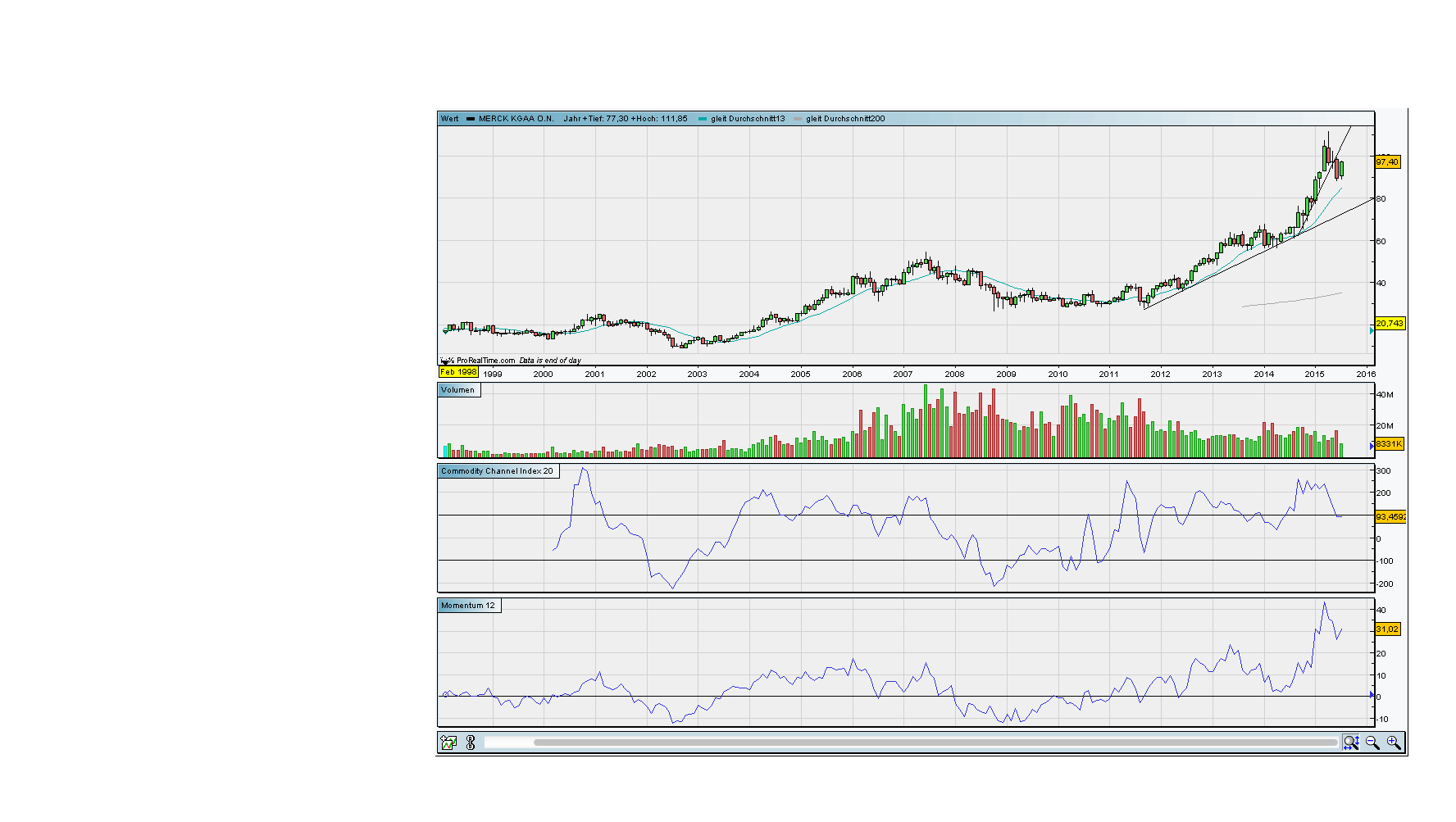

merk.png (verkleinert auf 28%)

merk.png (verkleinert auf 28%)

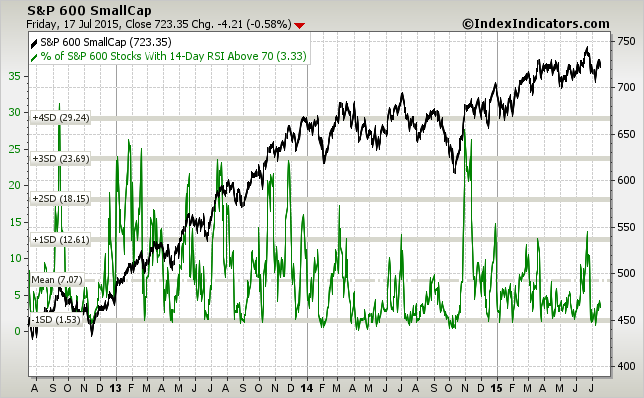

Bedeutet, dass es immer weniger Firmen gelingt die Erwartungen zu erfüllen oder zu übertreffen. Ist bei einem reifen Markt eine logische Entwicklung und begrenzt das Potenzial des laufenden Bullenmarktes.

Angehängte Grafik:

sp600-vs-sp600-stocks-above-200d-sma-params-....png (verkleinert auf 79%)

sp600-vs-sp600-stocks-above-200d-sma-params-....png (verkleinert auf 79%)

Angehängte Grafik:

sp600-vs-sp600-stocks-14d-rsi-above-70-....png (verkleinert auf 79%)

sp600-vs-sp600-stocks-14d-rsi-above-70-....png (verkleinert auf 79%)

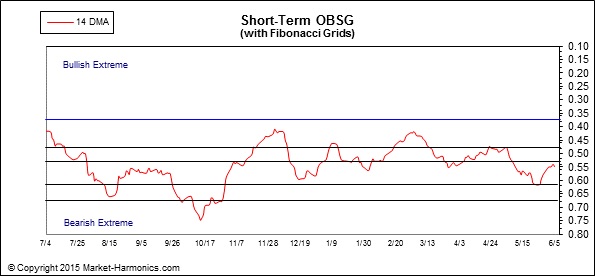

Das Risiko für long ist aktuell eher geringer als für short:

Optionen

Angehängte Grafik:

obsglong.gif (verkleinert auf 85%)

obsglong.gif (verkleinert auf 85%)

Dieses Jahr fing schon nicht gut an und es bleibt bisher wie es angefangen hat.

Ich sollte mal ein paar Schritte zurücktreten und etwas sortieren.

Den Markt kann ich gar nicht einschätzen, weshalb ich so gut wie keine Derivate anpacke. Bei Aktien kann man besser langfristig arbeiten. Weniger Druck!

Wenn dieEM´s nicht irgendwann aus dem extremen Tief herauskommen, hätte ich ohne dies mit Zitronen gehandelt.

The Austrian business cycle theory (ABCT) is an economic theory developed by the Austrian School of economics about how business cycles occur. The theory views business cycles as the consequence of excessive growth in bank credit, due to artificially low interest rates set by a central bank or fractional reserve banks.[1] The Austrian business cycle theory originated in the work of Austrian School economists Ludwig von Mises and Friedrich Hayek. Hayek won the Nobel Prize in economics in 1974 (shared with Gunnar Myrdal) in part for his work on this theory.[2][3]

Proponents believe that a sustained period of low interest rates and excessive credit creation result in a volatile and unstable imbalance between saving and investment.[4] According to the theory, the business cycle unfolds in the following way: Low interest rates tend to stimulate borrowing from the banking system. It is argued that this leads to an increase in capital spending funded by newly issued bank credit. Proponents hold that a credit-sourced boom results in widespread malinvestment. In the theory, a correction or "credit crunch" – commonly called a "recession" or "bust" – occurs when the credit creation has run its course. Then the money supply contracts, causing resources to be reallocated back towards their former uses.

Austrian business cycle theory states that distortions in the availability of credit are the cause of business cycles. The Austrian explanation of the business cycle differs significantly from the mainstream understanding of business cycles and is generally rejected by mainstream economists.

Malinvestment and “boom”[edit]

According to ABCT, a period of "malinvestment" is caused by a period of excessive business lending by banks, and this credit expansion is later followed by a sharp contraction and period of distressed asset sales (liquidation) which were purchased with such bank credit.[citation needed][5] The initial expansion is believed to be caused by fractional reserve banking issuance excessive loans at interest rates below what full reserve banks would demand for such loans. Due to the availability of relatively inexpensive funds, entrepreneurs invest in capital goods for more roundabout, "longer process of production" technologies. Borrowers take their newly acquired funds and purchase new capital goods, thereby causing an increase in the proportion of aggregate spending allocated to capital goods rather than consumer goods. Austrian economists further contend that such a shift is unsustainable due to mispricing caused by excessive credit creation by the banks and must reverse itself eventually as it is always unsustainable. Proponents of the theory conclude that the longer the increased proportion of spending in capital goods industries continues, the more violent and disruptive will be the necessary re-adjustment process. Economist Bryan Caplan has examined ABCT and Caplan denies that the shift must reverse itself or "that the artificially stimulated investments have any tendency to become malinvestments".[6]

Austrians argue that a boom taking place under these circumstances is actually a period of wasteful malinvestment. "Real" savings would have required higher interest rates to encourage depositors to save their money in term deposits to invest in longer term projects under a stable money supply. According to Mises's work, the artificial stimulus caused by bank lending causes a generalized speculative investment bubble which is not justified by the long-term factors of the market.[5][not specific enough to verify]

“Bust”[edit]

Mises wrote that a "crisis" (or "credit crunch") arrives when the consumers come to reestablish their desired allocation of saving and consumption at prevailing interest rates.[7][8] Mises conjectured that the "recession" or "depression" is actually the process by which the economy adjusts to the wastes and errors of the monetary boom, and reestablishes efficient service of sustainable consumer desires.[7][8][not specific enough to verify]

Austrians argue that continually expanding bank credit can keep the artificial credit-fueled boom alive (with the help of successively lower interest rates from the central bank). In the theory, this postpones the "day of reckoning" and defers the collapse of unsustainably inflated asset prices.[7][9]

Austrians argue that the monetary boom ends when bank credit expansion finally stops – when no further investments can be found which provide adequate returns for speculative borrowers at prevailing interest rates. They further argue that the longer the "false" monetary boom goes on, the bigger and more speculative the borrowing, the more wasteful the errors committed and the longer and more severe will be the necessary bankruptcies, foreclosures, and depression readjustment.[7][not specific enough to verify]

Government policy error[edit]

Austrian business cycle theory does not argue that fiscal restraint or "austerity" will increase economic growth or result in recovery.[10] Rather, they argue that the alternatives will make eventual recovery more difficult and unbalanced. All attempts by central governments to prop up asset prices, bail out insolvent banks, or "stimulate" the economy with deficit spending will only make the misallocations and malinvestments more acute and the economic distortions more pronounced, prolonging the depression and adjustment necessary to return to stable growth.[10] Austrians argue the policy error rests in the government's (and central bank's) weakness or negligence in allowing the "false" unsustainable credit-fueled boom to begin in the first place, not in having it end with fiscal and monetary "austerity". Debt liquidation is therefore the only solution to a debt-fueled problem.[11][12]

According to Ludwig von Mises:[7]

There is no means of avoiding the final collapse of a boom brought about by credit expansion. The alternative is only whether the crisis should come sooner as a result of the voluntary abandonment of further credit expansion, or later as a final and total catastrophe of the currency system involved.

The role of central banks[edit]

Austrians generally argue that inherently damaging and ineffective central bank policies, including unsustainable expansion of bank credit through fractional reserve banking, are the predominant cause of most business cycles, as they tend to set artificial interest rates too low for too long, resulting in excessive credit creation, speculative "bubbles", and artificially low savings.[13] Under fiat monetary systems, a central bank creates new money when it lends to member banks, and this money is multiplied many times over through the money creation process of the private banks. This new bank-created money enters the loan market and provides a lower rate of interest than that which would prevail if the money supply were stable.[5][14]

The Austrian theory is considered one of the precursors to the modern credit cycle theory, which is emphasized by Post-Keynesian economists, economists at the Bank for International Settlements. These two emphasize asymmetric information and agency problems. Henry George, another precursor, emphasized the negative impact of speculative increases in the value of land, which places a heavy burden of mortgage payments on consumers and companies.[39][39][40]

A different theory of credit cycles is the debt-deflation theory of Irving Fisher.

In 2003 Barry Eichengreen laid out a credit boom theory as a cycle in which loans increase as the economy expands, particularly where regulation is weak, and through these loans money supply increases. Inflation remains low, however, because of either a pegged exchange rate or a supply shock, and thus the central bank does not tighten credit and money. Increasingly speculative loans are made as diminishing returns lead to reduced yields. Eventually inflation begins or the economy slows, and when asset prices decline, a bubble is pricked which encourages a macroeconomic bust.[39]

In 2006 William White argued that "financial liberalization has increased the likelihood of boom-bust cycles of the Austrian sort" and he has later argued the "near complete dominance of Keynesian economics in the post-world war II era" stifled further debate and research in this area.[41][42] While White conceded that the status quo policy had been successful in reducing the impacts of busts, he commented that the view on inflation should perhaps be longer term and that the excesses of the time seemed dangerous.[42] In addition, White believes that the Austrian explanation of the business cycle might be relevant once again in an environment of excessively low interest rates. According to the theory, a sustained period of low interest rates and excessive credit creation results in a volatile and unstable imbalance between saving and investment.[4][42]

wiki