against all odds

Seite 101 von 117 Neuester Beitrag: 08.04.20 16:14 | ||||

| Eröffnet am: | 22.03.13 19:18 | von: Fillorkill | Anzahl Beiträge: | 3.904 |

| Neuester Beitrag: | 08.04.20 16:14 | von: Fillorkill | Leser gesamt: | 344.292 |

| Forum: | Börse | Leser heute: | 38 | |

| Bewertet mit: | ||||

| Seite: < 1 | ... | 98 | 99 | 100 | | 102 | 103 | 104 | ... 117 > | ||||

Die öffentliche Hand geht (ausserhalb der Brüningzonen) recessiv antizyklisch ins Deficit, um das Bedürfnis der Privaten nach sicheren Assets zu beantworten:

Autor http://www.interfluidity.com/v2/6174.html

Private sector net financial assets are “special” precisely because they are not backed by domestic real assets, but instead by promises that are credibly independent of domestic real asset values, especially promises of states. Saving that takes the form of real stuff, whether that stuff is directly held or hidden behind financial claims, is inherently risky. House prices fall.

If you own a factory, or shares in a firm that owns a factory, the factory can burn down. Even if you hold a diversified stock portfolio, you will find it subject to wild swings in value. If you own private sector debt, you expose yourself to credit risk. If you own a diversified portfolio of domestic stocks and bonds, your own circumstances and that of your investment portfolio will be correlated in an unpleasant way. The times when you lose your job and need to draw on savings are likely to be the same times when stocks have crashed and people are defaulting on their debts. People desperately covet assets that are divorced from the risks of the domestic real economy. And that is precisely what “net financial assets” are.

Net financial assets are special, because they serve insurance functions that assets produced by the domestic private sector simply cannot provide. When households are risk-averse, they covet these assets especially. For firms, these assets offer protection against insolvency risk that real assets, whose values both fluctuate idiosyncratically and covary with the real economy, cannot provide. MMT economists often suggest that if the public sector fails to accommodate the private sector’s appetite for net financial assets, recession and financial instability will result. That makes sense.

It’s conventional, if a bit vapid, to describe recessions as times when “animal spirits” are low, when people are risk averse. But what matters is not the courage in people’s hearts (or lack thereof). What matters is how people behave. If people’s behavior is counterproductively risk averse, you can encourage greater risk-taking by offering insurance. That’s precisely what injections of “net financial assets” into an economy provide. If firms are teetering on the brink of bankruptcy, you can flood the economy with safe assets they can use to shore up their balance sheets to reduce their risk of default.

That’s precisely how the United States saved its banks in 2008 (for better or for worse). The headline bailouts and TARPs and accounting forbearance were all expedients to keep those firms alive until a flood of assets immune to correlated private sector collapse could find their way onto bank balance sheets (with the help of opaque subsidies). Those special assets are “net financial assets”.

“Net financial assets” are a heterogeneous category. They include both claims against the domestic state and claims on foreign public and private sectors. A claim on a foreign firm in foreign currency does not provide the same insurance as claim against the domestic government in domestic currency. Nevertheless, claims on the foreign sector do provide insurance against domestic shocks that do not impair the foreign counterparty. And note that contrary to naive financial theory, which predicts developed economies will net-accumulate claims on emerging economies to invest in their growth, in practice emerging economies tend to net-accumulate claims on developed economies. The insurance function of safer foreign assets outweighs the investment function of accepting foreign capital (or at least it has since the Asian Financial Crisis).

For firms and households in an emerging economy, foreign claims and claims on government are both useful insurance. In developed as well as emerging economies, negative positions with respect to foreign creditors increase the domestic private sector’s exposure to risk as surely as indebtedness to the state would, assuming debt contracts are uniformly enforced.

All this terminology — private sector surplus, net financial assets, etc. — is associated with heterodox, lefty MMT, but it maps very nicely to discussion of “safe asset shortages” in the mainstream financial press or Gary Gorton’s schtick on the importance of “informationally insensitive” assets. The main difference has to do with whether we can or ought to rely upon the domestic private sector to produce these kinds of assets. The MMT analysis, by construction, excludes private sector “triple-A” assets, where people like Gorton emphasize a role of private sector in producing assets that might provide this sort of insurance. The MMTers have it right. The domestic private sector simply cannot produce assets that provide insurance against systematic risks of the domestic economy without the help of the state. (Gorton tacitly recognizes this when he suggests the state should supervise and guarantee assets produced by shadow banks like it insures bank deposits. No thank you.)

The insurance function of “net financial assets” is not unambiguously a good thing. Net financial assets are special precisely because they provide insurance against systematic risk. When net financial assets are claims on foreign debtors, they are not so problematic, they just represent a form of diversification that can insure against domestically (but not globally) systematic shocks. Claims against the domestic state, however, offer safety to their holders in a manner that can be quite dangerous to the rest of us. “Insurance” against a truly systematic shock is necessarily a zero-sum game.

If we are all collectively poorer, the only way the state can make some claimants whole is by shifting their share of the aggregate loss to people who don’t hold the government’s promises. We’ve experienced this very painfully over the past decade, as both the European and American policymakers refused to accept any risk of inflation (thereby prioritizing the value of past promises). Policymakers chose to make absolutely sure that holders of state assets would be made whole in real-terms, and imposed severe costs on debtors and the marginally employed to do so. (I think policymakers overshot the inherent zero-sum-ness of providing insurance during a systematic shock and have played a sharply negative-sum game.)

It would be better, I think, if states downgraded the insurance they provide by weakening the promise they make to asset holders from price stability to an NGDP path target. And I worry much more than I think most MMT economists do about the unjust distribution of risk-bearing that might accompany a large stock of net financial assets very unequally distributed. (Unusually, I’m with Greg Mankiw on this one.) I think the economy includes people who are already overinsured by their stock of net financial assets, and those people tend disproportionately to accumulate new issues. So we should think more about how we can accommodate private sector entities’ need for some degree of insurance by redistributing existing net financial assets rather than creating new ones.

This sentence is a pithy conclusion.

Optionen

Optionen

Angehängte Grafik:

my_spending_is_your_income__chart_paul_krug....png (verkleinert auf 68%)

my_spending_is_your_income__chart_paul_krug....png (verkleinert auf 68%)

ACEMAXX-ANALYTICS

link: http://acemaxx-analytics-dispinar.blogspot.de

https://twitter.com/acemaxx

herkunft: anglo-saxon (krugman)

sprache: deutsch

schwerpunkt: statistik

Optionen

Optionen

Optionen

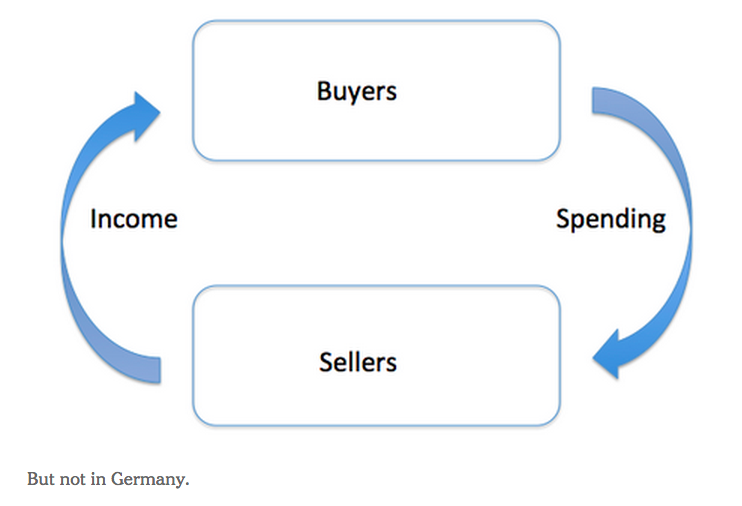

'Sinn will Mindestlohn abschaffen'

'Der ifo-Präsident fordert zur Bewältigung der Flüchtlingskrise eine neue Agenda 2010. Die Deutschen sollten länger und billiger arbeiten, fordert Sinn in der ZEIT.'

'..Aus seiner Sicht müssen die Deutschen zudem länger arbeiten, um die Kosten der Integration der Flüchtlinge stemmen zu können. "Wir sollten lieber das Rentenalter heraufsetzen, um die Flüchtlinge zu ernähren... '

http://www.zeit.de/wirtschaft/2015-10/...inn-mindestlohn-sozialreform

Prof Unsinn demonstriert einmal mehr die perfekte Symbiose zwischen Angebotsfanatismus - je tiefer Aggregate Demand gedrückt wird, umso kräftiger sollen private Investitionen aufblühen - und der völkischen Sündenbocktheorie, die die Verantwortung für den sozialen Kahlschlag 'den Fremden' anlastet.

Wahr daran ist eigentlich nur der Nexus, dass wer die ökonomische Moral der Michel teilt, derzufolge ein gegebenes Stück Kuchen nicht beliebig oft verteilt werden könne, sich der ökonomischen Argumentation für die Einwanderungsgesellschaft beraubt.

'..In Germany, many communities, villages and cities, are taking in refugees and are doing very good work. But their means are insufficient. They lack the necessary funding to set up decent accommodation. Once again, our economic and financial policies are to blame. Because what is the case? Politicians discuss funding for day-care staff, accommodation and governmental aid within the iron framework of their restrictive economic policies, even when state and city budgets show surpluses. Once again, ideology clashes with rationality, although it is all really simple: invest now or you will overburden future generations in an intolerable manner.

There is a great and genuine willingness of the vast majority of German politicians to act towards the refugees in a rational and humane way, without xenophobic resentment or religious prejudice. Their position remains nonetheless highly irresponsible as long as they stick to their nonsensical fiscal and economic policies. Nothing will be solved as long as they strive for trade and budget surpluses and never understand the inherent destructiveness of such policies...'

http://www.flassbeck-economics.de/the-boat-is-far-from-being-full/

Optionen

Optionen

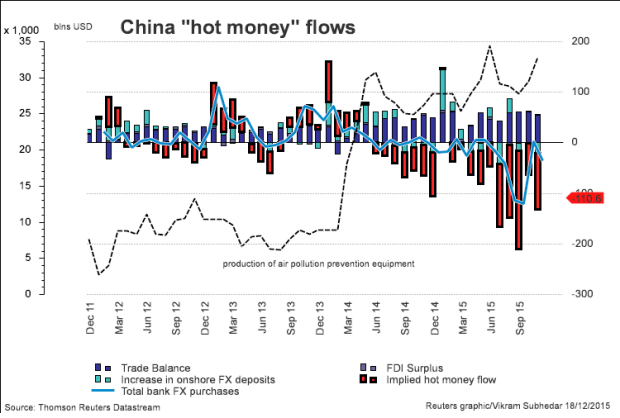

Angehängte Grafik:

hot-money-flows-vikramreuters-dec1815.png (verkleinert auf 82%)

hot-money-flows-vikramreuters-dec1815.png (verkleinert auf 82%)

At the most basic level, the entire economy and financial system is highly unnatural. It is entirely made up out of thin air. Stocks, bonds, cash, money – all of it is just a figment of the human imagination conjured up from nothing to try to reflect the state of what is. In some ways the financial system and the monetary system is real as it reflects things in the real world that we transfer from one another like real goods and services, but in another sense it is a total fiction in that it also reflects things like intangible services and goodwill. But even those tangible goods are highly unnatural – iPhones don’t grow in the wild after all.

The point is that our entire economy is a human construct. It is created by animals who intervene in markets on a daily basis. We are all making discretionary decisions every minute of the day. There is no “natural” order to all of this. There is only the constant state of human beings manipulating an otherwise natural world. And that is, after all, what we are best at. We are the only animals on the planet constantly disrupting the natural order of things.

This is primarily the result of the fact that human beings run surpluses against all other things in nature. We utilize tools that ensure that we don’t have to rely purely on that “natural” order of the world. We don’t wait for the seasons for warmth. We conjure heat up by manipulating the natural order of things. We don’t wait for the migration of animals to feast on meat. We conjure it and store it up as we please. There is nothing “natural” about the way the economy and the financial system operate. It is, in fact, a giant manipulation of the natural world.

We usually hear about the “natural” state of the financial markets during some political diatribe. Or we hear about how discretionary intervention in the economy is bad. Or how anything other than passive investing is silly. All of these ideas are based on some flawed myth about a “natural” order in the economy or the financial markets. But this idea of a “natural” state of being ignores the fact that human beings only created an economy and a financial system because we have become masters of manipulating our natural surroundings. It is our greatest strength and perhaps our greatest weakness.

Optionen

Eine Gegenbewegung wird jetzt warscheinlich, aber wir befinden uns nicht mehr im Bullenmodus. Ob die Stimmung schon schlecht genug ist?

The past year’s pessimism in the face of continued economic improvements has within in a couple of days shifted to panic. Multiple forecasts for oil prices to plunge to $20 BBL, even $10 BBL were issued yesterday. One firm says “Sell Everything!” Yet, in the face of all this, the economics are quite sound. Why is the market panicking and not seeing the obvious economic strength?

...The majority of investors are Momentum Trend Followers. Momentum Investors believe that stock prices carry all the information necessary with which to make investment decisions. Economic fundamentals are not a factor in this approach except to find a reason to justify what they believe price trends are telling them. In other words, if the price trend is down, Momentum Investors will find an economic fundamental to support the trend, even if they are incorrect in doing so. It is the act of forcing numbers to tell one’s point of view even with misplaced reasoning. This is emotional investing.

Momentum Investing is emotional investing. It has no basis but for a price trend which ‘feels good’ or ‘feels bad’. There is no connection to fundamental returns with this approach. That ‘price trend’ is not an economic return measure is difficult for the majority of investors to grasp. Most think prices reflect the consensus analysis which is better than analysis by individuals. However, the overwhelming majority of investors do not use fundamentals. They do not know how to do so. Instead they believe that market prices rely on someone who does know how to do this and that markets price securities ‘more correctly’ and regardless of price level.

If revenues are higher than expected, then the price should go higher. If revenues under-perform expectation, then price should fall. This is crowd investing. This is investing on the psychology of expectations of other investors. This is what Momentum Investing is all about. Momentum Investing is the belief that a crowd of investors are better at understanding the value of a company than any other approach. When the majority carries the belief that someone who actually knows what they are doing is responsible for market prices then ‘Consensus Logic’ is not logical!

History reveals that major market corrections only occur when the fundamentals, the true fundamentals, have turned down. By ‘True Fundamentals’ I refer to economic activity. The combined day-to-day individual striving to improve one’s own and one’s family’s standard of living which shows up in increases in Employment, in Real Personal Income and Real Retail Sales. Major market corrections do not occur unless these economic indicators reflect a down-turn in these fundamentals. Today there is no evidence to support a correction!

‘Group Think’ has focused on oil prices as the primary indicator of economic activity and falling oil has panicked investors into believing an imminent correction is upon us. One firm even said “Sell Everything”! Oil prices are like any other prices. They are simply set by ‘Group Think’. With the strong US$ bet being made today by Hedge Funds which have dominated short-term pricing since 1995, we have witnessed considerable shifts in price levels for commodities, currencies and fixed income securities all of which become interpreted by Momentum Investors into illusionary economic misperception. Meanwhile, the economic fundamentals which continue to expand are lost as investors strive to explain price trends which are short-term psychological gobbledygook!...

Optionen

Myth 2: Printing money to finance budget deficits is inflationary

Myth 3: Budget deficits/high debt lead to high interest rates

Myth 4: Budget deficits are unsustainable

Myth 5: Debt is a burden on future generations

GMO Investing : https://www.gmo.com/docs/default-source/...and-delusions.pdf?sfvrsn=2

Optionen

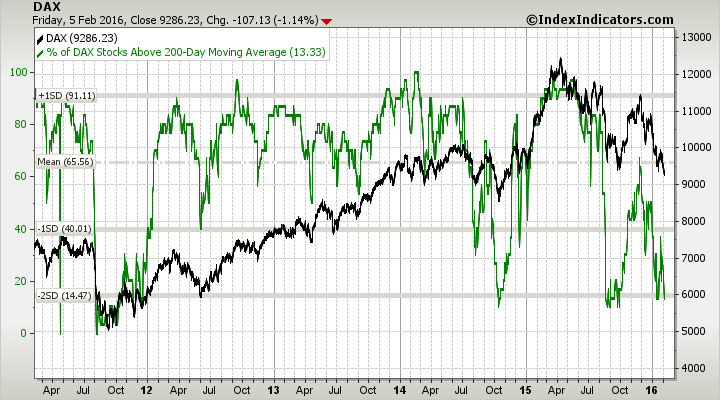

Leider sind die Amis noch nicht ganz so weit, weshalb ich persönlich außer Dollar Short noch nicht Investiert bin.

Angehängte Grafik:

dax-vs-dax-stocks-above-200d-sma-params-5y-....png (verkleinert auf 70%)

dax-vs-dax-stocks-above-200d-sma-params-5y-....png (verkleinert auf 70%)