AGNICO EAGLE MINES mit 50% Potenzial

Glänzende Aktie

Der Goldpreis hat sich zuletzt prächtig entwickelt, der Aufwärtstrend sollte sich fortsetzen. Top-Chancen auf Gewinne mit Gold bietet die kanadische Agnico-Eagle Mines.

Selten war der Markt so nervös wie derzeit. Wie geht es weiter mit der US-Konjunktur? Ist der Aufschwung der Weltwirtschaft vorbei? Gibt es einen Börsencrash? Diese Fragen dürften die Anleger noch eine Weile quälen. Parallel könnte es in den kommenden Monaten einen großen Gewinner dieser Entwicklung geben: Gold. Wie DER AKTIONÄR bereits in Ausgabe 04/08 geschrieben hat, gilt Gold traditionell als sicherer Hafen in unsicheren Zeiten.

Kanadische Perle

Goldaktien sollten deshalb in keinem Depot fehlen. Besonders attraktiv ist Agnico-Eagle Mines. Das kanadische Unternehmen wurde vor 36 Jahren gegründet und zählt zu den alten Hasen in der Branche. Derzeit produzieren die Kanadier im Jahr 250.000 Unzen. Bis 2010 soll die Förderung auf 1,2 Millionen Unzen steigen. Sämtliche Entwicklungsprojekte in Kanada, den USA, Finnland und Mexiko sind weit fortgeschritten. „Bis 2010 werden wir in fünf neuen Goldminen die Produktion starten“, so Agnico-Chef Sean Boyd.

Lob vom Experten

Darüber hinaus ist das Unternehmen ein Low-Cost-Produzent. Pro Unze Gold muss Agnico nur 230 Dollar aufwenden, was ein gutes Stück unter dem Branchendurchschnitt liegt. 480 Millionen Dollar Cash und 300 Millionen Dollar Kreditlinie sind zudem ein solides finanzielles Polster. Kein Wunder, dass Michael Jalonen, Rohstoffanalyst von Merrill Lynch, viel von Agnico hält. Seiner Meinung nach sollte der Titel 2008 besonders gut abschneiden.

Fazit

DER AKTIONÄR erwartet, dass der Goldpreis seinen Aufwärtstrend fortsetzt. Dies und die bevorstehende Produktionsausweitung dürften Agnico beflügeln. Auf Jahressicht hat das Papier 50 Prozent Potenzial.

Auszug

"

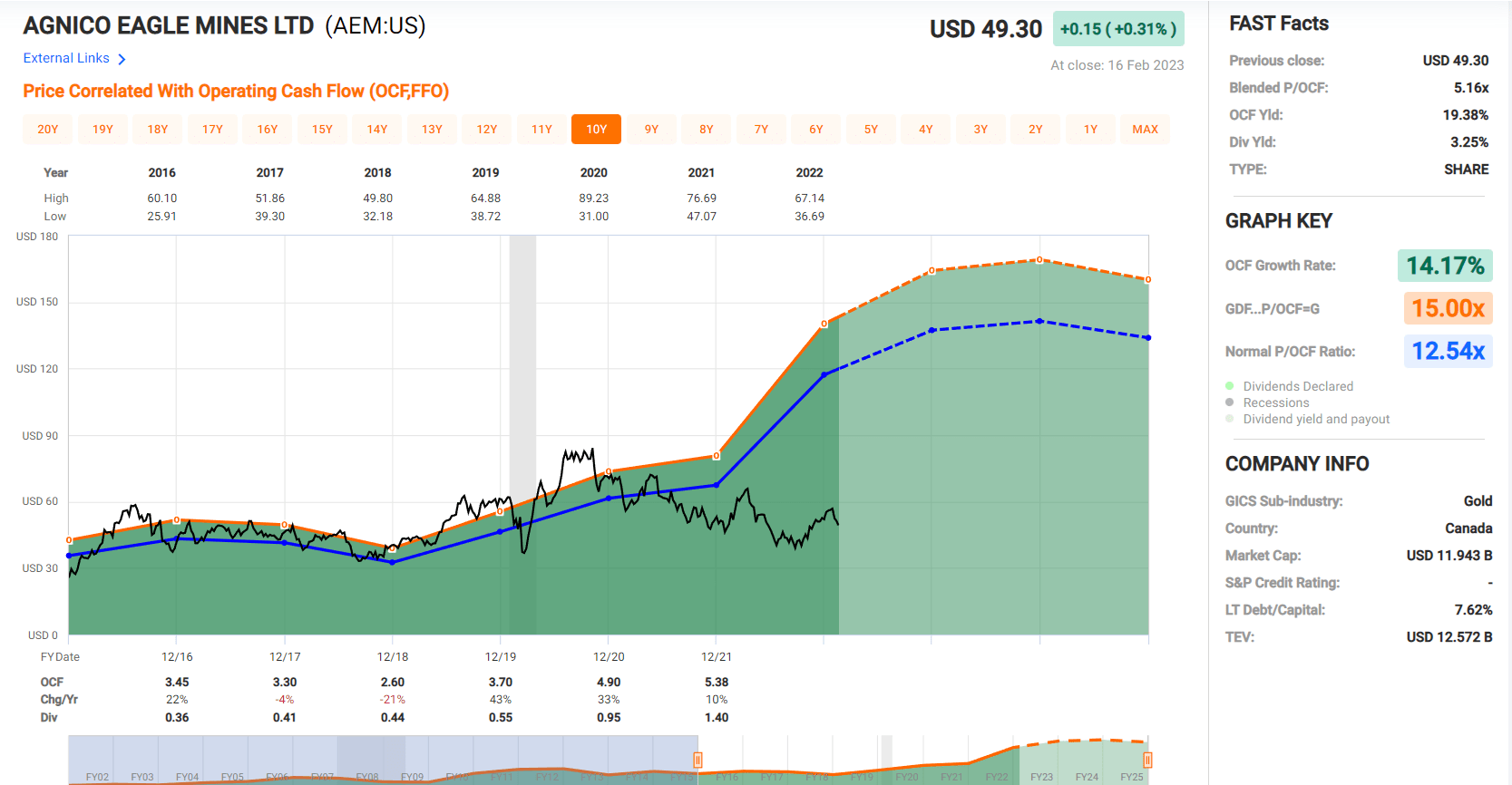

Looking at the chart above , Agnico has historically traded at 12.5x cash flow, and I would argue that a multiple of 13.0 is more than reasonable, given that it's the premier major producer with favorable jurisdictions and attractive margins. Based on conservative FY2023 cash flow estimates of $4.50, this translates to a fair value for the stock of US$58.50, pointing to 20% upside from current levels. However, this fair value estimate is based on what will be a weak year for Agnico, and it doesn't place any value on its strong development pipeline or exploration upside, where I think we can easily assign a value of $5.0+ billion (Santa Gertrudis, Upper Beaver, Wasamac, Hammond Reef, Hope Bay, San Nicolas [50%], exploration upside). It also doesn't place any value on organic growth at existing assets like Detour Lake."

"Given that valuing the stock on cash flow understates the company's long-term potential, I believe the best way to value Agnico Eagle Mines Limited stock is on a P/NAV basis. Based on an estimated net asset value of ~$23.7 billion after adjusting for G&A expenses, and assigning a 1.45x P/NAV multiple given its strong history of reserve replacement, I see a fair value for Agnico stock of ~$35.0 billion. After dividing by ~490 million shares (year-end 2023), this translates to a fair value for the stock of US$71.40, translating to a 44% upside from current levels or ~47% upside on a total return basis.

Importantly, this doesn't account for upside in the gold price, with these assumptions based on a $1,700/oz gold price, in line with the three-year average. Given its undervaluation, I continue to see Agnico as one of the best buy-the-dip candidates sector-wide."

Chart Cashflow

https://static.seekingalpha.com/uploads/2023/2/17/...38073_origin.png

{kind=link}

https://seekingalpha.com/article/...eagle-mines-a-softer-2023-outlook

******

Prognosen

https://www.marketscreener.com/quote/stock/...ITE-1408914/financials/

******

Saisonalität: Bodenbildung im März, Hoch August

https://charts.equityclock.com/...le-mines-ltd-nyseaem-seasonal-chart

Angehängte Grafik:

agnico_prognosen.jpg (verkleinert auf 63%)

agnico_prognosen.jpg (verkleinert auf 63%)

AEM ist extrem überverkauft, fundamental alles i.O., das Gap bei 54$ sollte wie ein Magnet wirken sobald die 200er bei ~48$ genommen wird. als starkes Zeichen werte ich auch, dass trotz Divi-Abschlag der Kurs gestern gestiegen ist; bin long

Optionen

| Boardmail an "chivalric" |

Wertpapier: Agnico-Eagle Mines Ltd. |

Optionen

| Boardmail an "chivalric" |

Wertpapier: Agnico-Eagle Mines Ltd. |

Optionen

| Boardmail an "chivalric" |

Wertpapier: Agnico-Eagle Mines Ltd. |

https://www.bnnbloomberg.ca/video/...nd-mine-agnico-eagle-ceo~2794208

Q1 2024 Earnings Forecast for Agnico Eagle Mines Limited Issued By Raymond James (TSE:AEM)

Posted by Defense World Staff on Mar 23rd, 2024

Gibt es für dasselbe auch einen zielführenden Link ?

Optionen

| Boardmail an "Teras" |

Wertpapier: Agnico-Eagle Mines Ltd. |

... auf das von Dir gemeinte Video gefragt, damit ich mir dasselbe auch anschauen kann ...

Nichts für ungut:

Der olle Teras.

Optionen

| Boardmail an "Teras" |

Wertpapier: Agnico-Eagle Mines Ltd. |

... den ich hiermit wie folgt übersetze: https://www.youtube.com/watch?v=UaTsqnOlNNI ...

Optionen

| Boardmail an "Teras" |

Wertpapier: Agnico-Eagle Mines Ltd. |

Angehängte Grafik:

2024-04-08-agnico-eagle-tipp-des-tages.png (verkleinert auf 79%)

2024-04-08-agnico-eagle-tipp-des-tages.png (verkleinert auf 79%)