against all odds

Seite 77 von 117 Neuester Beitrag: 08.04.20 16:14 | ||||

| Eröffnet am: | 22.03.13 19:18 | von: Fillorkill | Anzahl Beiträge: | 3.904 |

| Neuester Beitrag: | 08.04.20 16:14 | von: Fillorkill | Leser gesamt: | 341.122 |

| Forum: | Börse | Leser heute: | 0 | |

| Bewertet mit: | ||||

| Seite: < 1 | ... | 74 | 75 | 76 | | 78 | 79 | 80 | ... 117 > | ||||

...After all, everyone knows that socialism is unconstitutional. It clearly contradicts the ideals of our Founding Fathers. Actually, it doesn"t. Here"s a shock. Many of our Founding Fathers were socialists. They believed that "essential" services should be provided by government to the public at large for little or no remuneration. The costs of these services would be shared by the whole. This, by most modern accounts, is socialism.

The Constitution of the United States, drafted in the summer of 1787 in Philadelphia by some of the smartest men on this side of the Pond, proves this to be true. In that cherished document, the Founding Fathers demanded socialism. Section 8 of Article I, for example, empowers Congress "To establish Post Offices and post Roads." That same Section also authorizes Congress "To raise and support Armies," and even "To provide and maintain a Navy." Although the text does not preclude privatization of these public institutions — indeed, they continue to include entrepreneurial elements to this day — the Framers understood that they would certainly have public, social elements as well. Alexander Hamilton, James Madison, George Washington, Benjamin Franklin, and John Adams — among others — all signed this document. They agreed that the new national government would facilitate communication and defense through taxation. They agreed that these essential services would not have to be purchased on the open market. They agreed that these services would not be limited to those who could pay fair market value.

The author of the Declaration of Independence, Thomas Jefferson (who skipped the Constitutional Convention in favor of traipsing off to Paris during that hot summer in 1787), also supported the fledgling Nation"s foray into socialism. Perhaps the greatest of all of America"s socialized institutions, the Nation"s modern highway system, was begun in 1806 by then-President Jefferson"s authorization of the Cumberland (National) Road. Transportation, too, was deemed to be one of the Nation"s essential services that could not be relegated to private industry.

The Congress did President Jefferson one better. It socialized the great bulk of America"s navigable waterways in the late eighteenth and early nineteenth centuries. The founding generation recognized early on that the national government needed the power regulate interstate commerce—this was written into Article I of the 1787 Constitution—and waterways provided the most important channel of commerce. The national government, using this authority, opened America"s internal waterways to commerce. These immense "social" highways proved a boon to entrepreneurial activities (and perhaps saved the Nation).

Communication, transportation and mutual defense provide only the most obvious examples of the Founding Father"s interests in socialized institutions. Contrary to some popular reports, many in the founding generation had "republican," communitarian leanings. Our forefathers were not devout disciples of Adam Smith, let alone Herbert Spencer (who in the mid-nineteenth century infamously coined the phrase, "survival of the fittest"). They were pragmatists, capitalists and socialists, willing to try whatever was necessary to insure that the American experiment did not fail...'

http://jurist.law.pitt.edu/forumy/2009/10/...ist-founding-fathers.php

The Constitution of the United States, drafted in the summer of 1787 in Philadelphia by some of the smartest men on this side of the Pond, proves this to be true. In that cherished document, the Founding Fathers demanded socialism. Section 8 of Article I, for example, empowers Congress "To establish Post Offices and post Roads." That same Section also authorizes Congress "To raise and support Armies," and even "To provide and maintain a Navy." Although the text does not preclude privatization of these public institutions — indeed, they continue to include entrepreneurial elements to this day — the Framers understood that they would certainly have public, social elements as well. Alexander Hamilton, James Madison, George Washington, Benjamin Franklin, and John Adams — among others — all signed this document. They agreed that the new national government would facilitate communication and defense through taxation. They agreed that these essential services would not have to be purchased on the open market. They agreed that these services would not be limited to those who could pay fair market value.

The author of the Declaration of Independence, Thomas Jefferson (who skipped the Constitutional Convention in favor of traipsing off to Paris during that hot summer in 1787), also supported the fledgling Nation"s foray into socialism. Perhaps the greatest of all of America"s socialized institutions, the Nation"s modern highway system, was begun in 1806 by then-President Jefferson"s authorization of the Cumberland (National) Road. Transportation, too, was deemed to be one of the Nation"s essential services that could not be relegated to private industry.

The Congress did President Jefferson one better. It socialized the great bulk of America"s navigable waterways in the late eighteenth and early nineteenth centuries. The founding generation recognized early on that the national government needed the power regulate interstate commerce—this was written into Article I of the 1787 Constitution—and waterways provided the most important channel of commerce. The national government, using this authority, opened America"s internal waterways to commerce. These immense "social" highways proved a boon to entrepreneurial activities (and perhaps saved the Nation).

Communication, transportation and mutual defense provide only the most obvious examples of the Founding Father"s interests in socialized institutions. Contrary to some popular reports, many in the founding generation had "republican," communitarian leanings. Our forefathers were not devout disciples of Adam Smith, let alone Herbert Spencer (who in the mid-nineteenth century infamously coined the phrase, "survival of the fittest"). They were pragmatists, capitalists and socialists, willing to try whatever was necessary to insure that the American experiment did not fail...'

http://jurist.law.pitt.edu/forumy/2009/10/...ist-founding-fathers.php

Optionen

Abstract

Traditional decision theory distinguishes between risk and uncertainty. With risk, the probabilities of possible outcomes are known; with uncertainty, those outcomes are known, but not their probabilities. We introduce the concept of ignorance, a third, less tractable category. With ignorance, even the possible outcomes cannot be identified. Ignorance takes importance when high payoffs are associated with the unidentified outcomes. Thus we focus on consequential amazing developments, or CADs.

CADs spring upon societies as well as individuals. In the policy realm, the 2008 financial meltdown and the Arab Spring would represent CADs, major unanticipated events. For an individual, a CAD might be the discovery that a faithful spouse of many years has a secret second family, or that our trusted business partner has been pilfering corporate secrets all along. Authors depict the implications of consequential ignorance in some of the greatest of literary works: Hamlet’s ignorance of his father’s killer, Macbeth’s unawareness of outcomes when he attempts to seize the Scottish crown, Odysseus’s journey back to Ithaca involving a series of consequential adventures, all unknowable.

Consequential ignorance cannot be studied in a controlled laboratory setting, since its payoffs are high, its time delays often long, and merely introducing the subject tends to give away the game. Thus we study ignorance through great works of literature, from antiquity to the present day, positing that great writers understand how humans make decisions. We distinguish between unrecognized and recognized ignorance. In the latter category, we identify specific cognitive biases at work. We provide a formula for calculating consequential ignorance that incorporates the expected magnitudes and assessed base rates for CADs. Finally, we propose steps towards measured decision making under ignorance.

https://research.hks.harvard.edu/publications/...Id=9136&type=WPN

Traditional decision theory distinguishes between risk and uncertainty. With risk, the probabilities of possible outcomes are known; with uncertainty, those outcomes are known, but not their probabilities. We introduce the concept of ignorance, a third, less tractable category. With ignorance, even the possible outcomes cannot be identified. Ignorance takes importance when high payoffs are associated with the unidentified outcomes. Thus we focus on consequential amazing developments, or CADs.

CADs spring upon societies as well as individuals. In the policy realm, the 2008 financial meltdown and the Arab Spring would represent CADs, major unanticipated events. For an individual, a CAD might be the discovery that a faithful spouse of many years has a secret second family, or that our trusted business partner has been pilfering corporate secrets all along. Authors depict the implications of consequential ignorance in some of the greatest of literary works: Hamlet’s ignorance of his father’s killer, Macbeth’s unawareness of outcomes when he attempts to seize the Scottish crown, Odysseus’s journey back to Ithaca involving a series of consequential adventures, all unknowable.

Consequential ignorance cannot be studied in a controlled laboratory setting, since its payoffs are high, its time delays often long, and merely introducing the subject tends to give away the game. Thus we study ignorance through great works of literature, from antiquity to the present day, positing that great writers understand how humans make decisions. We distinguish between unrecognized and recognized ignorance. In the latter category, we identify specific cognitive biases at work. We provide a formula for calculating consequential ignorance that incorporates the expected magnitudes and assessed base rates for CADs. Finally, we propose steps towards measured decision making under ignorance.

https://research.hks.harvard.edu/publications/...Id=9136&type=WPN

Optionen

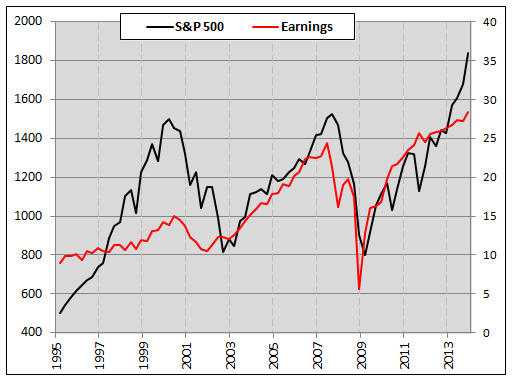

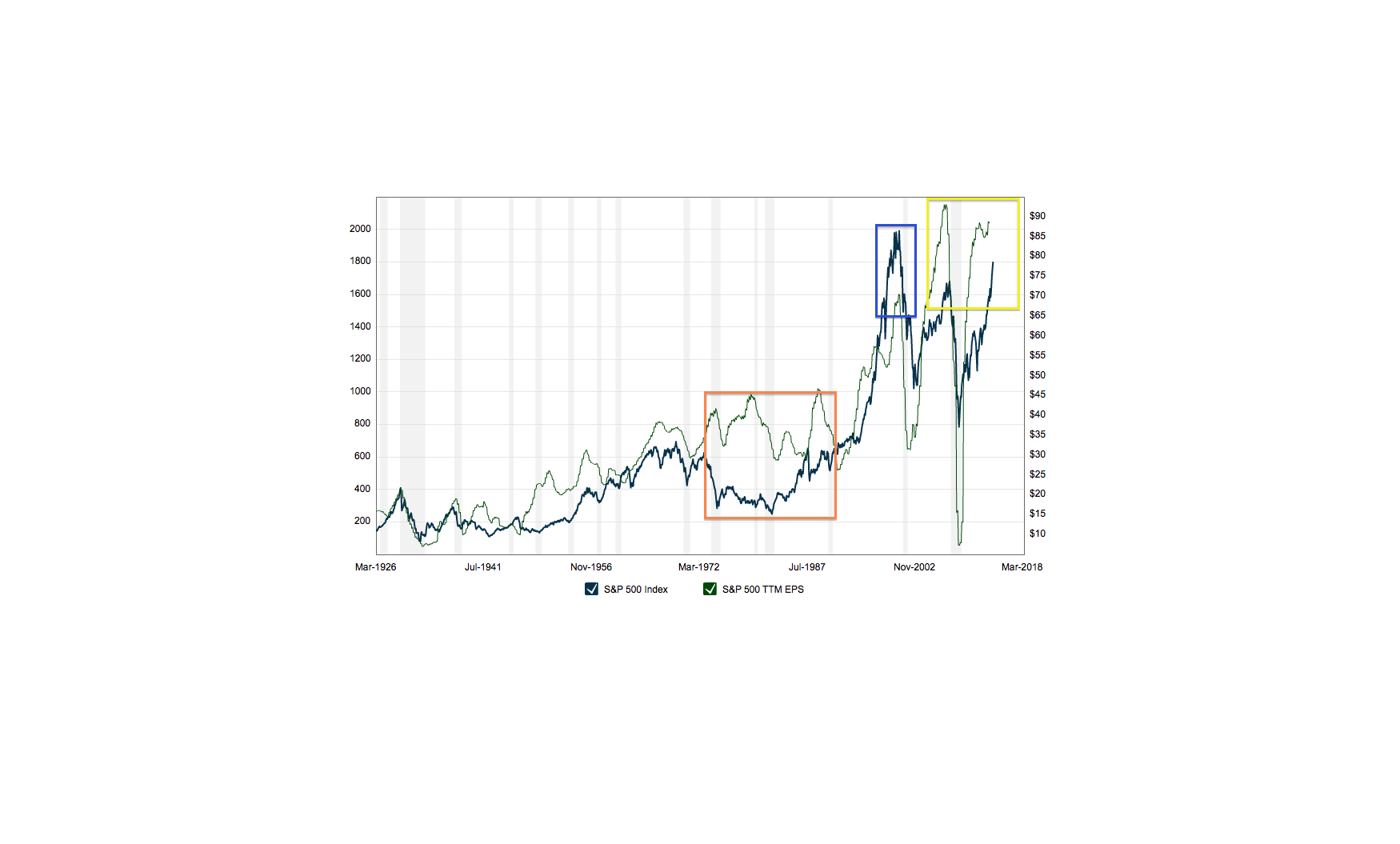

eines Bärenmarktes ist bekanntlich die Entfernung der Kurse von ihrer Grundlage, den Earnings. Massgeblich für die Definition eines kritischen Niveaus sind jedoch nicht die reported Earnings, sondern die Gewinnerwartungen vs Sentiment. Der Hinweis, der Abstand Preisniveau zum P/E von gestern sei historisch schon mal deutlicher ausgefallen als aktuell, kann deshalb keine Entwarnung begründen

Optionen

Angehängte Grafik:

spx-vs-corporate-earnings-historical-performance-....png (verkleinert auf 99%)

spx-vs-corporate-earnings-historical-performance-....png (verkleinert auf 99%)

damit EMs übergeordnet performen braucht es (in aktueller Umgebung) in den DMs entweder einen moderaten Bärenmarkt / Recession mit wieder sinkender Zinserwartung, einen Outflow bei den Aktien und typischerweise damit einhergehend eine Trendwende bei den Industrie-Commodities. Oder aber makro eine echte Boomphase, die eben jene Commodities nach oben zwingt und dann damit den Flow wieder in die EMs lenkt. Mit anderen Worten: Ich glaube JETZT weder an eine dramatische Performance der EMs trotz Sentiment noch des Dax...

Optionen

Der steile Anstieg 2012-2013 geht mit dem steilen Anstieg der Indizes einher.

Angehängte Grafik:

nyse-margin-debt-spx-growth-since-1995.gif (verkleinert auf 56%)

nyse-margin-debt-spx-growth-since-1995.gif (verkleinert auf 56%)

wie mehrfach von Fill dargestellt. Schön zu sehen auch die 2000er Blase, wo die Kurse den Earnings wegliefen. Für mich auch erkennbar, dass der Markt in den 70ern gegenüber heute unterbewertet war und auch deshalb eine Wiederholung dieses Ausmaßes unwahrscheinlich ist.

Das werden wohl feuchte Bullenträume bleiben! Armer lehna!

Das werden wohl feuchte Bullenträume bleiben! Armer lehna!

Angehängte Grafik:

earnings.png (verkleinert auf 29%)

earnings.png (verkleinert auf 29%)

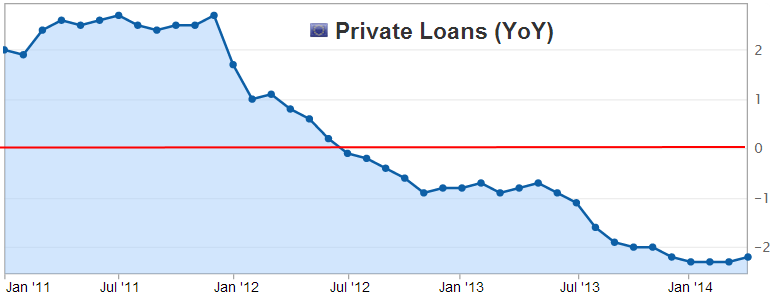

Hier werden sie jedenfalls nicht generiert - Bank balance sheets declined by around 20 percentage points of gross domestic product last year. Private Loans Eurozone:

Optionen

Angehängte Grafik:

private_loans.png (verkleinert auf 65%)

private_loans.png (verkleinert auf 65%)

In der modernen Geldtheorie entsteht neues Geld und damit eine Expansion des Money Supply nahezu ausschliesslich dadurch, indem Geschäftsbanken oder ihre Funktionen (Schattenbanken) Kredit vergeben. Angewandt auf die Börse bedeutet dies, dass frisches Geld an die Börse nur durch die Margin Debt gelangt, während alles andere einfach nur den Swap innerhalb verschiedener Anlageformen beschreibt. Wie im Credit Cycle makro fundiert eine Kreditexpansion an der Börse die Hausse und umgekehrt deren Rückabwicklung die Baisse. ..

Daraus folgt, dass die Bewegung der Margin Debt keinen Indikator für ein kritisches Niveau up- oder downside stellen kann. Jedenfalls nicht viel mehr als ein Kursindex selbst, denn steigende Kurse fallen notwendig mit einer Kreditexpansion zusammen (und umgekehrt). Es gilt nur grundsätzlich: Je höher die Kurse laufen, um so grösser das Rückschlagspotential - eben weil dann ein entsprechend grosses Kreditvolumen rückabgewickelt wird...

Daraus folgt, dass die Bewegung der Margin Debt keinen Indikator für ein kritisches Niveau up- oder downside stellen kann. Jedenfalls nicht viel mehr als ein Kursindex selbst, denn steigende Kurse fallen notwendig mit einer Kreditexpansion zusammen (und umgekehrt). Es gilt nur grundsätzlich: Je höher die Kurse laufen, um so grösser das Rückschlagspotential - eben weil dann ein entsprechend grosses Kreditvolumen rückabgewickelt wird...

Optionen

ist mittlerweile natürlich wieder reichlich unter Wasser... ist immer ärgerlich, wenn man einige Tage zuvor den braten gerochen und trotzdem nicht entsprechend gehandelt hat... eine Prämisse des trades war aber, dass ich im kurzen nicht so gut funktioniere und daher auch nicht kurzfristig reagieren sollte... trotzdem...

da hätte sich der ek aber schön senken lassen... abprall von der ema 200 und mit schwung, das geht ja nun mal gern noch ein paar tage oder wochen so weiter, wenn die das machen...

ariva-sentiment ist mittlerweile wieder strong long, nachdem es letzte woche deutlich short unterwegs war... immerhin...

da hätte sich der ek aber schön senken lassen... abprall von der ema 200 und mit schwung, das geht ja nun mal gern noch ein paar tage oder wochen so weiter, wenn die das machen...

ariva-sentiment ist mittlerweile wieder strong long, nachdem es letzte woche deutlich short unterwegs war... immerhin...

Optionen

aus Deiner Strategie kann durchaus etwas werden. Nur bezahlst du halt mit einem Risiko, dass ich so nicht eingehen würde, obwohl ich das Szenario weiterhin grundsätzlich teile. Eine entscheidende Bedingung für nachhaltigen Erfolg ist, sich über sein Risiko aufrichtig Rechenschaft abzulegen - und zwar vor dem Entry. Wenn man spürt, dass dies nicht wirklich möglich ist, ist das Risiko zu hoch...

Optionen

aber mir fällt es schwer, die eintrittswahrscheinlichkeit meiner annahmen abzuschätzen, und daher kann ich auch das risiko nicht gut kalkulieren... insgesamt bin ich guter dinge, aber die letzten 5-7 handelstage ärgern mich, da man das haussieren der kurse absehen konnte...

einen wunderschönen sommertag wünsch ich... bin am vertikutieren, meine nachbarn mögen es mir verzeihen.

einen wunderschönen sommertag wünsch ich... bin am vertikutieren, meine nachbarn mögen es mir verzeihen.

Optionen

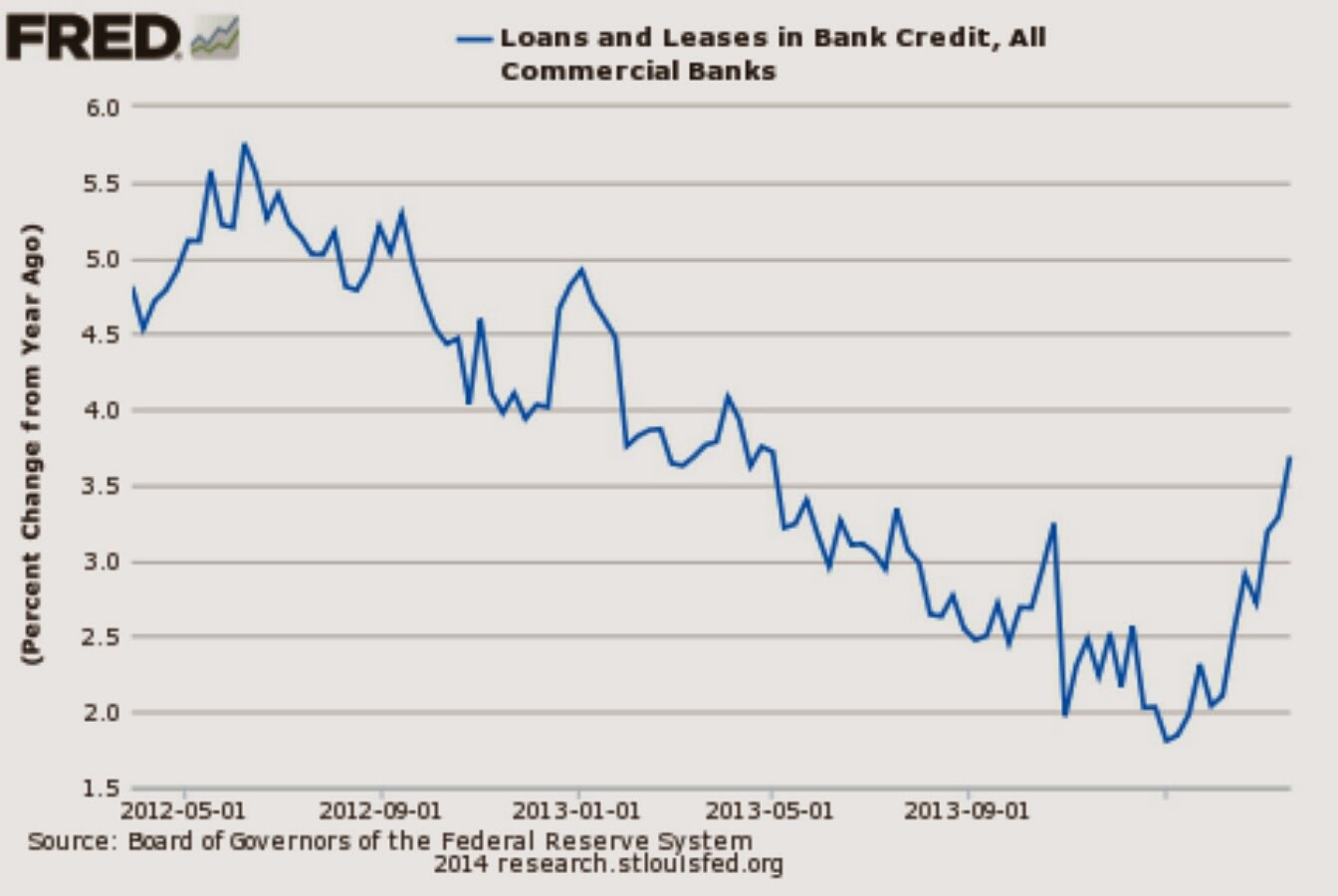

Das konsequente Tapering wird gemeinsam mit der fiskalen Konsolidierung vom Makro-Sentiment übersetzt als gelungene Recovery. Entsprechend zieht Private Investment wieder Kredit und kann so die Kontraktion des Saatssektors (bislang) kompensieren:

Optionen

Angehängte Grafik:

loans_and_leases.jpg (verkleinert auf 37%)

loans_and_leases.jpg (verkleinert auf 37%)

The list is a long one and includes practically every major theory:

(1) classical loanable funds theory, with time preference explaining the interest rate;

(2) Wicksell’s natural rate of interest;

(3) neutral rates of interest;

(4) rational expectations;

(5) the belief that real world market economies can be modelled with single representative agent models where agents maximise utility;

(6) Ricardian equivalence;

(7) belief in a real world tendency to general equilibrium;

(8) belief that money is neutral (whether in the short or long run, or in the long run);

(9) the quantity theory of money;

(10) the law of demand as a universal law;

(11) the law of diminishing marginal utility as a universal law;

(12) the law of diminishing marginal productivity;

(13) the belief that firms equate price with marginal cost or move price towards marginal cost;

(14) the belief that agents maximise utility in the neoclassical sense;

(15) the belief that involuntary unemployment is fundamentally caused by inflexible wages.

(16) the idea that macroeconomics needs rigorous microfoundations.

(via Lord Keynes)

(1) classical loanable funds theory, with time preference explaining the interest rate;

(2) Wicksell’s natural rate of interest;

(3) neutral rates of interest;

(4) rational expectations;

(5) the belief that real world market economies can be modelled with single representative agent models where agents maximise utility;

(6) Ricardian equivalence;

(7) belief in a real world tendency to general equilibrium;

(8) belief that money is neutral (whether in the short or long run, or in the long run);

(9) the quantity theory of money;

(10) the law of demand as a universal law;

(11) the law of diminishing marginal utility as a universal law;

(12) the law of diminishing marginal productivity;

(13) the belief that firms equate price with marginal cost or move price towards marginal cost;

(14) the belief that agents maximise utility in the neoclassical sense;

(15) the belief that involuntary unemployment is fundamentally caused by inflexible wages.

(16) the idea that macroeconomics needs rigorous microfoundations.

(via Lord Keynes)

Optionen

"Der finale Spike bzw der grosse Sentimenttrigger ist nur eine Frage der Zeit. Das Makrosentiment verbessert sich as predicted stetig - entsprechend strömt Dumb in die Aktien, wie die Flows nachweisen. Die langen Zinsen steigen mit den Konjunkturerwartungen, die das QE-Narrativ von den via Fed hochgepumpten Märkten sukzessive ersetzen. Gleichzeitig mehren sich die Indizien auf sinkende Earnings, was jedoch wie immer im Vorfeld des Bärenmarktes als Einmaleffekt oder saisonale Schwäche oder dergleichen weggewunken wird. Usw..."

fillorkill am 02.08.13

wie war das noch mit dem beige book und dem terminus weather? als saisonale schwäche weggewunken...

fillorkill am 02.08.13

wie war das noch mit dem beige book und dem terminus weather? als saisonale schwäche weggewunken...

Optionen

Möglicherweise ist es kritisch gemeint. Allerdings hat meine Analyse durchaus Bestand, wie ich finde. Konjunkturerwartung & Makrosentiment zogen ja tatsächlich an, während Earnings tendenziell schwächer tendierten. Dumb kauft zu, während smart tendenzielll abgibt. Und das QE-Moneyprinting ist inzwischen in der Mottenkiste. Die andere Sache ist das Timing. Da bin ich im Prinzip flat seit bald einem Jahr, also ein gutes Endstück des Bullmarktes verpasst. ...

Optionen

die prognose, dass tendenziell sinkende earnings zunächst als saisonal und vorübergehend eingeordnet werden, deckte sich recht gut mit der besonderheit im beige book, dass der harte winter als ein wichtiger grund für relative schwäche genannt wurde... es gab doch diese darstellungen, dass das wort wetter etwa um den faktor 10 mal häufiger im bericht vorkam...

mein bärenherz sagt also: gute prognose, wie immer, fill.

gruß

mein bärenherz sagt also: gute prognose, wie immer, fill.

gruß

Optionen

What are the grand dynamics that drive the accumulation and distribution of capital? Questions about the long-term evolution of inequality, the concentration of wealth, and the prospects for economic growth lie at the heart of political economy. But satisfactory answers have been hard to find for lack of adequate data and clear guiding theories. In CAPITAL IN THE TWENTY-FIRST CENTURY, economist Thomas Piketty analyzes a unique collection of data from twenty countries, ranging as far back as the eighteenth century, to uncover key economic and social patterns. His findings will transform debate and set the agenda for the next generation of thought about wealth and inequality.