Top oder Flop??? American Capit.LTD

Die letzten Tage geht es ja steil nach oben und wenn mann sich die Kurse vor einigen Monaten anschaut gibt es da ne menge Spielraum nach oben! Vieleicht auch nach unten?

Kauf oder nicht?

Vielen Dank für eure Meinung.......

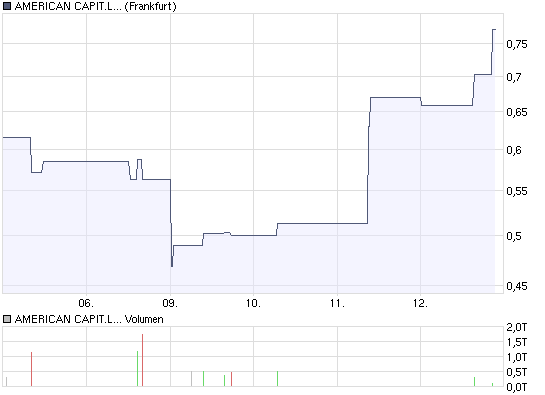

Angehängte Grafik:

chart_week_american_capit.png (verkleinert auf 93%)

chart_week_american_capit.png (verkleinert auf 93%)

Ami._Finanzmärkten leicht bergauf zu gehen,heut werden wir vieleicht leicht im minus schließen,aber ging die letzten 3 Tage 50 % nach oben.

So günstig wie heut wirds nicht mehr.Oder???????????????

Naja, aus Erfahrung lernt man. Halte jetzt meine Posi bis wir zweistellig sind...........

Zwischenzeitliche Kurskorrekturen nach unten werde ich nutzen um nachzukaufen.

Lg

Lucki

Der Zug rollt!!! bitte einsteigen..........

Lg

Optionen

| Boardmail an "Rico11" |

Wertpapier: American Capital |

The first-quarter net loss for the Bethesda, Maryland-based company, was $547 million, or $2.65 cents a share, compared with $813 million, or $4.16 cents a share in the year-ago period.

The company said income from ongoing operations was $64 million, or 31 cents a share.

Analysts expected the firm to earn 35 cents, excluding items, according to Reuters Estimates.

American Capital, which was removed from the S&P 500 market index in February, said the net unrealized depreciation on its its portfolio totalled $525 million in the first quarter, while realized losses amounted to $79 million.

American Capital also said it was in default on $2.3 billion of unsecured credit arrangements as of March 31, 2009, leading to higher interest rate payments.

The company said it has hired restructuring firm Miller Buckfire & Co to help negotiate with its lenders.

In late March, American Capital completed the buyout of minority shareholders in European Capital, paving the way for the possible sale of its European portfolio company.

The company said European Capital breached some of its debt covenants and the existing defaults could prevent it from realizing its net asset value, which tracks the worth of its investment portfolio.

It has been in talks with lenders since December about restructuring its credit facilities and is looking for buyers for its European portfolio in a deal that could be worth up to $2 billion.

American Capital plans to sell its European unit -- which had assets under management of $3.5 billion at the end of the third-quarter of 2008 -- in its entirety, or could split it up [ID:nLU402800]. (Reporting by Sweta Singh in Bangalore, and Phil Wahba in New York; Editing by Dhara Ranasinghe)

Mit dem Gewinn konnte ich heute die Anzahl der Aktien in meinem Depot deutlich erhöhen.

Lg

Carsten

Keefe Bruyette upgraded American Capital following the Q1 report and raised its target price.

www.thestreet.com

Glen Bradford

11-May-2009

Quarterly Report

Item 2. Management's Discussion and Analysis of Financial Condition and Results of Operations (in millions, except per share data)

Management's Discussion and Analysis of Financial Condition and Results of Operations (MD&A) is designed to provide a reader of American Capital's financial statements with a narrative from the perspective of management. Our MD&A is presented in four sections:

� Executive Overview

� Results of Operations

� Financial Condition, Liquidity and Capital Resources

� Forward-Looking Statements

EXECUTIVE OVERVIEW

We are a publicly traded private equity firm and a global asset manager. We primarily invest in senior debt, subordinated debt and equity in the buyouts of private companies sponsored by us ("American Capital One-Stop Buyouts�") and buyouts of private companies sponsored by other private equity firms ("American Capital One Stop Financings") and provide capital directly to early stage and mature private and small public companies. In addition, we also invest in structured product investments including CMBS, CLO and CDO securities ("Structured Products") and invest in alternative asset funds managed by us. We are also an alternative asset manager with $11 billion of capital resources under management as of March 31, 2009.

Our primary business objectives are to increase our taxable income, net realized earnings and net asset value ("NAV") by investing in private equity, private debt, private real estate investments, early, middle and late stage technology investments, special situations, credit opportunities, alternative asset funds managed by us and structured finance investments with attractive current yields and/or potential for equity appreciation and realized gains.

American Capital Investing Activities

We provide investment capital to middle market companies, which we generally consider to be companies with sales between $10 million and $750 million. We primarily invest in senior debt, mezzanine debt and equity in the buyouts of private companies sponsored by us, the buyouts of private companies sponsored by other private equity firms and provide capital directly to early stage and mature private and small public companies. Currently, we will invest up to $400 million in a single middle market transaction in North America. We also invest in Structured Products and alternative asset funds managed by us. For summary financial information of our investment portfolio by segment and geographic area, see Note 5 to the interim consolidated financial statements in Part I, Item I of this Quarterly Report on Form 10-Q.

We seek to be a long-term partner with our portfolio companies. As a long-term partner, we will invest capital in a portfolio company subsequent to our initial investment if we believe that it can achieve appropriate returns for our investment. Add-on financings fund (i) strategic acquisitions by a portfolio company of either a complete business or specific lines of a business that are related to the portfolio company's business, (ii) recapitalization of a portfolio company to raise financing on better terms, buyout one or several owners or to pay a dividend, (iii) growth of the portfolio company such as product development or plant expansions, or (iv) working capital for a portfolio company, sometimes in distressed situations, that needs capital to fund operating costs, debt service, or growth in receivables or inventory.

The total value of our investment portfolio was $6,849 million and $7,427 million as of March 31, 2009 and December 31, 2008, respectively. During the three months ended March 31, 2009 and 2008, we originated investments in 12 and 23 portfolio companies, respectively. Our new investment amounts represent the gross

committed capital on the origination date. The type and aggregate dollar amount of our new investments during the three months ended March 31, 2009 and 2008 were as follows (in millions):

Three Months Ended

March 31,

2009 2008

American Capital sponsored buyouts $- $303

Direct investments - 113

Investments in managed funds - 400

Structured products - 48

Add-on financing for growth and working capital - 13

Add-on financing for working capital in distressed situations 25 30

Add-on financing for recapitalizations 15 2

Total $40 $909

We received cash proceeds from realizations and repayments of portfolio investments as follows (in millions):

Three Months Ended

March 31,

2009 2008

Principal prepayments $ 42 $ 240

Loan syndications and sales 8 274

Scheduled principal amortization 10 17

Payment of accrued PIK interest and dividend and

original issue discounts 4 20

Sale of equity investments 15 380

Total $ 79 $ 931

Public Manager of Funds of Alternative Assets

We are a leading global alternative asset manager of third-party funds. In addition to managing American Capital's assets and providing management services to portfolio companies of American Capital, we also manage European Capital Limited ("European Capital"), American Capital Agency Corp. ("AGNC"), American Capital Equity I, LLC ("ACE I"), American Capital Equity II, LLC ("ACE II"), ACAS CLO 2007-1, Ltd. ("ACAS CLO-1") and American Capital CRE CDO 2007-1, Ltd. ("ACAS CRE CDO"). We refer to the asset management business throughout this report to include the asset management activities conducted by our wholly-owned portfolio company, American Capital, LLC.

As of March 31, 2009, our assets under management totaled $11 billion, including $4 billion under management in the third-party funds named above. As of March 31, 2009, our capital resources under management totaled $11 billion, including $4 billion under management in the third-party funds named above. Our third-party assets under management do not include the assets of European Capital since we own 100% of European Capital. As a result, only our investment in European Capital is included in our assets under management.

Through our asset management business, American Capital, LLC generally earns base management fees based on the size of the funds and incentive income based on the performance of the funds it manages. In addition, we may invest directly into our alternative asset funds and earn investment income from our direct investments in those funds. We intend to grow our existing funds, while continuing to create innovative products to meet the increasing demand of sophisticated investors for superior risk-adjusted investment returns.

The following table sets forth certain information with respect to our funds under management as of March 31, 2009:

ACAS ACAS

American Capital European Capital AGNC ACE I ACE II CLO-1 CRE CDO

Fund type Public Alternative Private Fund Public REIT Fund - Private Fund Private Fund Private Fund Private Fund

Asset The NASDAQ Global Market

Manager & Fund

Established 1986 2005 2008 2006 2007 2006 2007

Assets $7.2 Billion(1) $1.8 Billion(2) $2.4 Billion $0.6 Billion $0.3 Billion $0.4 Billion $0.1 Billion

Investment types Senior & Senior & Subordinated Agency Securities Equity Equity Senior Debt CMBS

Subordinated Debt, Equity,

Debt, Equity, Structured Products

Structured

Products

Capital type Permanent Permanent Permanent Finite Life Finite Life Finite Life Finite Life

(1) Includes our investment in third-party funds that we manage.

(2) Excluded from our third-party funds as we now own 100% of ECAS.

Summary of Critical Accounting Policies

The preparation of our financial condition and results of operations requires us to make judgments and estimates that may have a significant impact upon our financial results. We believe that of our significant accounting policies, the following require estimates and assumptions that require complex, subjective judgments by management, which can materially impact reported results: valuation of investments; interest and dividend income recognition; stock-based compensation; and derivative financial instruments. All of our critical accounting policies are fully described in "Management's Discussion and Analysis of Financial Condition and Results of Operations" in our Annual Report on Form 10-K for the year ended December 31, 2008. The following are critical accounting policies for valuation of Investments and interest and dividend income recognition.

Valuation of Investments

Our investments are carried at fair value in accordance with the 1940 Act and SFAS No. 157. In accordance with the 1940 Act, unrestricted minority-owned publicly traded securities for which market quotations are readily available are valued at the closing market quote on the valuation date and majority-owned publicly traded securities and other privately held securities are valued as determined in good faith by our Board of Directors. For securities of companies that are publicly traded for which we have a majority-owned interest, the value is based on the closing market quote on the valuation date plus a control premium if our Board of Directors determines in good faith that additional value above the closing market quote would be obtainable upon a sale or transfer of our controlling interest.

We adopted SFAS No. 157 on January 1, 2008. SFAS No. 157 provides a framework for measuring the fair value of assets and liabilities and also provides guidance regarding a fair value hierarchy, which prioritizes information used to measure fair value and the effect of fair value measurements on. SFAS No. 157 applies whenever other standards require (or permit) assets or liabilities to be measured at fair value but does not expand the use of fair value in any new circumstances.

In April 2009, the Financial Accounting Standards Board ("FASB") issued FASB Staff Position No. 157-4, Determining Fair Value When the Volume and Level of Activity for the Asset or Liability Have Significantly Decreased and Identifying Transactions That Are Not Orderly ("FSP No. 157-4"). FSP No. 157-4 made amendments to SFAS No. 157 to provide additional guidance for estimating fair value in accordance with SFAS No. 157 when the volume and level of activity for the asset or liability have significantly decreased and includes guidance on identifying circumstances that indicate a transaction is not orderly. It emphasizes that even if there has been a significant decrease in the volume and level of activity for the asset or liability and regardless of the valuation technique used, the objective of a fair value measurement remains the same that the fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction (that is, not a

forced liquidation or distressed sale) between market participants at the measurement date under current market conditions. The guidance in FSP No. 157-4 is effective for periods ending after June 15, 2009 and is applied prospectively with early adoption permitted for periods ending after March 15, 2009. We adopted FSP No. 157-4 during the quarter ended March 31, 2009. The adoption of FSP No. 157-4 did not have a material impact on our consolidated financial statements.

SFAS No. 157 defines fair value in terms of the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date under current market conditions. The price used to measure the fair value is not adjusted for transaction costs while the cost basis of our investments may include initial transaction costs. Under SFAS No. 157, the fair value measurement also assumes that the transaction to sell an asset occurs in the principal market for the asset or, in the absence of a principal market, the most advantageous market for the asset. The principal market is the market in which the reporting entity would sell or transfer the asset with the greatest volume and level of activity for the asset. In determining the principal market for an asset or liability under SFAS No. 157, it is assumed that the reporting entity has access to the market as of the measurement date. If no market for the asset exists or if the reporting entity does not have access to the principal market, the reporting entity should use a hypothetical market.

The market in which we would sell our private finance investments is the M&A market. Under SFAS No. 157, we have indentified the M&A market as our principal market for portfolio companies only if we have the ability to initiate a sale of the portfolio company as of the measurement date. We decide whether we have the ability to initiate a sale of a portfolio company based on our ability to control or gain control of the board of directors of the portfolio company as of the measurement date. In evaluating if we can control or gain control of a portfolio company as of the measurement date, we include our equity securities and those securities held by entities managed by American Capital, LLC, on a fully diluted basis. For investments in portfolio companies for which we do not have the ability to control or gain control as of the measurement date and for which there is no active market, our principal market under SFAS No. 157 is a hypothetical secondary market. The determination of the principal market used to estimate the fair value of each of our investments can have a material impact on our estimate of the fair value of our investments.

The levels of fair value inputs used to measure our investments are characterized in accordance with the fair value hierarchy established by SFAS No. 157. Where inputs for an asset or liability fall into more than one level in the fair value hierarchy, the investment is classified in its entirety based on the lowest level input that is significant to that investment's fair value measurement. We use judgment and consider factors specific to the investment in determining the significance of an input to a fair value measurement. The three levels of the fair value hierarchy and investments that fall into each of the levels are described below:

� Level 1: Level 1 inputs are unadjusted quoted prices in active markets that are accessible at the measurement date for identical, unrestricted assets or liabilities. We use Level 1 inputs for investments in publicly traded unrestricted securities for which we do not have a controlling interest. Such investments are valued at the closing price on the measurement date. We did not value any of our investments using Level 1 inputs as of March 31, 2009.

� Level 2: Level 2 inputs are inputs other than quoted prices included within Level 1 that are observable for the asset or liability, either directly or indirectly.

� Level 3: Level 3 inputs are unobservable and cannot be corroborated by observable market data. We use Level 3 inputs for measuring the fair value of substantially all of our investments as follows:

- For investments in securities of companies that are publicly traded for which we have a controlling interest, the fair value of the investment is based on the closing price of the security on the measurement date adjusted for the fair value of a control premium, if any, based on the value above the closing market quote that would be obtainable upon a sale of our controlling interest. A control premium incorporated into the valuation would be considered a Level 3 input if it has a significant impact on the determination of fair value.

- For investments in portfolio companies for which we have identified the M&A market as the principal market, we estimate the fair value based on the Enterprise Value Waterfall valuation methodology. Under the Enterprise Value Waterfall valuation methodology, we estimate the enterprise fair value of the portfolio company and then waterfall the enterprise value over the portfolio company's securities in order of their preference relative to one another. For minority equity securities, we also estimate the fair value using the Enterprise Value Waterfall valuation methodology. To estimate the enterprise value of the portfolio company, we prepare an analysis consisting of traditional valuation methodologies including market, income and cost approaches. We weight some or all of the traditional valuation methods based on the individual circumstances of the portfolio company in order to conclude on our estimate of the enterprise value. The methodologies consist of valuation estimates based on: valuations of comparable public companies, recent sales of private and public comparable companies, discounting the forecasted cash flows of the portfolio company, estimating the liquidation or collateral value of the portfolio company's assets, third-party valuations of the portfolio company, considering offers from third-parties to buy the company, estimating the value to potential strategic buyers and considering the value of recent investments in the equity securities of the portfolio company. To determine the enterprise value of a portfolio company, we analyze its historical and projected financial results. This financial and other information is generally obtained from our portfolio companies, and may represent unaudited, projected or pro-forma financial information. The assumptions incorporated in the valuation methodologies used to estimate the enterprise value consists primarily of unobservable Level 3 inputs, including management assumptions based on judgment. A change in these assumptions could have a material impact on the determination of fair value.

- For investments in portfolio companies for which we have identified the hypothetical secondary market as the principal market, we determine the fair value based on the assumptions that a hypothetical market participant would use to value the investment in a current hypothetical sale using a Market Yield valuation methodology. In applying the Market Yield valuation methodology, we estimate the fair value based on such factors as third-party broker quotes and market participant assumptions including synthetic credit ratings, estimated remaining life, current market yield and interest rate spreads of similar securities as of the measurement date. The assumptions used to estimate the fair value in a hypothetical secondary market are considered primarily Level 3 inputs. We weight third-party broker quotes in determining fair value based on our understanding of the level of actual transactions used by the broker to develop the quote and whether the quote was an indicative price or binding offer. In estimating the remaining life, we generally use an average life based on market data of the average life of similar loans. However, if we have information available to us that the loan is expected to be repaid in the near term, we would use an estimated life based on the expected repayment date. The average life used to estimate the fair value of our loans is generally shorter than the legal maturity of the loans as our loans have historically been prepaid prior to the maturity date. The current interest rate spreads used to estimate the fair value of our loans is based on our experience of current interest rate spreads on similar loans. A change in the unobservable inputs and assumptions that we use to estimate the fair value of our loans could have a material impact on the determination of fair value.

- We value our investments in Structured Products using the Market Yield valuation methodology. We estimate the fair value based on such factors as third-party broker quotes and our cash flow forecasts subject to our assumptions a market participant would use regarding the investments' underlying collateral including, but not limited to, assumptions of default and recovery rates, reinvestment spreads and prepayment rates. Cash flow forecasts are discounted using a market participant's market yield assumptions which are derived from multiple sources including, but not limited to, third-party broker quotes, recent investments and securities with similar structure and risk characteristics. We weight the use of third-party broker quotes in determining fair value based on our understanding of the level of actual transactions used by the broker to develop the quote

and whether the quote was an indicative price or binding offer. The cash flow forecasts and market yields used to discount the cash flows incorporate a significant amount of Level 3 inputs. A change in our default and recovery rate assumptions in the cash flow forecasts or a change in the market yield assumptions could have a material impact on the determination of fair value.

- We value derivative instruments based on fair value information from both the derivative counterparty, as adjusted for nonperformance risk considerations, and third-party pricing services. We corroborate the fair value by analyzing the estimated net present value of the future cash flows using relevant market forward interest rate yield curves in effect at the end of the period as adjusted for quantitative and qualitative nonperformance risk considerations. A change in our determination of the nonperformance risk could have a material impact on the determination of fair value.

Due to the uncertainty inherent in the valuation process, such estimates of fair value may differ significantly from the values that would have been used had a ready market for the investments existed, and the differences could be material. Additionally, changes in the market environment and other events that may occur over the life of the investments may cause the gains or losses ultimately realized on these investments to be different than the valuations currently assigned.

See Note 5 to our consolidated financial statements in this Quarterly Report on Form 10-Q for further information regarding the classification of our investment portfolio by Levels 1, 2 and 3 as of March 31, 2009.

Interest and Dividend Income Recognition

Interest income is recorded on the accrual basis to the extent that such amounts are expected to be collected. Original issue discount ("OID") is accreted into interest income using the effective interest method. OID initially represents the value of detachable equity warrants obtained in conjunction with the origination or purchase of loans and loan origination fees that represent yield enhancement. Dividend income is recognized on the ex-dividend date for common equity securities and on an accrual basis for preferred equity securities to the extent that such amounts are expected to be collected or realized. In determining the amount of dividend income to recognize, if any, from cash distributions on common equity securities, we will assess many factors including a portfolio company's cumulative undistributed income and operating cash flow. Cash distributions from common equity securities received in excess of such undistributed amounts are recorded first as a reduction of our investment and then as a realized gain on investment. We stop accruing interest or dividends on our investments when it is determined that the interest or dividend is not collectible. We assess the collectability of the interest and dividends based on many factors including the portfolio company's ability to service our loan based on current and projected cash flows as well as the current valuation of the enterprise. For investments with payment-in-kind ("PIK") interest and cumulative dividends, we base income and dividend accruals on the valuation of the PIK notes or securities received from the borrower or the redemption value of the security. If the portfolio company valuation indicates a value of the PIK notes or securities or redemption value that is not sufficient to cover the contractual interest or dividend, we will not accrue interest or dividend income on the notes or securities.

A change in the portfolio company valuation assigned by us could have an effect on the amount of loans on non-accrual status. Also, a change in a portfolio company's operating performance and cash flows can impact a portfolio company's ability to service our debt and therefore could impact our interest recognition.

Interest income on CMBS, CLO and CDO investments is recognized on the effective interest method as required by Emerging Issues Task Force ("EITF") Issue No. 99-20, Recognition of Interest Income and Impairment on Purchased and Retained Beneficial Interests in Securitized Financial Assets ("EITF No. 99-20"). Under EITF No. 99-20, at the time of purchase, we estimate the future expected cash flows and determine the effective interest rate based on these estimated cash flows and our cost basis. Subsequent to the purchase and on

a quarterly basis, these estimated cash flows are updated and a revised yield is calculated prospectively based on the current amortized cost of the investment. To the extent the current quarterly estimated cash flows decrease from the prior quarterly estimated cash flows, the revised yield is calculated prospectively based on the amortized cost basis of the investment calculated in accordance with Financial Accounting Standards Board (the "FASB") Staff Position No. FAS 115-2 and 124-2, Recognition and Presentation of Other-Than-Temporary Impairment, ("FSP FAS 115-2"). In estimating these cash flows, there are a number of assumptions that are subject to uncertainties and contingencies. These include the amount and timing of principal payments (including prepayments, repurchases, defaults and liquidations), the pass through or coupon rate, and interest rate fluctuations. In addition, interest payment shortfalls due to delinquencies on the underlying loans, and the timing of and magnitude of projected credit losses on the loans underlying the securities have to be estimated. These uncertainties and contingencies are difficult to predict and are subject to future events that may impact our estimates and interest income. As a result, actual results may differ significantly from these estimates.

RESULTS OF OPERATIONS

Hallo da ich hier auch investiert bin habe ich eine Frage !

Kann diese Aktie auch wertlos wie ein Optionsschein

verfallen.

Also wenn wir bei 0 angekommen sind nie mehr steigen ?

- Ein Unternehmen ist pleite – und trotzdem ist die Aktie noch was wert. Warum ist das so?

Weil die Hoffnung eben siegt. An dem Beispiel von Qimonda ist es recht gut zu sehen. Die Aktie fiel bis auf 7 Cent und konnte sich dann wieder bis auf etwa 9 Cent erholen. Nicht nur die Aktionäre hoffen auf die kleine Chance, dass es trotz des Antrags auf Insolvenz weitergeht. So will auch Qimonda-Chef Kin Wah Loh an eine Rettung in letzter Sekunde glauben.

Solange das operative Geschäft noch lebt, werden die Aktionäre denn wohl auch weiter hoffen. Vielleicht hofft man auch noch auf verwertbare Vermögensteile. Doch die Aktie ist, wie auch in den letzten Monaten schon, zum Spekulationspapier verkommen, das vorwiegend Zocker anlockt, und heftige Kursbewegungen verbucht.

Manchmal treibt auch eine Mantel-Spekulation

Was geschieht aber, wenn das operative Geschäft (zum Beispiel nach einer Pleite) irgendwann komplett beendet ist. Sinkt der Kurs dann auf Null? Nicht immer. Bei vielen Aktien steckt dennoch Leben drin.

Die Gesellschaften bestehen zwar im Grunde nur noch aus ihrer rechtlichen Hülle, dem so genannten Mantel. Doch solche "Börsenzombies" können durchaus noch zu von Nutzen sein. Sie haben nämlich etwas, was anderen Unternehmen fehlt: Die Rechtsform einer Aktiengesellschaft und die Börsennotierung. Damit sind sie für Unternehmen interessant, die kostengünstig an die Börse gehen möchten. Sie können mit weniger bürokratischem Aufwand in einen bereits bestehenden Börsenmantel schlüpfen. Wenn die Börse etwas derartiges wittert, bekommt die Aktie schon mal Auftrieb: Man nennt das Mantel-Spekulation.

Traders were focused on the June 5 options, where more than 9,000 calls changed hands Friday for $0.15 and $0.20, according to optionMONSTER's Heat Seeker monitoring system. The turnover dwarfed the average daily volume of just 409 calls at that strike and was more than double the open interest of under 4,000 contracts.

* More Options Tips from Pete Najarian

* Options Tips from Jon Najarian

* Read The CNBC Stock Blog

American Capital [ Loading... () ] closed Friday down 6.5 percent in the regular session and dropped another 1.3 percent in after-hours trading to an even $3. The shares have been making their way back up after being beaten down to under $1 in March but are still only a fraction of their 52-week high of $33.56.

The options activity suggests that traders are hoping that the stock will reach $5 by the end of the third Friday in June, when that month's contracts expire. The investment firm, which specializes in private equity acquisitions, was upgraded on May 7 to "market perform" by Keefe Bruyette after the company reported quarterly earnings that missed analysts' estimates.

BETHESDA, Md., June 11 /PRNewswire-FirstCall/ -- American Capital Ltd. (Nasdaq: ACAS - News; the "Company") announced today that its Board of Directors has declared a dividend of $1.07 per share payable on August 7, 2009, to stockholders of record as of the close of business on June 22, 2009, with an ex-dividend date of June 18, 2009. At the election of each stockholder, the dividend is payable either in cash or in shares of common stock, or due to certain limitations described below, in a combination of cash and common stock.

If the aggregate amount of the cash elections exceeds 10% of the aggregate dividend amount, the cash portion will be prorated among the stockholders electing to receive cash. The remaining portion of the dividend will be paid in shares of common stock ("Stock Portion"). The number of shares of common stock comprising the Stock Portion will be determined based on the volume weighted average price of American Capital's stock on the NASDAQ Global Select Market on July 27, July 28 and July 29, 2009. The exact distribution of cash and stock to each stockholder will depend on the stockholder's election as well as elections of other stockholders. For example, if all stockholders elected to receive the dividend in cash, the actual dividend that would be paid to stockholders would consist of a 90% Stock Portion and a 10% cash distribution.

This dividend includes the Company's remaining 2008 taxable income, which is required to be distributed to stockholders in order for the Company to maintain its tax status as a regulated investment company and to eliminate its income tax liability. The IRS issued a Revenue Procedure allowing a publicly traded regulated investment company to distribute, with respect to a taxable year ending on or before December 31, 2009, its own stock as a dividend for the purpose of fulfilling its distribution requirements if, among other things, the aggregate amount of cash that may be distributed to its stockholders is at least 10% of the total dividend. The Investment Company Act of 1940 could prohibit American Capital from paying any cash dividend when its asset to debt coverage as determined under the Act is less than 200% and it has public bonds outstanding. However, the staff of the Securities and Exchange Commission has provided the Company with no-action relief to the effect that American Capital may declare and pay a cash dividend in these circumstances, provided that the cash portion does not exceed the 10% cash minimum required by the IRS Revenue Procedure.

The Company will mail a letter with additional information regarding the distribution election and an election form only to registered stockholders promptly after June 22, 2009. (Registered stockholders are those stockholders who own their stock directly and not through a bank, broker or nominee.) The completed election form to receive cash or common stock must be received by American Capital's transfer agent, Computershare Trust Company, N.A., prior to 5:00 p.m. (EDT) on July 24, 2009. Registered stockholders with questions regarding the dividend may call our transfer agent, Computershare Trust Company, N.A. at (800) 733-5001. Registered stockholders who do not make an election will be deemed to have elected to receive their dividend in stock.

Stockholders who hold their shares through a bank, broker or nominee will not receive an election form from the Company. Rather, they should contact their bank, broker or nominee for instructions on how to make an election or if they otherwise have questions regarding the dividend.

American Capital reports the anticipated tax characteristics of each dividend when announced, while the actual tax characteristics of each year's dividends are reported annually to stockholders on Form 1099DIV. The dividend will be fully taxable to stockholders. The Company anticipates the 2009 declared dividends to date of $1.07 per share to be a distribution of ordinary taxable income.

For further information or questions, please call our Investor Relations Department at (301) 951-5917 or send an email to IR@AmericanCapital.com.