RENESOLA startet

Das ist doch echt schon alles sowas von gesteuert. Haben die keine Ukraine finden die was anderes und morgen werden dann die Nutten billiger, na schönen Dank auch

Mal schaun, ob die 2 USD heute halten werden. Darunter könnte man wieder ein paar Stücke kaufen.

On the Q2 conference call, management guided Q3 total module shipments of between 530 MW and 550 MW and Q3 gross margin of 15% to 17%.

...

...

...

A key metric to watch will be ReneSola's manufacturing cost per watt, as falling manufacturing costs will make ReneSola more competitive and turn a currently breakeven company into a profitable one in the future. In Q2, the company's OEM cost per watt was $0.63, while its internal cost per watt was $0.51-$052.

Given that the company's strategy is to basically expand OEM capacity going forward, a falling OEM production cost per watt is essential to ReneSola's future bottom line.

Given the strong Q3 for ReneSola's peers, I believe ReneSola will likely beat both revenue and profit expectations on November 26th.

http://seekingalpha.com/article/2696575-renesola-earnings-preview

Von meinem durchschnittlichen Einkaufskurs bin ich grausam weit weg, aber nicht mehr lange ;-)

http://stocktwits.com/symbol/SOL?q=SOL

Die shortquote ist nicht auffällig groß. Das Problem von SOL ist eher die nicht vorhandene Aufmerksamkeit, verglichen mit den anderen Chinasolaris. Sieht man auch an den Börsenumsätzen. Da gibt es keinen Yieldco Phantasie oder dergleichen. Durch die angespannte Finanzlage sind Sol die Hände gebunden. Auch Produktionserweiterungen scheitern angesichts der Kassenlage. Lediglich OEM Erweiterungen sind möglich, aber die bringen keine großen Margen. KE`s sind angesichts des Minikurses auch keine Alternative.

Selbst von einer Aufhebung der US-Zölle dürfte Sol kaum profitieren.

Und so kommt es, dass ein Unternehmen mit über $ 1,8 Milliarden Jahresumsatz mit lächerlichen $ 215 Mio. bewertet wird.

Es wird heute spannend, wie Sol sich im Markt schlägt und welche Perspektiven man bei SOl sieht.

Ich denke das Beste wäre für Sol, sich einen großen (finanzstarken)Partner zu suchen.

Optionen

| Boardmail an "Obelisk" |

Wertpapier: ReneSola Ltd ADR |

http://ir.renesola.com/...amp;p=irol-EventDetails&EventId=5174781

VG und viel Glück

Taktueriker

JIASHAN, China, Nov. 26, 2014 /PRNewswire/ -- ReneSola Ltd ("ReneSola" or the "Company") (www.renesola.com) (NYSE: SOL), a leading brand and technology provider of solar photovoltaic ("PV") products, today announced its unaudited financial results for the third quarter ended September 30, 2014.

ReneSola Logo

Financial and Operational Highlights for Q3 2014

•Total solar module shipments were 462.2 megawatts ("MW"), compared to 498.7 MW in Q2 2014 and 462.9 MW in Q3 2013. Total solar wafer and module shipments were 663.8 MW, compared to 698.3 MW in Q2 2014 and 851.0 MW in Q3 2013.

•Net revenues were US$372.5 million, compared to US$387.1 million in Q2 2014 and US$419.3 million in Q3 2013.

•Gross profit was US$57.1 million with a gross margin of 15.3%, compared to a gross profit of US$56.9 million with a gross margin of 14.7% in Q2 2014 and gross profit of US$36.7 million with a gross margin of 8.7% in Q3 2013.

•Operating income was US$8.5 million with an operating margin of 2.3%, compared to an operating income of US$10.6 million with an operating margin of 2.7% in Q2 2014 and an operating loss of US$180.3 million with an operating margin of negative 43.0% in Q3 2013.

•Net loss attributable to holders of ordinary shares was US$11.7 million, representing basic and diluted loss per common share of US$0.06 and basic and diluted loss per American depositary share ("ADS"), each representing two common shares, of US$0.12.

•Cash and cash equivalents plus restricted cash totaled US$196.7 million as of the end of Q3 2014, compared to US$218.8 million as of the end of Q2 2014 and US$438.5 million as of the end of Q3 2013.

•Net cash outflow from operating activities was US$10.7 million, compared to net cash outflow from operating activities of US$40.6 million in Q2 2014 and net cash inflow from operating activities of US$79.6 million in Q3 2013.

http://ir.renesola.com/...10622&p=irol-newsArticle&ID=1993153

Optionen

| Boardmail an "Goethe21" |

Wertpapier: ReneSola Ltd ADR |

Optionen

| Boardmail an "Goethe21" |

Wertpapier: ReneSola Ltd ADR |

Sieht hier auch jemand was positives oder schnell raus hier?

Maydorn ist und bleibt größtenteils ein Kontraindikator zum Zeitpunkt seiner Empfehlungen.

Ärgerlich für die welche dadurch zum Kauf animiert wurden.

VG

Taktueriker

Bei 1 Cent steige ich dann auch aus :)

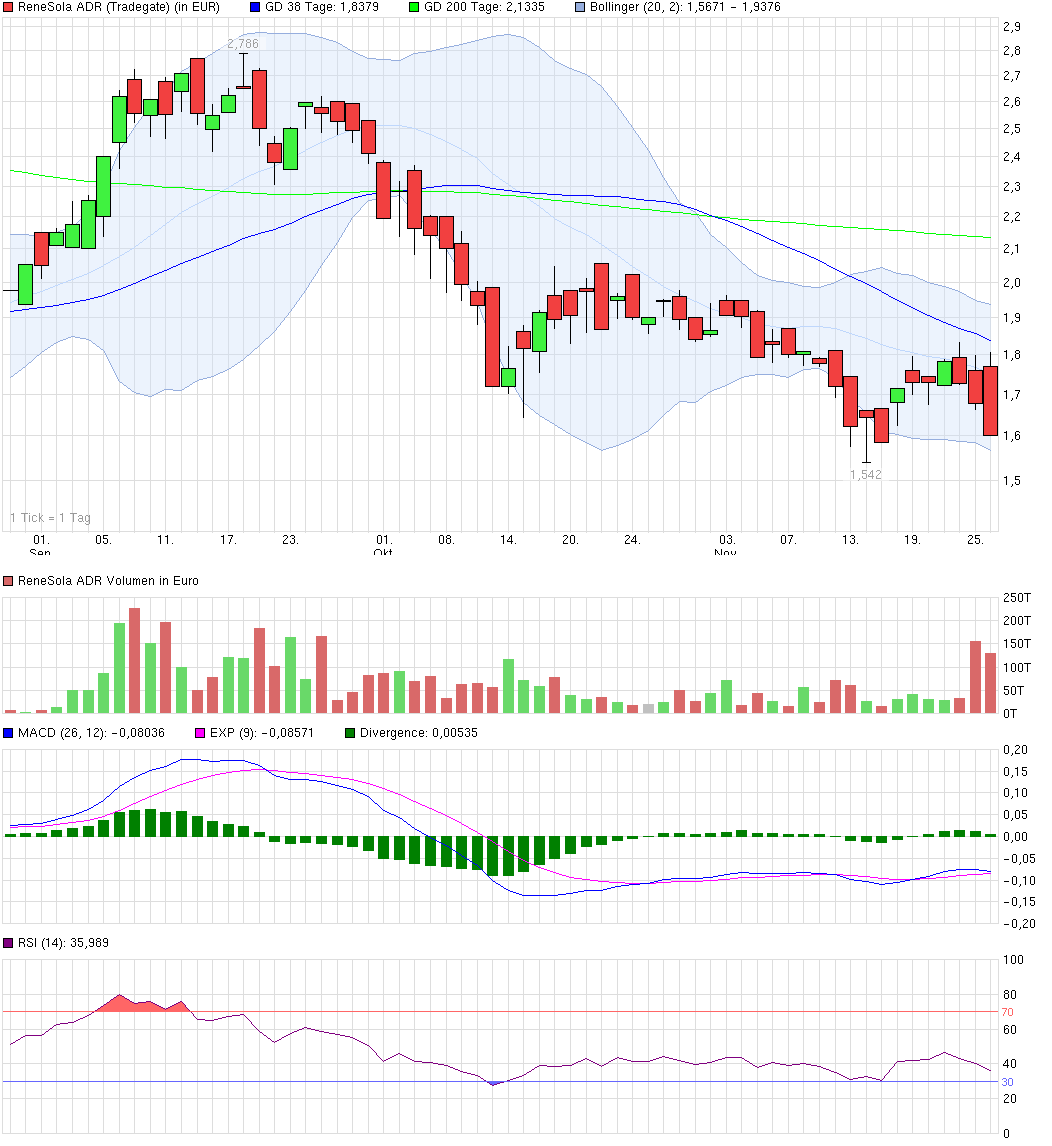

Angehängte Grafik:

chart_quarter_renesolaadr.png (verkleinert auf 48%)

chart_quarter_renesolaadr.png (verkleinert auf 48%)

Optionen

| Boardmail an "Goethe21" |

Wertpapier: ReneSola Ltd ADR |