MannKind - 500$ - Aktie zu 2,89$

Seite 7 von 10 Neuester Beitrag: 08.05.11 19:29 | ||||

| Eröffnet am: | 22.06.08 16:24 | von: Prometheos | Anzahl Beiträge: | 232 |

| Neuester Beitrag: | 08.05.11 19:29 | von: silbereuro | Leser gesamt: | 52.560 |

| Forum: | Börse | Leser heute: | 12 | |

| Bewertet mit: | ||||

| Seite: < 1 | 1 | 2 | 3 | 4 | 5 | 6 | | 8 | 9 | ... > | ||||

Die Aktie fällt heute um 12%.

Ein gefeuerter Mitarbeiter behauptet Studiendaten seien gefälscht. Selbst wenn an den Vorwürfen nichts dran ist, wovon ich ausgehe, ist es möglich dass dadurch das PDUFA Datum bzw. die Zulassung verzögert wird.

www.bloomberg.com/news/2010-11-04/...s-study-misconduct-update2-.html

Mannkind Chief Financial Officer Matthew Pfeffer, reached by phone, says Arditi's lawsuit is without merit because the company's investigation of the allegations conducted by an outside auditing firm found nothing wrong with the Afrezza clinical data.

The FDA has not raised any questions about the clinical data and Arditi was fired for "good cause," Pfeffer added.

Mannkind has not submitted a copy of its internal investigation to the FDA because the company's auditors found "nothing substantive to report to FDA. Had we found something, we would have reported it to FDA," said Pfeffer.

MannKind, in its most recent quarterly filing with the SEC, discloses that before Arditi filed his lawsuit on Sept. 16, the company "completed an internal investigation of his claims and retained an independent outside firm to conduct an independent investigation of his claims. Neither investigation found any basis for his claims."

MNKD, MannKind Corporation (11.16.2010 share price at $6.06)

MannKind Corporation, Stock Ticker “MNKD”

MNKD was founded by Al Mann, an entrepreneur and investor with a proven track record of successfully developing medical products and bringing returns to shareholders. So far, he has invested over a billion dollars of his own money into MNKD in addition to loaning the company money. As a result, he owns close to 40% of the shares of the company. Such a relatively high rate of inside ownership demonstrates that the incentives of Al Mann and MNKD shareholders are aligned.

MNKD is primarily invested in the research and development of Afrezza (an inhalable insulin), its Dreamboat reusable inhalers and its Screamin’ Cricket disposable inhalers. It is also researching therapeutic cancer vaccines.

http://www.mannkindcorp.com/

Alfred Mann, An Entrepreneur With a Track Record of Success

Al Mann’s track record of successfully developing and bringing products to market and generating substantial returns for shareholders is well-documented.

Al Mann started Spectrolab and Heliotek in 1956 and successfully sold both aerospace firms to Textron in 1960. He is renown as a biomedical inventor and investor and developed insulin pumps through MiniMed which was eventually sold to Medtronic in 2001 for $3.7 billion. Al Mann also successfully developed cochlear implants through Advanced Bionics.

http://www.forbes.com/lists/2010/10/...res-2010_Alfred-Mann_NG0I.html

The Product (“Afrezza”), An Inhalable Insulin

1. “Yes We Can!” Inhale, A Unique Delivery Method

MNKD is in the process of revolutionizing the diabetes space through the introduction of inhalable insulin. Many diabetics have to take four injections a day, one basal injection and three meal time injections. MNKD’s product currently deals with meal time insulin and will allow many diabetics to reduce the number of injections they have to take each day by 75%.

2. Afrezza, A Superior Form of Insulin

MNKD’s inhalable insulin (Afrezza) more closely mimics the natural insulin response of the human body than injectable insulins. The graph below compares Afrezza and several other types of insulin to a healthy body’s natural insulin response.

http://static.seekingalpha.com/uploads/2010/5/23/...tments_origin.JPG

{kind=link}

Many diabetics gain weight due to the fact that standard meal time injections are not rapid-acting and cause a spike in insulin levels two to three hours after the meal. This induces hunger which causes more calories to be ingested during the day. Since Afrezza mimics the body’s natural response, Afrezza users are significantly less likely to overeat due to abnormally high post-meal levels of insulin during non-meal times.

3. Reusable and Disposable Inhalers, More Convenient than Needles

MNKD’s oral reusable inhaler is embodied by its Dreamboat line.

http://www.mannkindcorp.com/dreamboat.aspx

MNKD also created a line of disposable inhalers for even more convenient use.

http://www.mannkindcorp.com/disposable_inhaler.aspx

Whether the delivery of insulin is conducted through the reusable or the disposable inhaler, either case presents a much more convenient and rapid acting method of insulin intake than the standard needle therapy that is the only option on the market currently.

Product Safety & Efficacy

So far, the safety and efficacy of MNKD’s inhalable insulin and inhaler have been rigorously tested. No significant adverse side effects were recorded and it’s effectiveness is at least as good as, if not significantly better than, many of the current diabetes treatments on the market.

More information about the science behind MNKD’s product and summations of recent clinical trial data can be found in the links below.

http://afresa.blogspot.com/

http://finance.yahoo.com/news/...Show-bw-1479611787.html?x=0&.v=1

Near-Term Catalysts

1. December 29, 2010 Meeting with the FDA

http://seekingalpha.com/article/...ish-options-sentiment?source=yahoo

There are two upcoming events that will have a significant effect on the price of MNKD shares. The first is the possibility of FDA approval in December of 2010 or soon thereafter. Accordingly to the original timeline, FDA approval should have occurred earlier this year. An overall view of the general FDA drug approval process is located in the link below.

http://www.fda.gov/drugs/resourcesforyou/consumers/ucm143534.htm

However, a Complete Response Letter (“CRL”) was issued which sent MNKD shares which were over $10 a share into a nose dive. Since the CRL, MNKD shares have basically been range bound between $5.00 - $7.25 a share. The CRL did not reject MNKD’s patent applications and merely asked for new data. The data was provided to the FDA earlier this year after the issuance of the CRL and a meeting is set in December of 2010 between the FDA and MNKD. At this point, aside from the fact that the FDA is backlogged with thousands of new drug approval petitions, there appears to be no good reason for MNKD’s product not to be given speedy approval. A New York Times article concerning the backlog of applications at the FDA is below.

http://www.nytimes.com/2010/02/20/business/20generics.html

2. Partnership Talks with Global Pharmaceutical Companies

The second near-term catalyst concerns the possibility of a partnership announcement with a global pharmaceutical company. MNKD was in talks with over ten potential partners but has narrowed the list to three. The three potential partners are assisting MNKD currently with the FDA approval process. If they did not think that there was a significant chance that the product would be approved, it stands to reason that they would not be assisting MNKD in its dealings with the FDA. A global partner would help MNKD market and distribute the product which will allow MNKD to continue to focus on researching and manufacturing the product.

The Perfect Storm For Explosive Near-Term Share Price Appreciation

1. Too Many Shares Short

As of October 29, 2010, the number of shares short is 16.09 million and short percentage of float is 25% with an astounding short ratio of 8.10.

http://finance.yahoo.com/q/ks?s=MNKD+Key+Statistics

FDA approval in December means that a partnership announcement would be imminent. By themselves, the two events will propel MNKD past $20 a share. When also taking into consideration the number of shares short, covering by short sellers could propel the stock past $30 a share before the close of 2011.

Long-Term Catalysts

1. Greater Market Awareness & Acceptance of Inhalable Insulin as a Viable Treatment Option

It should be self-evident that diabetics would prefer inhaling rapid-acting insulin at meal time rather than injecting themselves with needles. In addition to the fact that studies clearly show that there is less pain involved with inhaling the meal time insulin versus injecting it, there is also much less social stigma involved in inhaling insulin than in injecting oneself in public with needles. The convenience of an inhalable form of insulin is indisputable. As MNKD’s product gains wider publicity, many diabetics will try and eventually switch from their standard meal time insulin injections to MNKD’s rapid-acting and more convenient inhalable insulin.

2. FDA Approval Means Monopoly Position in the Inhalable Insulin Space

Since MNKD is the only company that is currently close to introducing an inhalable insulin product into the market, FDA approval virtually guarantees an almost unassailable monopoly position in the inhalable insulin space for many years.

Several years ago, Pfizer launched a competing inhalable insulin product called Exubera. The subsequent failure of Exubera to command significant market share as well as its inability to maintain consistent clinical viability dissuaded many potential competitors from developing their own inhalable insulin lines. As a result, MNKD remains the sole company that is close to approaching FDA approval and eventual market distribution of inhalable insulin.

For an exhaustive comparison between Afrezza and Exubera, please refer to the link below.

http://afresa.blogspot.com/2010/05/...-comparison-of-exubera-and.html

The failure of Exubera is good for MNKD for the following reasons. First, it means that Pfizer, a global pharmaceutical company, is no longer a competitor to MNKD. Second, it also strongly suggests that Afrezza will eventually be approved by the FDA since Afrezza is a superior product to Exubera as the above comparison indicates.

With eventual FDA approval on the near-term horizon, this will leave MNKD as the ‘last man standing’ and subject to much less competitive price pressures than would normally be the case.

3. Increasing Rates of Diabetes Worldwide

Moreover, the long-term trend for the numbers of diabetics is projected to increase dramatically by 2030. More sedentary lifestyles and the increased caloric consumption that occurs as incomes rise are the primary contributing factors to the worldwide diabetes epidemic. The following links present some evidence of the global diabetes epidemic.

http://www.who.int/diabetes/facts/world_figures/en/

http://care.diabetesjournals.org/content/27/5/1047.full

http://www.nytimes.com/2010/09/28/business/global/...02030&st=cse

Recent Market Panic Over Specious Lawsuit Over-Discounts Share Price

1. Market Dislikes Uncertainty

Generally, the market tends to over-discount the value of companies faced with lawsuits. Lawsuits entail an element of uncertainty and the market does not react very well to uncertain prospects.

2. Wrongful Termination Suit Against MNKD Baseless, Presents Buying Opportunity

In the case of MNKD, the recent unlawful termination lawsuit by a former disgruntled employee alleging fraud by the company in its clinical trials appears fraudulent, specious, and without any legal or evidentiary foundation.

An independent investigator was provided unfettered access to the data related to MNKD’s FDA submission for Afrezza. “The independent investigator concluded that MannKind is, and was, taking prudent measures under Good Clinical Practice regulations to meet the requirements of Good Clinical Practices, and that there was no evidence of any deception or intent on the part of MannKind to deceive the FDA.”

http://finance.yahoo.com/news/...sues-bw-2001617502.html?x=0&.v=1

Currently, MNKD is trading at a share price of $6.06 a share, well below the +$20 a share price it recorded several years ago. The recent bout of negative news coverage concerning the recent wrongful termination suit is an excellent time to buy shares at overly discounted prices.

Risks of Investing in MNKD

1. Possible Delay in FDA Approval

Due to the backlog of new drug applications confronting the FDA and the recent wrongful termination lawsuit brought against MNKD, there is a chance that the FDA will delay the approval of Afrezza pending further studies or investigation.

As mentioned above, the FDA will probably conclude that the allegations in the wrongful termination suit against MNKD are groundless. The risk is that with the FDA overstretched, even a baseless lawsuit may consume valuable resources and delay the process of approval.

If the FDA decides that Afrezza must be subject to further trials, this will also serve to lengthen the approval process.

Regardless of the reason, a delay in the FDA approval process could send MNKD shares down to the $3.50 to $4.00 range or lower. When the CRL was issued earlier in 2010, MNKD shares fell from +$10.00 to as low as $4.76. A similar drop from current prices would have MNKD shares at sub-$3.00 a share.

2. Possible Denial of Afrezza

So far, all of the clinical trials suggest that Afrezza is a safe and very effective product. This strongly indicates that Afrezza will eventually be approved.

In the case that there is an outright denial by the FDA, MNKD’s value would be substantially impaired and share prices could plummet to sub-$2.00 a share since the value of the company would, at that point, solely depend on its therapeutic cancer vaccine line and whatever residual value there may be in the research of Afrezza.

It must be reiterated that at this point, all the evidence suggests Afrezza will be approved by the FDA.

Reasons to Buy MNKD

1. Clinical Studies Strongly Indicate that Afrezza Approval Imminent

The two main areas that the FDA focuses on when considering a new drug application is (1) whether the product is safe and (2) whether the product provides significant benefits over existing options. Clinical studies demonstrate that Afrezza is just as safe as current treatment options for diabetics and that it is a superior form of insulin therapy relative to current insulin options.

2. Partnerships with Global Pharma

MNKD is currently engaged in negotiations with three global pharma companies and the three candidates are assisting MNKD with the FDA approval process. This suggests that FDA approval will quickly be followed by a partnership agreement that will give the company greater access to capital and expertise in the marketing and distribution of Afrezza.

3. Al Mann’s Incentives are Aligned with Shareholders

Al Mann owns approximately 40% of the shares of MNKD and continues to lend the the company money as needed. He has a very strong incentive for MNKD to succeed. When MNKD’s other shareholders succeed, Al Mann, as MNKD’s largest single shareholder, will also succeed.

4. Al Mann’s Track Record of Success

Al Mann has a history of making money for shareholders and successfully introducing and developing new products into the healthcare space.

5. MNKD’s Access to Capital

Most ventures fail for lack of capital. MNKD has plenty of available capital to finance its research and development. Al Mann stands ready to finance MNKD’s ventures on an as-needed basis. Fortunately, FDA approval may come as early as December 29 of 2010 and subsequent partnerships will give MNKD access to even greater amounts of capital.

6. MNKD More than Just About Diabetes Treatment

Although most of the focus on MNKD is on its diabetes products which include Afrezza and its reusable and disposable oral inhalers, it is also involved in the research and development of therapeutic cancer vaccines.

Suggested Ways to Invest in MNKD

1. Build Your Share Position Incrementally

In the past five years, the price range for MNKD shares were as high as +$20 a share to as low as sub-$2 a share. As with many other start-up companies in the pharmaceutical space, share price volatility is a given. As a result, buying shares in increments is recommended.

2. Attractive Entry Points

If the FDA delays approval of Afrezza, a drastic drop in MNKD shares would probably result and present the investor with an opportunity to buy shares at prices significantly cheaper than $6.06 a share. Shares may fall below $3.00 a share in such a case.

If the FDA approves Afrezza, MNKD’s share price should go above $12.00 a share within a couple of months after the announcement, if not within a couple of weeks or even days. Moreover, this will make it much more likely that a partnership announcement would be imminent which should push the share price past $20.00 a share. The period between the FDA approval and the partnership announcement may present some opportunities to add to your position or it may be a good entry point for those that do not want to risk FDA delays or disapproval of Afrezza and the subsequent effects of such announcements on MNKD’s share price.

The next attractive entry point would be some time after the partnership announcement but before any large scale manufacturing, advertising, and sales of Afrezza. The market may not properly factor in future sales of Afrezza until the first set of quarterly numbers come out after large scale efforts to promote and distribute the product.

Although a lot of money can be made trading in and out of MNKD, the best strategy may simply be to build a larger and larger position of MNKD shares over time. As previously mentioned, due to the extreme price swings characteristic of MNKD shares, it is recommended to buy and eventually sell MNKD shares incrementally.

Other Suggested Reading

http://afresa.blogspot.com/

http://seekingalpha.com/article/...alue-of-mannkind?source=qp_article

http://seekingalpha.com/article/206605-a-giant-leap-for-mannkind

Posted 1 day ago

Trading Technique, Diversification Across Positions and Time

Times of volatility call for different trading techniques. In today’s current volatile environment, it may be advantageous to employ diversification across different stocks and also across time.

Diversification Across Positions

Adequate diversification can be obtained through 7 to 8 stock positions. There is really no need to buy into hundreds of different companies to be adequately diversified or to buy into a mutual fund. Generally, mutual funds are disadvantageous because their returns lag index funds and mutual funds charge higher annual fees in addition to any start up or exit fees that are involved. Moreover, mutual funds are normally subject to more regulation which limits their ability to buy into the best investment opportunities. What many people also do not realize is that the culture of many mutual funds encourages herd-like behavior since their aim is to mirror the performance of the overall market. Since that is the goal, most people would be better off buying index funds which very closely mirror actual market performance and charge substantially less in terms of management fees.

Diversification Across Time

In addition to diversifying across different stock positions, it is also advantageous to diversify across time. This means to buy into a stock at different times instead of placing an order to buy all at once. Also, when selling a stock, the same approach may be helpful. For example, if a stock breaks out of its recent trading range and begins trading well above what fundamental analysis dictates would be a reasonable price range for the stock, it is often a good idea to sell off a quarter of your position at one price level and a quarter at another price level and so on. By doing this, you can lock in gains in case the stock drops in price later. Maybe more importantly, it also allows you to keep money in play as a stock breaks up in price. It gives you a better chance at capturing gains when a stock’s price is fueled by market sentiment to ever more ridiculous price levels. Since it is generally difficult to time the lows and highs, diversification across time can be used as a risk management tool to provide better average entry points and exit points.

Posted 1 day ago

Volatility, Here for the Next Several Years

The current market canvas that investors are painting on is colored by one word, volatility. With QE2 and low interest rates, the general market trend in terms of price action should be bullish through the end of 2011 which means that stock markets in the U.S. and many other developed and developing countries should end 2011 higher than they are right now.

With massive asset purchases by the Fed and an effective ‘zero’ percent interest rate policy, commodity prices are rising and are set to rise to ever higher levels going forward. The multi-decade bull market in bonds is set to reverse and the dollar appears set to win against a basket of other currencies in a race to the bottom.

Welcome to volatility. It’s here to stay so get used to it. The only question for the next several years is whether price action across various asset classes will trend volatile up or volatile down. Stocks and commodities will trend volatile up while U.S. government bonds will trend volatile down.

(Bergen County), against us and two of our officers. Pursuant to an existing arbitration agreement, Mr. Arditi had previously agreed to resolve claims

relating to his employment through arbitration. On November 22, 2010, we confirmed that Mr. Arditi had filed a Notice of Voluntary Dismissal with the

court on November 18, 2010, dismissing his lawsuit without prejudice. We did not make any payment or provide consideration of any kind to Mr. Arditi in

connection with this dismissal. As of the date of this report, Mr. Arditi has not initiated arbitration.

Theoretisch möglich wäre auch eine vorzeitige Entscheidung vor dem 24.12, solche Fälle gab es schon, ist aber sehr unwahrscheinlich.

Die Akzeptanz ist weder bei den Patienten, noch Ärzten wirklich groß.

Eine Injektion stellt für fast alle Patienten kein Problem dar, wenn sie erst einmal damit angefangen haben. Und die Injektion bedarf es in den allermeißten Fällen ohnehin, da viele Patienten ein langwirksamen UND ein kurzwirksames Insulin benötigen. Beide Formen sind mit der Inhalation aber nicht darstellbar, da man mit der Inhalation kein Depot im Körper erzeugen kann. Weiterhin ist Insulin ein Wachstumshormon, was zu bedenken ist, wenn man die Risiken von unkontrolliertem Wachstum in Betracht zieht. Da es bei der Applikation über die Lunge auch noch deutlich höher dosiert werden muss, wird dieses Risiko sicher nicht vermindern.

Letztlich kommt dann noch der Preis hinzu.

Dieser wird, allein schon wegen des höheren Aufwandes und der vielfach höheren Dosierung, kaum auf dem Niveau einer heutigen Insulintherapie liegen können.

Letztlich stellt sich die Frage, ob sich der Vertrieb für die paar Einzelfälle, die dann damit behandelt werden, wirklich lohnt. Nicht umsonst haben die großen in der Insulinbranche wie NovoNordisk diesen Weg nicht weiter verfolgt, obwohl man die Zulassung sicher hätte bekommen können.

Für mich sind das einfach zu viele Punkte die gegen einen Erfolg sprechen.

Also Jungs, wenn ich Euch richtig verstanden habe, wollt Ihr damit ausdrücken, daß eine Entscheidung wahrscheinlich erst im Januar bekannt gegeben wird?

Falls sie positiv ausfällt, soll es mir nichts ausmachen!

Gruß@all

Wenn man sich schon zukunft weisenden Therapien zuwenden will, dann muss man ausserhalb des Bereiches Insulin suchen.

Viel Interessanter ist im Moment der Einsatz von GLP-1. Die Therapieerfolge sind gut und der Eisatz sehr einfach und sicher. Zusätzlich verlieren die Patienten enorm an Gewicht.

Ein weiterer Weg sind die DPP-4-Hemmer, die einen ähnlichen Weg beschreiten, durch Hemmung des Abbaus von Körpereigenem GLP-1. Hier besteht nur das Problem, dass man nicht so deutlich von einem Erfolg partizipieren kann, da es bereits eine Vielzahl von Substanzen gibt und eine noch größere Anzahl auf den Markt drängt, was dann wiederum bedeutet, dass es nicht DAS Unternehmen geben wird, welches überproportional profitiert.

Interessanter sind da schon Firmen, die einen neuen Weg eingeschlagen haben.

Idee der Therapie ist es, durch Senkung der Nierenschwelle den Zucker über den Urin auszuscheiden.

Dies hätte auch den zusätzlichen Effekt, dass die Patienten deutlich an Gewicht verlieren können, da die Kalorien mit dem Zucker im Urin ausgespült werden.

Hier gibt es aber noch keine Zulassung die Studien befinden sich maximal in PhaseIII

Conclusion:

The street has no idea of the profoundly positive impact Afrezza will have in the world of diabetes therapies. Once Afrezza is approved and once the absorption kinetics of it is understood by healthcare providers and patients, Afrezza will become the new “normal science” for treating diabetes. Afrezza will overtake basal insulin as the first course of insulin therapy for type 2 diabetics going onto insulin therapy (earlier in the treatment plan) and will replace existing RAA options for a majority of patients already on prandial insulin. When this happens, not only will Afrezza reach “mega-blockbuster” status but it could become the most valuable drug of our time. When the barriers to insulin therapy come down, the "Paradigm Shift" of Afrezza is inevitable -- improving the health and Quality of Life for millions of diabetics.

Disclosure: Long MNKD

Stocks: MNKD, SNY, NVO, LLY

Clearing Up the Uncertainty Around MannKind’s Afrezza

by: KLLJ Investments December 08, 2010 | about: MNKD Font Size: PrintEmail Recommend 2 Share this page

Share0 KLLJ Investments 271

Followers 10

Following FollowSend Message You are currently following KLLJ Investments

Stop FollowingYou are no longer following KLLJ Investments

Articles (11)

Instablog (17)

Comments (25)

Profile

Submit an

article to With the upcoming PDUFA date for MannKind’s (MNKD) Afrezza of December 29th, there are just a few weeks left for investors to take a position before this binary event. Investors rely too much on analyst comments and published headlines from journalists that perform cursory due diligence at best. Smart investors who look at the underlying technology, the barriers to entry for insulin therapy and the huge unmet need in the market for a better solution will understand why Afrezza is such an advancement above the gold standards that exist today. There is an enormous opportunity in the market to do a better job of controlling this pandemic that Afrezza addresses. It is estimated that 2 new diabetics are diagnosed every 10 seconds worldwide. If Afrezza can make the impact it should, it could become one of the biggest selling drugs of all time.

There are number of misconceptions that surround Afrezza and whether or not it will find success in the market. These uncertainties continue to pressure MannKind’s share price and I believe all of them are unwarranted. It is important to note that these misconceptions come from the financial community and NOT from the medical community, who has shown a strong willingness to prescribe Afrezza once approved.

Exubera failed and therefore Afrezza will fail:

This one is a tired story told by a bear analyst that is easily dispelled simply by looking at the facts. I’ll layout each of the facts below and if you still think that Exubera foreshadows the failure of Afrezza --then MannKind definitely isn’t the stock for you.

Exubera Facts:

Pfizer’s (PFE) Exubera was one of the biggest failures in the history of biotech. Originally projected to do over $2B a year in sales, it was a complete flop when introduced and Pfizer took a $2.8B charge to write-off the program. MannKind’s detractors and skeptics continue to point to the dismal sales of Exubera as an indicator for the future of Afrezza. Here are the facts about Exubera, which ultimately led to its failure.

Exubera offered absolutely no medical benefit whatsoever to Rapid Acting Analogs (RAA) None.

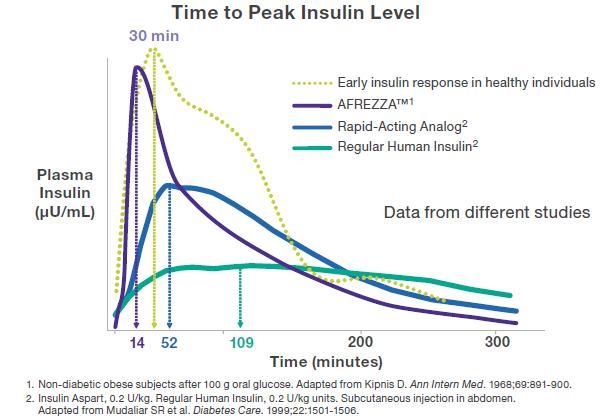

Exubera achieved peak insulin levels at 49min compared to injected Rapid-Acting Insulin's 52min (Afrezza peaks at 14min)

The only benefit of Exubera is that you inhaled it and could prevent mealtime injections, but the kinetics and side effects were similar to regular RAA.

Exubera had very complex dosing requirements, unique to the product and not linear to standard insulin units. You still had to perform dose titration before a meal and continue to perform Self-Monitoring Glucose Tests.

Prescribers hated it. It offered no advantage as a therapy, had complex dosing and therefore took a lot of time to explain its use to patients. Patients were often confused by how to use it, which took up a lot of time for physicians and their staff.

Exubera was priced 20% higher than RAA so Payers didn’t want to cover it.

The device itself was very inconvenient.

Despite a popular myth, Exubura did not cause an increase in lung cancer risk.

It is no wonder that Exubera was such a dud in the market given the facts above. The question is why did Pfizer even bother with it? The ‘other’ company’s efforts at inhaled insulin were ceased after Exubera’s failure. Every single one of those programs was a ‘me too’ effort offering no medical benefit, just like Exubera.

Now here are the facts about MannKind’s Afrezza:

Afrezza Facts:

Afrezza is the world’s first Ultra-Rapid Insulin.

Afrezza mimics the normal insulin response to a meal that a healthy person would have.

Afrezza greatly reduces the risk of hypoglycemia

Afrezza is weight-neutral.

Afrezza results in lower fasting glucose levels.

Afrezza inhaler is convenient and easy to use, tested for patients as young as 4 years old.

Afrezza causes no clinically meaningful impact to pulmonary function (1.7% on the Medtone device – similar to Exubera - and about .5% on the Gen2 inhaler.) This is about the same impact you would see by aging 1 year and it reverses when treatment is discontinued.

The Device is disposed of every 2 weeks, eliminating concerns over cleaning or long-term durability.

Afrezza’s meal-escalation study demonstrated that there was no increased risk of hypoglycemia from Zero up to 150 grams of carbohydrates during a meal. Very little if any need for complex meal titration.

Afrezza eliminates the need for painful shots, a major concern for new patients requiring insulin therapy and a complaint for those already on insulin therapy.

Afrezza breaks down all of the existing barriers for introducing insulin therapy to a patient!

No Advisory Committee: Analysts have backed off this one a bit, but some still say the lack of an Advisory Committee means that the FDA won’t approve Afrezza by this PDUFA date. It isn’t surprising at all that an Advisory Committee wasn’t required for Afrezza. There is already precedent for pulmonary delivery of insulin with the approval of Exubera – who had their own advisory committee in 2005 where the expert panel members voted 7-2 in favor of approval. That Advisory Committee was to discuss the efficacy of Exubera and the pulmonary delivery of insulin. Afrezza is a far better product than Exubera for all of the facts described earlier and the FDA knows this. Advisory committees are usually called when there is a Risk vs. Benefit discussion that needs to take place with feedback from outside experts or if the drug under review is a new, novel compound. Afrezza is simple insulin carried on completely inert particles. Afrezza had no serious safety flags through dozens of trials and 5,000 patients that would require a Risk vs. Benefit discussion. There is absolutely nothing with Afrezza that would warrant an Advisory Committee. If one was deemed necessary by the FDA, it would have been called during the initial review in 2009.

Patient Acceptance: Diabetics are ‘used’ to taking multiple shots a day and won’t want to change. Are you kidding me? This is one of the most asinine statements that I’ve heard on numerous occasions. Now, while this may be true for some, it will be the exception and not the rule. This was even demonstrated in the Quality of Life study referenced earlier, where when given the choice of continuing to use injected RAA insulin or switching to Afrezza, 75% chose to switch. Now think about the millions of diabetics who should be on insulin therapy but resist it. Taking shots is the most widely referenced barrier to entry for beginning insulin therapy. MannKind presented a poster presentation at the 2010 ADA conference to discuss a survey conducted directly to almost 1,100 Type 2 Diabetics regarding the interest of inhaled insulin given the medical benefits laid out in the survey – over 68% of responders said they would be interested in it, and that is before they see commercials on TV or hear about it from their physician. Most of the reasons for the interest expressed by patients were better control of high blood sugar after a meal, avoiding the discomfort and inconvenience of shots along with less weight gain.

FDA won’t allow MannKind to switch Delivery Devices: There is no FDA Draft Guidance for Bioavailability and Bioequivalence Studies for Pulmonary delivery. The closest thing is Draft Guidance for Nasal delivery (local action.) In the research I've done, the FDA is most concerned about particle size and drug exposure when it comes to new devices. A good comparison is nebulizer machines. Studies show there is a wide variation of drug exposure and particle size across nebulizers. There are acceptable ranges accepted by the FDA. For Bioavailability and Bioequivalence in different classes of drugs, there are generally recommendations given by the FDA. Many of those just require In Vitro studies. Comparative studies are also common. YOU DO NOT HAVE TO RUN ALL NEW TRIALS to show bioequivalance. In the case of Gen2, all that needs to be demonstrated is that the drug delivered to the deep lung is similar and the particle size is similar. The recommendation from the FDA is that you consult with them when designing bioequivalance studies. THAT IS EXACTLY WHAT MANNKIND DID. In fact, they ran the recommended assays to demonstrate bioequivalance that the FDA wanted along with another standard. MannKind’s Gen2 inhaler is simply a more efficient, simpler form of the Medtone inhaler.

Conclusion:

The street has no idea of the profoundly positive impact Afrezza will have in the world of diabetes therapies. Once Afrezza is approved and once the absorption kinetics of it is understood by healthcare providers and patients, Afrezza will become the new “normal science” for treating diabetes. Afrezza will overtake basal insulin as the first course of insulin therapy for type 2 diabetics going onto insulin therapy (earlier in the treatment plan) and will replace existing RAA options for a majority of patients already on prandial insulin. When this happens, not only will Afrezza reach “mega-blockbuster” status but it could become the most valuable drug of our time. The Paradigm Shift of Afrezza is inevitable -- improving the health and Quality of Life for millions of diabetics.

In a future article, I’ll cover how Afrezza breaks down the existing barriers to insulin therapy and how that equates to huge market share. In the meantime, you can read a post on my Instablog regarding the subject here.

Disclosure: I am Long MNKD.

Aber in der Praxis sieht es nach meinen eigenen Erfahrungen doch oft anders aus und die Hoffnungen auf einen Blockbuster scheitern an den Anforderungen die ein Medikament im Alltag erfüllen muss.

Nicht umsonst war die Einführung von Exubera im Jahr 2006 ein ebensolcher Flop.

Mir viel Energie und Aussendienstaktivität versuchte Pfizer dieses Produkt erfolgreich zu launchen. Und heute, 4 Jahre später???? Man hört wirklich nichts mehr davon, Exubera hat nie eine wirkliche Rolle in der Insulintherapie gespielt und dies lag mit Sicherheit nicht an der mangelnden Erfahrung der Verantwortlichen.

Das die Jungs bei Pfizer Produkte vertreiben können, haben sie in der Vergangenheit schon oft bewiesen.

Also stellt sich doch die Frage, woran der Misserfolg dieser Therapieform liegt?

Beachtenswert ist der letzte Abschnitt "Fazit". Zeigt er doch ganz klar welch grobe Fehleinschätzungen hier vorlagen.

Das neue Inhalative Insulin Exubera® ist seit Anfang 2006 in Deutschland zugelassen.

Die Entwicklung des neuen Inhalativen Insulins Exubera® wurde von der Fachwelt mit grosser Aufmerksamkeit verfolgt. Auch die Markteinführung von Exubera® wurde von Anfang an mit kontroversen Diskussionen begleitet. Wir haben diesen Entwicklungsprozess in einzelnen Stadien dokumentiert, die Sie auf unserer Webseite Exubera-in-Progress lesen können. Im folgenden wird eine Gesamtübersicht gegeben.

Eigenschaften

Exubera® ist ein schnell wirkendes Humaninsulin zur Behandlung des Typ-1- und Typ-2- Diabetes.

Das inhalative Insulin wird mit Hilfe eines Inhalators eingeatmet. Über die Lungenalveolen kommt es relativ schnell ins Blut.

Laut den FDA-Daten werden die höchste Konzentrationen vom inhalativen Insulin Exubera® nach 49 Minuten (30 bis 90 Minuten) erreicht, bei subkutaner Gabe.vom schnell wirkenden Humaninsulin nach 105 Minuten (60 bis 240 Minuten).

Das Inhalative Insulin ist dadurch schneller wirksam als subkutan injiziertes schnell wirkendes Humaninsulin. Aufgrund des raschen Wirkungseintrittes sollte Exubera® innerhalb von 10 Minuten vor Beginn einer Mahlzeit gegeben werden.

Pfizer hebt insbesondere hervor, dass viele Patienten Hemmungen davor haben, Insulin subkutan zu spritzen. Dadurch würde wertvolle Zeit bei der Diabetes-Therapie verloren gehen. Das inhalative Insulin Exubera könne dazu beitragen, die Hemmschwelle vor einer notwendigen Insulintherapie zu senken. (Medknowledge-Anmerkung: Es ist jedoch zu vermerken, dass bei Diabetes-Typ-II die Umstellung zur Insulintherapie in der Regel zuerst mit verzögert wirkenden Insulinen begonnen wird, die weiterhin subkutan gespritzt werden müssen)

Anwendung:

Das inhalative Insulin Exubera sollen die schnellwirksamen Subkutaninsuline vor den Mahlzeiten ersetzen. Verzögerungsinsuline müssen weiterhin gespritzt werden.

Wir haben Pfizer bzgl. der Handhabung der Exubera in der Praxis kontaktiert und folgende Antwort erhalten: "Exubera kann bei der Behandlung von Diabetes-Patienten die kurz wirkenden subkutanen. Insuline ersetzen. Bei erwachsenen Patienten mit Typ-1-Diabetes ist Exubera nach sorgfältiger Nutzen-Risiko-Abwägung zusätzlich zu lang wirkendem oder verzögert wirkendem subkutanem Insulin bestimmt.

Exubera ist für die Behandlung von erwachsenen Patienten mit Typ-2-Diabetes zugelassen, die mit oralen Antidiabetika nicht zufriedenstellend eingestellt sind und eine Insulintherapie benötigen. Zur Verbesserung der Blutzuckerkontrolle kann inhalatives Insulin allein oder in Kombination mit oralen Antidiabetika und/oder lang oder verzögert wirkenden, subkutan injizierbaren Insulin eingesetzt werden."

Wirksamkeit

Der Wirkungseintritt bei Exubera ist schneller als die subkutane Humaninsulin. Zwei aktuelle Studien (1) zeigten jedoch im Vergleich zum konventionellem Insulin kein erhöhtes Hypoglykämie-Risiko unter Exubera. (Medkowledge-Anmerkung: Es sind Vergleichsdaten. Hypoglykämien sind jedoch im allgemeinen die häufigste Nebenwirkung einer Insulintherapie, einschließlich des Exubera).

Die erwähnten Studien haben weiterhin ergeben, dass unter Exubera im Vergleich zum subkutanen Insulin zu einer geringeren Gewichtszunahme kommt (in 2 Jahren unter Exubera 1,7kg, unter dem konventionellen Insulin 2kg). Woher dieser Unterschied kommt, ist derzeit noch unklar.

Die HbA1c-Wert-Einstellung im Rahmen der intensivierten Insulintherapie wird durch das inhalative Insulin im Vergleich zu subkutanem Insulin nicht signifikant verbessert: Nach zwei Jahren lagen die HbA1c-Werte in beiden Therapie-Gruppen bei den Typ-2-Diabetikern in einem ähnlichem Bereich (7,3%). HbA1c-Senkung ist also unter Exubera ähnlich wie bei gespritztem Insulin.

Derzeit sehen die deutsche IQWiG (2) und die englische NICE (3) durch die Vorgestellten Daten keine signifikanten Vorteile des inhalativen Insulins Exubera® gegenüber subkutanem Insulin bei der Blutzuckereinstellung. IQWIG weist ausserdem darauf hin, dass es Hinweise für mögliche Nachteile wie beispielsweise häufigere Hypoglykämien (Unterzuckerungen) gibt.

Ob die deutsche IQWiG oder die englische NICE durch die vorgestellten Daten (1) auf der Jahrestagung der American Diabetes Association in Washington 2006 ihre bisherige negative Bewertungen bezüglich Exubera® ändern, ist abzuwarten

Dosis

Exubera® ist als 1-mg- und 3-mg-Einzeldosis-Blisterpackungen erhältlich. Diese werden zur oralen Inhalation über die Lunge angewendet und dürfen nur mit dem Insulin-Inhalationsgerät angewendet werden.

Die Anfangsdosis und weitere Gaben (Dosis und Zeitpunkte) sollten durch den Arzt individuell festgelegt und entsprechend dem Ansprechen und den Anforderungen des Patienten angepasst werden (z. B. Ernährung, körperliche Aktivität und Lebensweise).

Eine Tabelle im Beipackzettel macht ungefähre Angaben für die initiale, präprandiale Exubera-Dosierung (abhängig vom Körpergewicht des Patienten)

Für weitere Informationen wie die tägliche Dosis sowie Zeitpunkt der Anwendung siehe Fachinformation von Pfizer..

Nebenwirkungen und Gegenanzeigen:

Zwei aktuellen Studien (1) auf der Jahrestagung der American Diabetes Association in Washington 2006 zeigten, dass Exubera im Allgemeinen nicht schlechter verträglich sei als subkutanes Insulin. Die einzige Nebenwirkung, die öfter unter Exubera vorkam, war leichter Husten, der wiederum bei den meisten Patienten vorübergehend war und mild verlief.

Im Fachinformation werden Husten und Hypoglykämien als sehr häufig angegeben.

Wichtigste Kontraindikationen sind Lungenkrankheiten wie Asthma, COPD (Chronisch obstruktive Lungenkrankheit), Bronchitis und Emphysem. Raucher müssen mindestens 6 Monate abstinent sein.

Für weitere Informationen über Nebenwirkungen und Komplikationen siehe Fachinformation von Pfizer.

Fazit

Das inhalative Insulin Exubera® ist ein großer Fortschritt bei der Therapie der Diabetes-Patienten. Es eröffnet auch perspektivisch gesehen ganz neue Möglichkeiten der Insulin-Handhabung. Trotz der kritischen Haltung der deutschen QIWG wird das inhalative Insulin -wenn keine katastrophalen Nebenwirkungen in der Breitenanwendung bekannt werden- sich sicherlich etablieren.

Das neue Präparat kann zu einer Besserung der Lebensqualität der Diabetes-Patienten führen. Denn es ist schon ein qualitativer Unterschied, ob die Patienten mehrmals am Tag Insulin aufziehen und subkutan injizieren oder das Insulin ohne grosse Vorbereitung oder Pflege inhalieren können. Zwar werden Verzögerungsinsuline bei vielen Patienten weiterhin gespritzt werden müssen, diese werden jedoch in der Regel einmal oder zweimal am Tag (morgens und/oder abends) verabreicht.

Genauso die Größe des Inhalators, Mannkind hat eine handgroße Version, Pfizer hatte einen riesigen Inhalator den die Diabetiker nicht einfach überall mitnehmen konnten!

Wirft aber die Frage auf, ob dies im Behandlungsalltag relevant ist. Wie schon mal erwähnt, ist mir völlig klar, dass letztlich der Behandler die Entscheidung trifft, ob es für seine Therapie ein Vorteil ist.

Auch möchte ich hier nichts schlechtreden, ich mache mir nur paar Gedanken zum Thema.

Das von Novo Nordisk entwickelte inhalative Insulin war auch besser, ist aber aufgrund der schlechten Marktaussichten nie eingeführt worden.

Auch schon heute spielt die Zeit bis zum maximalen Wirkeintritt eine Rolle in der Therapie.

Wenn man bedenkt, dass Humaninsulin seine max. Wirksamkeit nach etwa 2-3,5 Std. hat und Analoginsulin nach 1-2,5 Std. sollte man meinen, dass die Analoginsuline den Vorzug bekommen sollten.

Es ist aber so, dass Humaninsulin noch immer deutlich höhere Verordnungszahlen aufweist, obwohl sie keinen Preisvorteil haben.

Ein weiterer Punkt lässt mich auch meine Zweifel nicht über Bord werfen.

Die allermeißten Diabetiker sind die des Typ2. Von diesen bekommen die meißten eine möglichst einfache Therapie mit einem langwirksamen Insulin + einem oralen Antidiabetikum, einfach weil es mit weniger Aufwand verbunden ist, nicht weil die Therapie besser wäre.

Diese lange Wirksamkeit ist mit Afrezze natürlich nicht zu erreichen.

Nun, wie gesagt, ich möchte hier niemanden etwas ausreden.

Ich schließe auch nicht aus, dass das Produkt erfolgreicher sein kann, als die früheren Kandidaten.

Aber ich bin dennoch der Meinung, wenn es auf den Markt kommt, wird es ein Nischenprodukt sein.

Es gibt inzwischen auch eine Vielzahl sehr guter neuer Therapien des Typ2, was zusätzlich den Markt enger macht und es werden in den nächsten 3 Jahren einige folgen.

Wie dem auch sei.

Für dich und andere die investiert sind hoffe ich, dass ich mit meiner Einschätzung falsch liege und würde jedem ein erfolgreiches Investment gönnen, keine Frage.

Beste Grüße!

Ich denke aber die nadelfreie und einfachste Anwendung macht Mannkind zum Game-Changer in Sachen Diabetik!

Alfred Mann, der CEO, hat schon mit seiner Insulinpumpe das richtige Händchen gehabt und nun nach einer Dekade und einer Milliarde privater Investition von Ihm, wird die Ernte bald eingefahren!

Auch eine Übernahme von Ely Lilly ist immer wieder im Gespräch zu 12,50 US Dollar pro Aktie!

Will MannKind's Afrezza Succeed Where Pfizer's Exubera Failed?

Follow SeekingAlpha

See all from SeekingAlpha

More from SeekingAlpha:

Orthofix Is a Value Buy as Orthopedic Industry Nears Bottom

Alexza Pharma Clears Hurdles Towards Approval for Agitation Drug

Kohl's: This Dominant Retail Stock Has Never Been So Cheap

Article Tools:

Buzz Up! Stumble It Tweet It Facebook LinkedIn Share It Referenced Stocks

LLY 0% Rate It

MNKD 0% Rate It

NVGN 0% Rate It

PFE 100% Rate It

Posted 7/26/2010 10:08 AM by Rockford Coscia from SeekingAlpha in Investing, Stocks

0 comments | Like itDon't like it Referenced Stocks: LLY, MNKD, NVGN, PFE Rockford Coscia submits:

This December, Afrezza, MannKind's ( MNKD ) inhalable insulin therapy for prandial (meal-time) management of blood glucose in diabetics, faces FDA decision. Afrezza's path to approval is well worn and bloodied, most notably by an approval and subsequent market withdrawal of Pfizer's ( PFE ) Exubera. Other inhalable therapies have also been attempted by such high-powered partnerships as Alkermes/Eli Lilly ( LLY ) and Aradigm/Novo Nordisk ( NVGN ); all abandoned in the wake of Exubera's withdrawal. Currently Afrezza is the only form of inhaled insulin still under FDA review.

With the market failure of Pfizer's Exubera, potential investors in MannKind's endeavor must address why Afrezza will not suffer the same market setbacks assuming a favorable decision by the FDA in December. MannKind has, of course, amassed a number of reasons to convince investors that Afrezza will become a market blockbuster with varying degrees of substance.

I wish to address the three biggest reasons I think Afrezza will succeed where Exubera failed: a demonstrated superiority over injectable therapies, increased patient and doctor compliance, and overall cost of the therapy.

Afrezza's Superiority Over Conventional Therapies

Soon after Pfizer's Exubera was approved, a review found that inhaled insulin at the time, including Exubera, "appears to be as effective, but no better than injected short-acting insulin." The reason for this is likely due to the fact that the insulin contained within Exubera is in its heximeric form.

Afrezza, on the other hand, is different. Afrezza's insulin is broken into its monomeric components, resulting in significantly shorter time to peak insulin levels (14 minutes for Afrezza vs. 49 minutes for Exubera). This monomeric formulation is reputed to more closely mimic the natural insulin response of healthy individuals as well as decrease the risk of hypoglycemia and weight gain.

In addition, MannKind has found Afrezza to be more effective at controlling postprandial glucose excretion and reduces glycosylated hemoglobin (HbA1c) levels - reducing possible vascular complications associated with diabetes. Unlike Exubera, the monomeric Afrezza offers a clear advantage over traditional injectable therapies.

Increased Convenience of Afrezza

The big draw any sort of inhalable insulin offers, of course, is the potential for the patient to avoid constant needle sticks for meal-time glucose control. While it seems that convincing a population of patients to ditch constant needle-sticks in favor or an inhalable therapy, Exubera highlights just how difficult that may be. Exubera's oft-maligned inhaler can only be described as 'bong-like'. While it collapsed into a cylinder about the size of a soda can, the appearance upon inhalation made users look, quite simply, ridiculous.

Pfizer's Exubera

MannKind's Afrezza

Afrezza inhalers, on the other hand, are small enough to slide into a pocket, are discreet, and won't arouse suspicions if you are pulled over by the police with it in the passenger seat. One other consideration worth mentioning is that the Afrezza inhalers are breath-activated, where Exubera required an 'activation while breathing' process for administration. Patients and doctors should find the actuation process much more convenient and reliable.

Cost

Whether or not Afrezza will be able to gain significant market share will ultimately come down to price. The cost of a day of treatment for Exubera was reported to be approximately $5 a day, compared to $2 or $3 for traditional injectable insulin. While it would appear that the cost per day of treatment has not been settled upon with Afrezza, some reports have stated the price will be offered at a 10-20% premium over traditional injectable therapies. At that cost, it would be reasonable to believe that MannKind can indeed gain a respectable share of the insulin market. Keep watch for an announcement from MannKind on the official cost of therapy, as a significantly higher cost of therapy - say similar to that of Exubera - may seriously impact Afrezza's prospects.

Summary

Afrezza is not without challenges heading into its December FDA decision and beyond. However, having apparently addressed the efficacy, convenience, and cost issues associated with Exubera, Afrezza stands a significantly better chance at capturing a larger portion of the insulin market. A recent Bank of America/Merrill Lynch survey of 100 physicians showed that MannKind could achieve a peak penetration of 15% of the insulin market - although that rate was adjusted down to 2% by the analysts due mainly to the failures of Exubera. Afrezza offers a significant improvement over existing therapies and should not be maligned by its ungainly predecessor.

Disclosure: No positions

See also Buffett Loads Up on J&J on seekingalpha.com

Read more: http://community.nasdaq.com/News/2010-07/...oryid=29932#ixzz17azFwiog

Ist ja auch gut so, sonst wäre es doch viel zu einfach und überhaupt nicht spannend!!

Dann schauen wir doch einfach mal, was sich so tut. Wie schon gesagt, wünsche ich allen ein gutes Investment.

Ich habe mich vor einer Woche für das unternehmen Lexicon entschieden, die ja einen anderen Therapieansatz haben.......mal sehen.....vielleicht klappt es.

Aber wie du schon so richtig sagst.....es gibt nie eine Garantie für die Zulassung.

Da ich schon viele Jahre im Diabetes-Geschäft und Pharmabereich bin, bin ich vielleicht manchmal doch zu kritisch......aber andererseits habe ich in all den Jahren schon so viele "Hoffnungsträger" gesehen, die dann schnell tot waren.

Ich bin gestern, trotz meiner Bedenken, mit einer kleineren Position eingestiegen.

Deine Argumente haben mich zum Nachdenken gebracht........musste mal die Brille des deutschen Gesundheitssysthems ausziehen und die Sache Global bewerten.

Insofern musste ich mir dann eingestehen, dass ich die Situation bisher doch zu pessimistisch gesehen habe......na, und schließlich war ich dann noch mutig und habe zugegriffen...

Die Chancen stehen nicht ganz schlecht, hier was zum aufwärmen:

Thursday, December 9, 2010The Keys to Unlocking Billions for MannKind’s Afrezza

Biotech investors are always looking for the next big advancement that will become a mega-blockbuster. Human Genome sciences continues to be a valuable company because of the prospects for Benlysta, which will be the first new therapy to treat Lupus in 50 years. Their market cap is still close to $5B Billion, with a lead drug expected to do around $1.5B a year and approval isn't even in hand yet. Dendreon is valued at over $5B and Provenge will only do $1B or so a year. However, since it is the first immunotherapy for cancer available, it remains hot. Who cares about a better insulin? Insulin isn’t sexy -- it has been used to treat diabetes for 90 years. Exubera was supposed to change all of that with an inhaleable form of insulin and was forecasted to do $2B a year in annual sales. Instead it was an utter failure and now nobody cares about inhaleable insulin, less alone a better insulin. In my last article on MannKind’s Afrezza, I tried to address why the Street and Bear Analysts are completely wrong when it comes to Afrezza’s potential and the comparison to Exubera’s failure is like comparing a Yugo to a Gulfstream. In this article, I will discuss the keys to unlocking the Afrezza’s multi-billion dollar potential.

In a report released in late November by national healthcare insurance giant, UnitedHealth Group, they estimate that more than half of America will be a diabetic or pre-diabetic by the end of the next decade at a cost of $3.35 trillion to our healthcare system. According to a recent report from the CDC, a child born today has a 1 in 3 chance of becoming a diabetic in a few decades if things don’t change in our country and we could wind up with as many as 500M worldwide at the current rate of expansion. Outside of Obesity, there is no bigger cost to the world’s healthcare system.

Insulin, even though it has been around for almost a century, is still the best treatment for type 2 diabetics that can’t control the disease through lifestyle modification and metformin alone. Type 1 diabetics don’t have choice but to take insulin but they make up only 5% or so of the overall population of diabetics. Insulin lowers HbA1c better than any form of newer therapy but it is often a treatment of last resort when it comes to type 2 diabetes. Why? Because there a number of barriers for introducing its use that keep it on the back burner for as long as possible. Overcoming these barriers is the first key to unlocking Afrezza’s potential. Even with these barriers, Insulin is still a $10B product worldwide.

In an article published by Irl Hirsch, M.D. (Univ of Washington School of Medicine) on 11/16/2005 entitled “Optimal Initiation of Insulin in Type 2 Diabetes,” Dr. Hirsch writes about the impact insulin therapy can have on Type 2 Diabetics and the optimal initiation plan to use insulin. Dr. Hirsch states that “it can be anticipated that most patients will eventually require insulin therapy to achieve and maintain glycemic control.” Regarding the ADA’s goal of maintaining a HbA1c < 6.5%, “Such stringent levels of glucose control cannot generally be maintained with oral antidiabetic drugs (OADs) alone. However, overall rates of insulin use for type 2 diabetes in the United States are very low. Approximately 11% of patients are treated with a combination of insulin plus OADs and another 16% receive insulin monotherapy. An A1C < 7.0% is only achieved in 36% of patients. Higher rates of glycemic control have been reported among patients with type 2 diabetes who are receiving care from endocrinology practices (61%) and may in part be due to a higher rate of insulin use.”

Dr. Hirsch’s description of the barriers to insulin therapy is spot-on in my opinion, “delays in initiating insulin may stem from both physician and patient barriers. Negative patient perceptions regarding insulin include fear of injections and hypoglycemia. In some cases, patients may perceive insulin as a sign of their personal failure to control the disease. Clinician concerns include hypoglycemia, weight gain, and the misconception that elevated insulin increases cardiovascular risks. In addition, both clinicians and patients may consider insulin therapy to be complicated and labor-intensive.”

Let’s look at how Afrezza addresses each of the barriers to insulin therapy:

Fear of Injections: This is the most common reason cited for delaying insulin therapy. Nobody wants to take a shot, especially not 4 times a day. Under the current standard of care, Basal insulin is typically introduced to patients starting insulin therapy before Prandial (mealtime) insulin. The reason being is 1 shot a day is easier to convince a patient to take than 3 or 4 mealtime injections. This completely changes with Afrezza. Afrezza opens up the door for physicians to start insulin far earlier in the treatment plan than has ever been done before. Ironically, this was the main benefit for Exubera and why their sales were expected to be over $2B a year. However, Exubera had a terrible device design and also failed to address the remaining barriers to entry. Even though Exubera didn't have a good device and no clinical benefit over injected insulin, the patients that did try it, actually loved it!

Fear of Hypoglycemia: Hypoglycemia is the number 1 side effect of insulin. This happens where there is too much insulin in the body, resulting in low blood sugar. This is why titrating the proper dose of insulin is so important with injected insulin. Hypoglycemia can be mild, just causing you to feel bad but sometimes can be severe, resulting in a coma or even death. With Afrezza, this risk is greatly reduced compared to injected insulin. The risk of severe hypos is reduced by 63%! This is a result of the quick method of action for Afrezza resulting in peak insulin levels at 14min, which quickly leaves the body – similar to a normal persons insulin response to a meal. This is a far contrast to the currently gold standard mealtime insulin products that peak at 52min and Exubera, which peaked at 49min.

Insulin is complicated to Dose and Manage: This is the final barrier to overcome and it will take a good education / sales program to effectively address it. Overtime as physicians become more comfortable, it will no longer be an issue. With Afrezza, the dosing is very simple and typically, you would use the same dosage before every meal. This means there is very little titration that needs to happen before a meal – just basic carbohydrate estimates. It also means there won’t be a need for rigorous self-monitoring of blood glucose. Afrezza’s simplicity and elegance will greatly ease the overhead typically associated with insulin therapy. Overcoming this barrier quickly will be influenced greatly by the next key to unlocking Afrezza’s potential.

A good partner is the final key for unleashing Afrezza’s paradigm-shift in the market. This will also be the largest catalyst to the stock price in my opinion. MannKind needs a partner that desperately needs to expand their diabetes program. A company like Merck (MRK) or AstraZeneca (AZN) would be a great fit. Whoever the partner is, proper execution of the marketing plan will be the key to Afrezza’s quick adoption in the market. With the right partner in place, MannKind could quickly reach the planned launch capacity to support 400,000 patients. At $2K per patient, that equates to $800M a year in revenue. With just $100M in expansions to MannKind’s award-winning plant in Danbury, CT, capacity would go up to 2M patients or $4B in annual sales. It is also worth noting that MannKind already owns enough insulin (at a cost of $3M) to fuel the first $10B in sales. Gross margins for the initial few years on the market will be astounding.

Price Predictions: I usually don’t like to guess at short term price movements in stocks. I’m a long term investor that cares less about the short term price fluctuations. I’m more concerned about the price 3 to 5 years from now as Afrezza is widely used in the US and the rest of the world. However, I will go ahead and make a guess since I get asked about this frequently. All of the technicals for MNKD look very good right now with a clear reverse head and shoulder pattern in place. A break above the $7.20’s would indicate a run to $9 or even $10 prior to the 12/29 PDUFA. If that happens, approval would trigger price appreciation to the upper teens if not $20. A complete response letter would cause a major sell off but how low would depend on what was in the CRL. If it is a slight delay then perhaps back to $5, if something more onerous then perhaps $3. Partnership is the biggest key to the price appreciation. Once a Big Pharma has signed on to commercialize Afrezza, we should have some insight into their guidance for the potential. If MannKind and that partner say that Afrezza is a $2-4B drug in the US, which it is, then arbitrage will take place and MNKD would be justified to have a marketcap higher than HGSI or DNDN. Something over $5B is reasonable to expect.

However, before any of this can happen, the FDA needs to approve Afrezza. It is possible of course the Bears are right and the FDA will issue another CRL. I don’t think they will but many do and that is why the stock is less than $10 right now. With December 29th only days away, we’ll all know soon. I for one am hoping for an early Christmas present this year.

Ist immer noch wenig los hier im Forum...außer uns scheint hier keiner interessiert zu sein. Hätte hier mehr Teilnehmer erwartet, als ich letzte Woche erstmals reingeschaut habe.

Bist du noch in anderen Foren unterwegs, in denen der Austausch etwas reger ist?

Aber mir macht das Nichts aus Perlen zu entdecken und nicht den Lemmingen hinterherzulaufen, kann natürlich auch schief gehen!

Stimmt, man sollte seinen eigenen Weg gehen, letztlich ist man ganz allein für die Entscheidungen verantwortlich, die man trifft.

Aber etwas Austausch ist manchmal doch nicht schlecht, hat ja hier auch meine Überlegungen beeinflusst.