Yingli/ Top Solarplayer Chancen und Einschäzungen.

Latin America has become Yingli Green’s key near-term focus as an emerging market, with plans to partner in Brazil to operate a PV module assembly plant.

Latin America has become Yingli Green’s key near-term focus as an emerging market, with plans to partner in Brazil to operate a PV module assembly plant.

Speaking at Yingli Green’s annual analyst event, held on the first exhibition day of Solar Power International, Robert Petrina vice president of sales and managing director of Yingli Green America, said that servicing key markets of Chile, Mexico and Brazil had become a “commitment” of the company.

Petrina noted in his presentation to the investor community that Brazil’s national development bank, BNDES, had included new local content requirements for solar projects to access very low interest rate project finance on the back of planned reverse (LER) auction’s for PV that are being held at the end of October, 2014.

To be competitive and a chance of winning bids in Brazil, module assembly at least would be required. Petrina added that “We will have to house local manufacturing in Brazil.”

According to the Yingli Green executive, negotiations on partnering with a local firm were well developed.

However, both Chile and Mexico were also very attractive to the company as the markets were becoming increasingly open to business for PV. Mexico was picked out by Petrina for having plans to target installations of around 38GW by 2024 and that PV retail grid parity in the country had already been effectively reached. This would lay the foundation for strong growth in demand for PV in the coming years.

Less optimism was displayed in discussing the MENA region. Petrina noted that countries such as Jordan were leading the way but that major potential markets such as Saudi Arabia could still take a few more years to build meaningful momentum.

Huge US demand

With respect to the US, Petrina said that the pending ITC cuts were generating “huge demand” for PV that would mean the US could compete with China for the largest market ahead of the ITC cuts in 2017.

Petrina said that there was even a new wave of US utility sector interest in PV that would push demand in the country higher.

However, the recent US anti-dumping ruling had made Yingli Green more cautious about its ability to capitalise and expand its shipments in the country.

Although stable module pricing had been beneficial to the company, duties meant that Yingli Green would have to adopt a measured approach to module supply as margins would be wafer thin.

The impression given by Petrina was that the company was being forced to be highly selective in its shipments levels and to which customers on the back of margin issues.

The executive was hopeful that some kind of agreement could still be reached with US agencies before year-end that could resolve key elements of the latest anti-dumping ruling obstacles to Chinese manufacturer’s ability to meet the huge demand in the US.

Gestern hat der chinesische Solarproduzent LDK Solar hat gestern in den USA Insolvenz angemeldet. Das Unternehmen hat in diesem Jahr bereits eine Anleihe nicht zurückzahlen können und befindet sich derzeit in Restrukturierungsmaßnahmen in Hong Kong und Cayman Islands. Das Unternehmen hat nun Insolvenzschutz nach Chapter 15 in Delaware angemeldet und 1,13 Mrd. USD an Schulden und 510 Mio. USD an Assets gemeldet. Die US-Töchter des Unternehmens haben Insolvenzschutz nach Chapter 11 beantragt. Die ADRs von LDK Solar brachen gestern um 23,5 Prozent auf 0,13 USD ein.

Yingli Green Energy hat gestern im Rahmen der SPI, welche derzeit in den USA stattfindet, mitgeteilt, dass der lateinamerikanische Markt kurzfristig der wichtigste Markt für das Unternehmen sein werde. Das Unternehmen will dazu Partner einer Modulproduktionsstätte in Brasilien werden, da man nur auf diesem Wege in Brasilien bestand haben könne. Verhandlungen mit einem lokalen Unternehmen seien weit fortgeschritten. Neben Brasilien sind Mexiko und Chile attraktive Märkte für das Unternehmen. In Mexiko existieren Pläne, Erzeugungskapazitäten von 38 GW bis zum Jahr 2024 zu errichten, wie ein ranghoher Vertreter von Yingli Green America mitteilte.

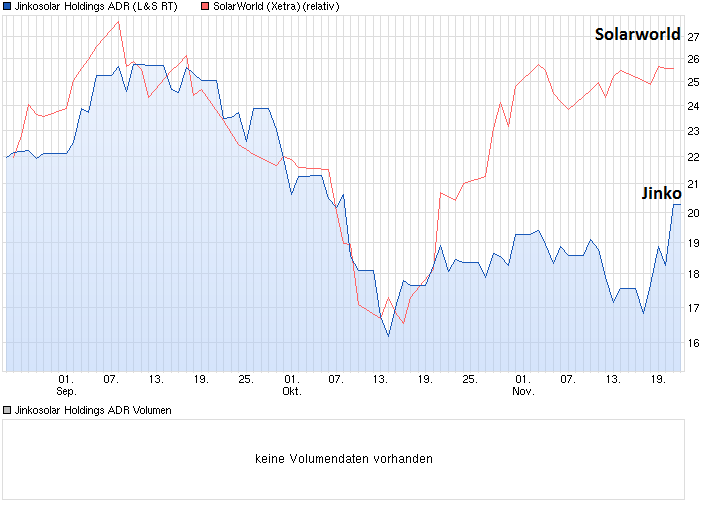

Die Papiere von Yingli Green Energy stiegen gestern um 2,7 Prozent auf 3,03 USD, JinkoSolar stiegen um 3,0 Prozent auf 24,09 USD, Trina Solar gewannen 2,7 Prozent auf 10,56 USD und Canadian Solar sprangen um 7,8 Prozent auf 30,85 USD nach oben. JA Solar verteuerten sich um 3,4 Prozent auf 8,27 USD und ReneSola kletterten um 2,9 Prozent auf 2,53 USD.

•Co announced that it has signed a landmark agreement to supply 120 MW of YGE 72 Cell solar panels for a 300 MW project in France. Upon completion this will be the largest solar power park in Europe.

•According to the agreement, Yingli Solar will ship more than 393,000 multicrystalline panels between December 2014 and June 2015

Positiv:

-für Yingliverhältnisse überraschend hohe Bruttomarge von 20,9%

-seit Ewigkeiten mal wieder ein Quartal mit operativem Gewinn

Negativ:

-Guidance für 2014 gekürzt um gut 10% von 3.6GW to 3.8GW auf 3.3-3.35 GW

-weiter hohe Schulden

Optionen

| Boardmail an "Juliette" |

Wertpapier: Yingli Green Energy |

Chinesische Solaraktien haben absolut miese Bilanzen und niedrige Eigenkapitalquoten....ist dem Dumpingkrieg geschuldet!

Optionen

| Boardmail an "Melmacniac" |

Wertpapier: Yingli Green Energy |

http://www.aktiencheck.de/exklusiv/...ktienkurs_Aktienanalyse-6149666

Yingli Solar’s loss per share in the reported quarter was narrower than the Zacks Consensus Estimate of a loss of 13 cents.

Revenue

Total net revenues were $551.5 million (RMB 3,385.2 million), down 6.8% from $591.6 million (RMB 3,649.4 million) in the third quarter of 2013. Revenues declined due to lower sales at the PV modules and PVsystems segment.......

Guidance

Yingli Solar revised its 2014 shipment volumes downwards expecting lower solar panel demand worldwide. The company now expects PV shipment volumes in the range of 3.30–3.35 GW (including 200–240 MW shipment for PV systems) for 2014, down from the previous expectation of 3.6–3.8 GW ....

http://www.zacks.com/stock/news/155458/...than-expected-outlook-falls

Optionen

| Boardmail an "Melmacniac" |

Wertpapier: Yingli Green Energy |

Summary

Yingli Green Energy reported an impressive growth in its financials and customer base during the third quarter.

Yingli's addressable market is set to improve on the back of global solar growth and government policies.

Yingli has a global customer base that will allow it to tap growth in key markets such as the Asia Pacific and Africa.

Yingli is making its products better in order to gain more customers going forward.

.........

APAC and Africa are primary drivers

However, the growth projections are the highest in the APAC region, which is projected to add more generation (2,794GW) than the rest of the world combined (2,647GW), and the global power demand growth is the strongest in APAC and Africa .. s. Karte Moreover, the company is also investing in product development to stay technologically relevant. ......

http://seekingalpha.com/article/...lar-adoption-are-long-term-drivers

http://www.youtube.com/watch?v=-hpwx2ui4h8

Deutsche Aktionäre haben die Pflicht, so etwas nicht zu unterstützen, wie chinesische Solarunternehmen, die so etwas machen....

Optionen

| Boardmail an "Melmacniac" |

Wertpapier: Yingli Green Energy |

Buchtips

http://www.amazon.de/...7020907&sr=1-6&keywords=china+dumping

http://www.amazon.de/...020963&sr=1-17&keywords=china+dumping

Optionen

| Boardmail an "Melmacniac" |

Wertpapier: Yingli Green Energy |

2. Wer sagt dass die weiter steigen, vielleicht gibts bald die Quittung fürs Dumping, die hohen Schulden der Chinesenfirmen in der Solarbranche sind ja schon erdrückend, ich würde hier Gewinne mitnehmen , wenn ich mit denen verdient hätte, in letzter Zeit machte man mit den Chinesen nur Verluste...

Optionen

| Boardmail an "Melmacniac" |

Wertpapier: Yingli Green Energy |

Optionen

| Boardmail an "Melmacniac" |

Wertpapier: Yingli Green Energy |

Angehängte Grafik:

chack.png (verkleinert auf 70%)

chack.png (verkleinert auf 70%)

In terms of the agreement between Yingli and Solarcentury, the company will complete the delivery of approximately 168,000 solar PV panels by the end of this year. The panels will be installed in projects across the UK. These projects will produce approximately 65,000 MWh of solar power per year, enough to supply around 21,800 typical UK homes, Yingli Solar notes.....

Was fürher war, das war, aber jetzt kann man mit den Chinesen kein Geld mehr verdienen, sollte man sich eine bessere Aktie suchen

Optionen

| Boardmail an "Melmacniac" |

Wertpapier: Yingli Green Energy |

Optionen

| Boardmail an "weiar" |

Wertpapier: Yingli Green Energy |