against all odds

Seite 81 von 117 Neuester Beitrag: 08.04.20 16:14 | ||||

| Eröffnet am: | 22.03.13 19:18 | von: Fillorkill | Anzahl Beiträge: | 3.904 |

| Neuester Beitrag: | 08.04.20 16:14 | von: Fillorkill | Leser gesamt: | 340.101 |

| Forum: | Börse | Leser heute: | 36 | |

| Bewertet mit: | ||||

| Seite: < 1 | ... | 78 | 79 | 80 | | 82 | 83 | 84 | ... 117 > | ||||

Wichtiger als der Gewinn ist zu lernen, welche Strategien zu einem passen und ob diese grundsätzlich einen positiven Erwartungswert haben. Dann kann man auch mit relativ kleinen Einsatz ansehnliche Renditen erwirtschaften.

So kann man ganz gut die Zeit bis zum All-Inn-Einsatz überbrücken.

Aktuell nähern wir uns übrigens wieder meinem Wunschszenario, dem temporär erfolgreichen Ausbruchsversuch nach oben. OBSG sollte in dieser Woche anziehen:

Optionen

Angehängte Grafik:

obsgshort.gif (verkleinert auf 85%)

obsgshort.gif (verkleinert auf 85%)

Früher hatte ich noch keine Werkzeuge und die entsprechende Erfahrung, um längerfristig an Positionen festzuhalten. Das hat sich verändert. Allerdings betreffen diese Werkzeuge eher die Longseite, die man allerdings unter anderen Vorzeichen im Bärenmarkt nutzen könnte. Nur der Bärenmarkt ist noch nicht da.

Optionen

Optionen

Angehängte Grafik:

japan-quo-vadis_2.png

japan-quo-vadis_2.png

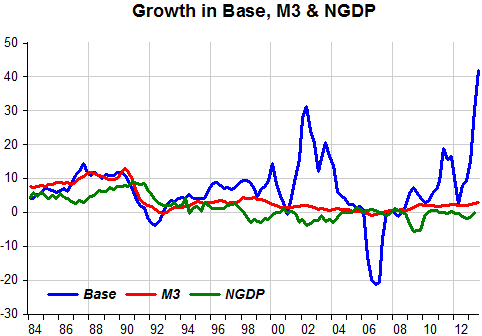

Based on the historic patterns of the unemployment rate indicators prior to recessions one can reasonably conclude that the U.S. economy is not likely to go into recession anytime soon.

Optionen

Angehängte Grafik:

fig-1.gif (verkleinert auf 51%)

fig-1.gif (verkleinert auf 51%)

http://www.gold-action.de/mitmachen.html

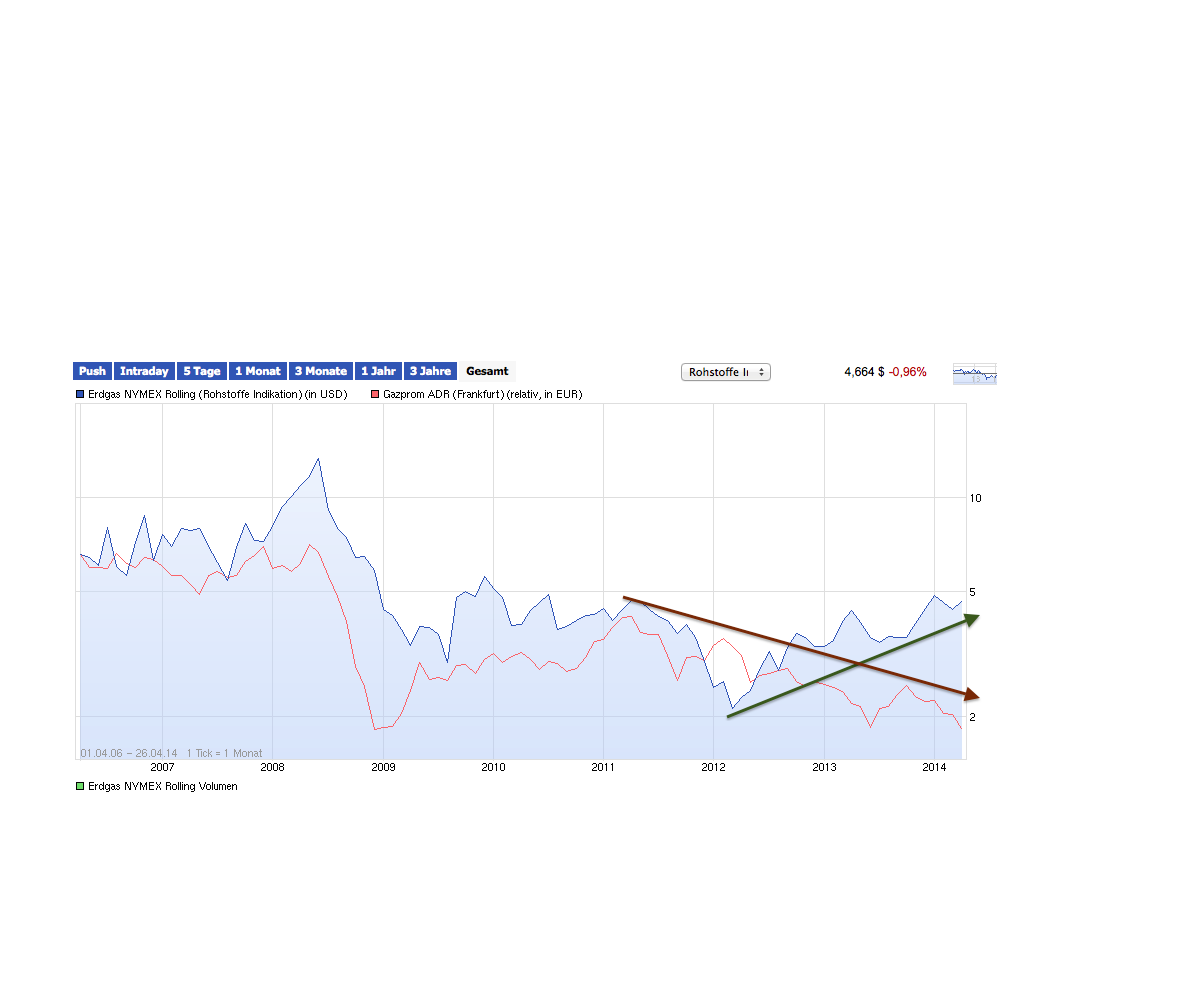

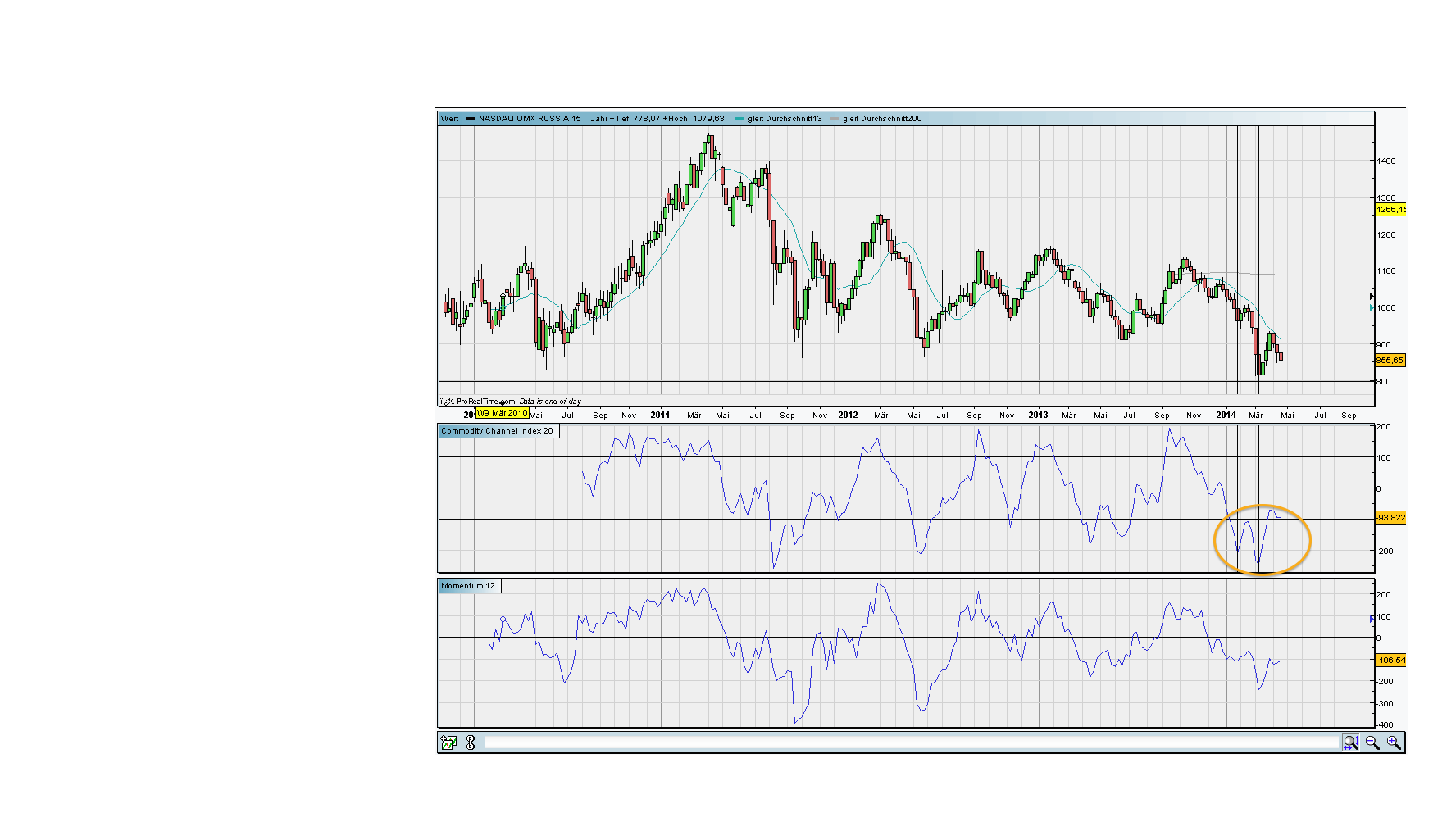

Die Herde hat sich aus Russland anscheinend langsam verabschiedet, was man angesichts der rechtlichen Unsicherheiten in Russland sogar nachvollziehen kann.

Trotzdem frage ich mich, ob es nicht schon bald Sinn macht hier antizyklisch zu handeln.

Angehängte Grafik:

bildschirmfoto_2014-04-26_um_21.png (verkleinert auf 42%)

bildschirmfoto_2014-04-26_um_21.png (verkleinert auf 42%)

Optionen

The main thrust of the heterodox “story” over the last 5 years is that mainstream economists misunderstood clear operational realities of the monetary system and in doing so, they failed to understand both the crisis as well as the fixes. Take, for instance, Paul Krugman’s own positions in recent years:

As late as 2011 Dr. Krugman didn’t understand why Japanese bond yields were low relative to Italian bond yields despite the massive debt loads in each nation. Some heterodox economists, like Warren Mosler, Wynne Godley and myself had been pointing out for years beforehand that there was a distinct operational difference between a country which issues its own currency in a truly autonomous currency area versus a nation like Italy which has effectively rendered itself a currency user. This was a MASSIVELY important understanding that has contributed to substantially flawed policy, politics and understandings.

Or how about 2012 when Dr. Krugman said: “First of all, any individual bank does, in fact, have to lend out the money it receives in deposits. Bank loan officers can’t just issue checks out of thin air”. This is another obvious misunderstanding about basic banking and the money multipler (which has since been soundly resolved by the Bank of England). And he wasn’t alone. This misunderstanding ran the gamut of mainstream economists.

So mainstream economists misunderstood basic banking as well as basic operational realities like monetary sovereignty. These aren’t small mistakes. They are colossal misunderstandings. And I haven’t even begun to delve into the actual errors which lead to these misunderstandings. Indeed, it is the underpinnings of Mainstream Macro which lead to these erroneous conclusions in the first place.

So none of this was about working with “the wrong story line”. We aren’t merely telling stories. We are saying explicitly, that it is the Mainstream who relies on “story lines”, “classroom gadgets” like the IS/LM model, DSGE, other models which don’t reflect reality, and base their thinking on a version of the world which looks nothing like the modern monetary system. Mainstream Economics has failed to reflect the world in which we actually live. That is why there’s a revolt against it. And it’s the failure of Mainstream Macro to conform with evolving ideas, that is leading to an increasing call for its dismissal. Some economists will go down on their ship. Others are clearly trying to evolve and embrace the views of the heterodoxy, which, for the record, have outperformed the views of all the Mainstreamers by a pretty substantial margin over the last 5 years.

Read more at http://pragcap.com/getting-the-story-wrong#f6ilUKzATRloKtp5.99

Optionen

Angehängte Grafik:

russia.png (verkleinert auf 28%)

russia.png (verkleinert auf 28%)

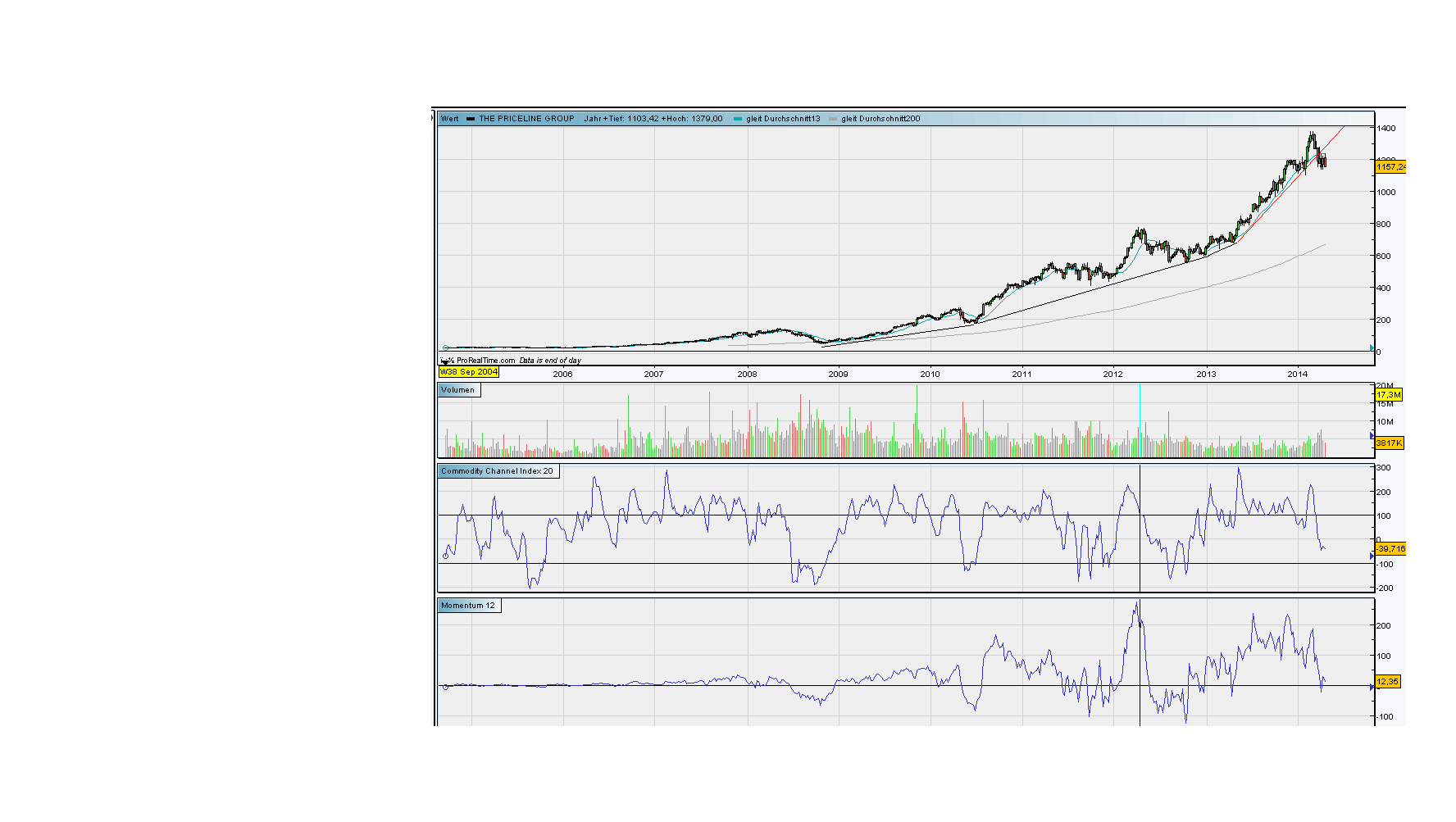

Als ersten Wert ein Momentumliebling des Marktes: Priceline

Angehängte Grafik:

priceline.png (verkleinert auf 28%)

priceline.png (verkleinert auf 28%)

Angehängte Grafik:

wynn_resort.png (verkleinert auf 28%)

wynn_resort.png (verkleinert auf 28%)

Angehängte Grafik:

ross_stores.png (verkleinert auf 28%)

ross_stores.png (verkleinert auf 28%)

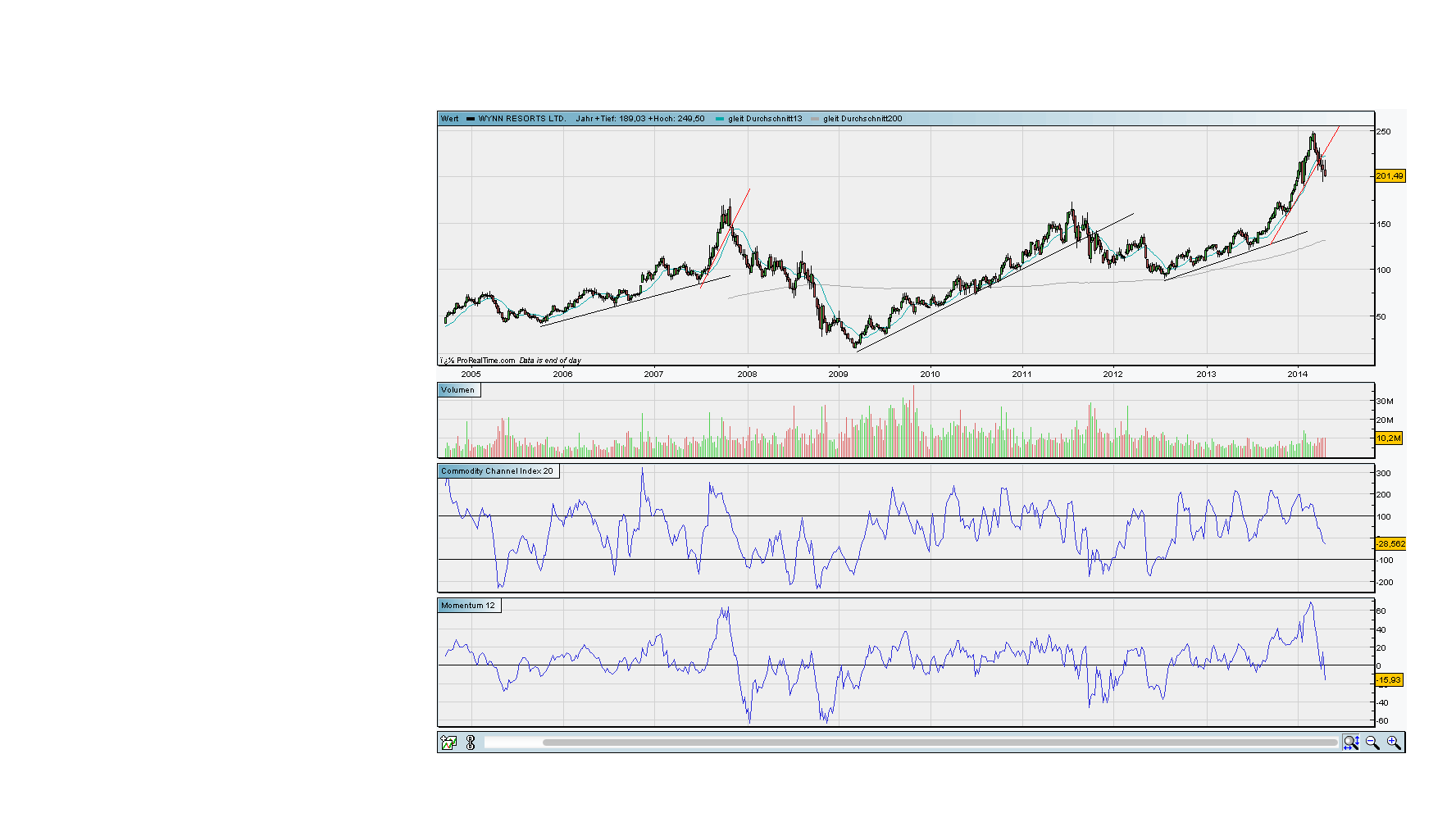

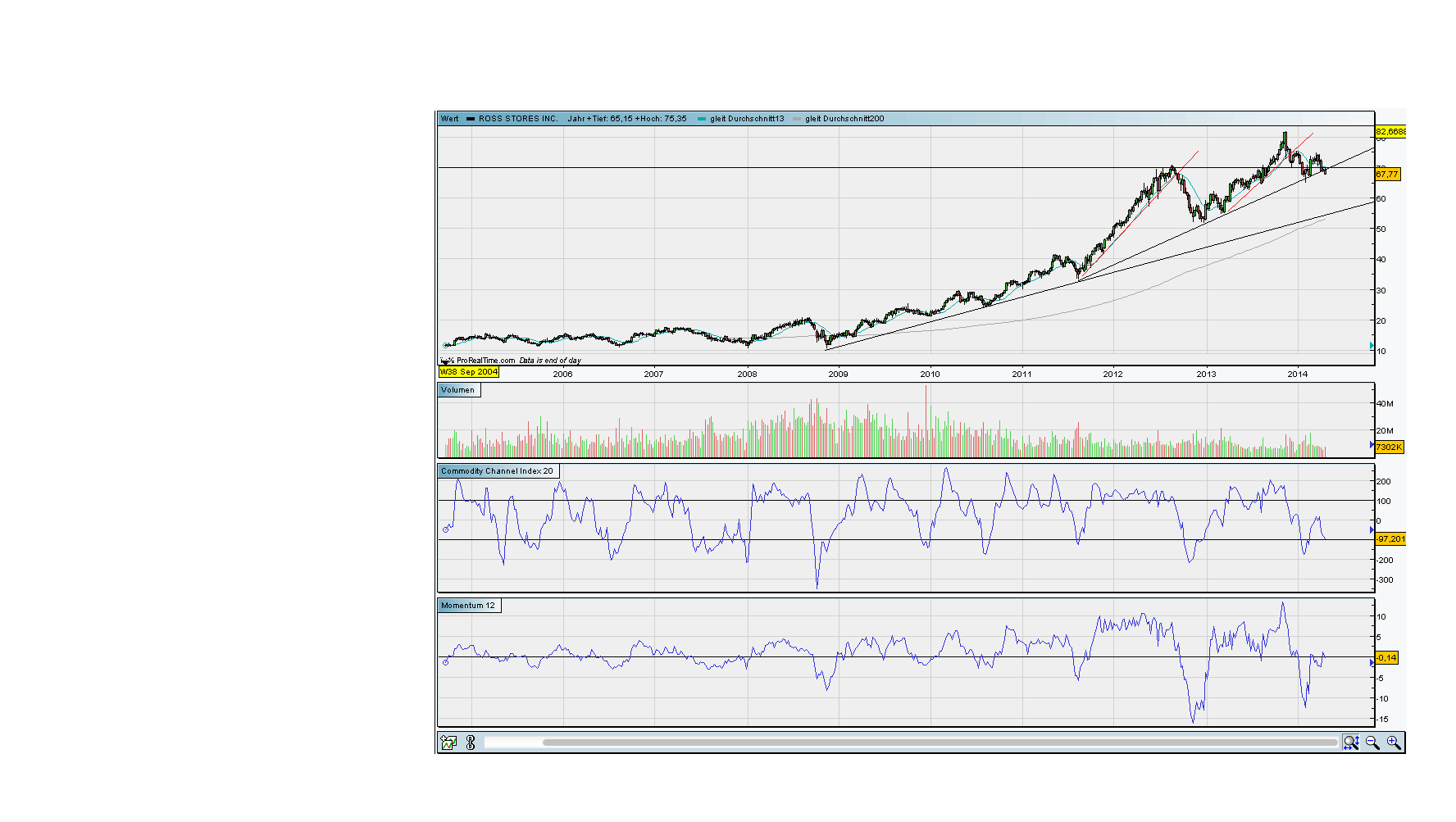

Allerdings kann man zur Zeit nicht seriös in die eine oder andere Richtung spekulieren, da der Konflikt in der Ukraine die Märkte zu jeder Zeit in jede Richtung bringen kann. Damit gibt es sowohl für Long und Short kein gutes CRV, zumindest, wenn man Derivate handelt.

Angehängte Grafik:

texas_instruments.png (verkleinert auf 28%)

texas_instruments.png (verkleinert auf 28%)