Lpath inc. (LPTN.OB)

Seite 1 von 2 Neuester Beitrag: 25.04.21 00:04 | ||||

| Eröffnet am: | 15.01.12 22:58 | von: Chalifmann3 | Anzahl Beiträge: | 44 |

| Neuester Beitrag: | 25.04.21 00:04 | von: Klaudiabrcca | Leser gesamt: | 12.431 |

| Forum: | Hot-Stocks | Leser heute: | 2 | |

| Bewertet mit: | ||||

| Seite: < 1 | 2 > | ||||

Lpath, Inc. and its Immune Y2 technology captured the biotech world’s attention in December 2010 after it announced a partnership with Pfizer (PFE) to develop and potentially market Lpath’s wet AMD drug, iSONEP. Per the agreement, Pfizer provided Lpath with $14 million upfront and Lpath would be eligible to receive development, regulatory and commercial milestone payments that could potentially add up to about $500 million not including the double-digit royalties from the sales of the drug if approved. Lpath announced the receipt of the $14 million in January 2011, setting the tone for the year for this small cap biotech and giving it broader exposure by putting it on many biotech investor watch lists. This agreement at least partially legitimizes Lpath’s Y2 technology and the iSONEP drug specifically as the Big Pharma leader recognizes the drug’s potential. The agreement also gives Pfizer the first right of refusal to Lpath’s cancer drug, ASONEP, which utilizes the same bioactive lipid signaling approach as iSONEP. Biotech traders view the agreement as being a huge positive as Pfizer wouldn’t be investing such a large amount of money or time in such an endeavor without having a great deal of confidence in the technology.

Information on their “top of the class” deserving Immune Y2 technology can be found on the company’s website. Basically, iSONEP itself is a monoclonal antibody targeting Sphingosine 1 Phosphate (S1P). S1P is a bioactive lipid that is a key component of the sphingolipid signaling cascade. In the wet AMD, S1P has been implicated as having many actions that promote inflammation and dysregulated angiogenesis. It additionally supports the survival of multiple cell types including fibroblasts, endothelial and inflammatory cells that participate in the dysfunctional processes of wet AMD and other eye diseases. If this pathway is tied up or neutralized, the angiogenesis, leakiness, scarring and inflammation due to AMD should be effectively eliminated because a larger portion of related factors involved will be targeted, not just those pertaining to the VEGF pathway that EYLEA, Avastin and Lucentis target due to the fact that S1P is linked to the production and activation of the growth factors VEGF, FGF, PDGF MCP-1 IL-6, IL-8 often implicated in the pathogenesis of wet AMD.

Phase 2 trials for iSONEP are already underway. They’re supported by strong phase I data in which the drug was well tolerated in all 15 patients with positive biological effects seen in most patients. The patient set chosen was a difficult one in which several of the patients had failed to respond positively to either Avastin or Lucentis. The drug appeared to stop the abnormal blood vessel growth, reduced the retinal thickness and also controlled the leakiness of the existing vessels, which are trademark effects of the ailment. However, as an added bonus the drug did something that neither Lucentis nor Avastin have shown clinical abilities to do. It mitigated the scarred tissue and inflammation, two key areas that could actually improve vision rather than only stopping its regression. If phase 2 data show comparable results to the phase I data particularly in the areas of vision improvement (2nd phase 2 trial) and in the case of RPE detachment phase 2 trial an improvement is seen in retinal pigment epithelium detachment secondary to wet AMD or polypoidal choroidal vasculopathy (PCV), the company will start generating phenomenal interest by potentially answering a large unmet need in a near-blockbuster market. Pfizer and many biotech investors are already watching the company closely and have already positioned themselves for success in the company. Interim and perhaps even final data obtained in 2012 will be huge catalysts for the company and could justify those decisions.

MFG

Chali

Optionen

| Boardmail an "Chalifmann3" |

Wertpapier: Apollo Endosurgery |

Angehängte Grafik:

smilie_denk_09.gif

smilie_denk_09.gif

Lpath's flagship product, iSONEP, is a new potential wet AMD treatment that targets Sphingosine 1 Phosphate, which I found to be a radically different approach relative to the standard blood vessel growth (angiogenic) inhibitors. Laser surgery is also an option for wet AMD patients, but it carries inherent risks that make it less and less popular with time.

Assuming that iSONEP stops blood vessel growth just as well as the competing AMD drugs, it looks like a winner when you factor in its potential to fix detachment of the retinal pigment epithelium (RPE) in wet AMD patients. RPE detachment is a related symptom of wet AMD, and has a variety of unpleasant symptoms that interfere with vision (such as blurry vision, micropsia, and scotomas).

iSONEP has become especially important for Lpath's future due to the partnership program with Pfizer (PFE) that started in 2010, which actually gave Pfizer total worldwide marketing rights to the drug. Although it already sold away most of the market potential of its biggest project, Lpath has every incentive to continue. The company can still get half a billion in cash from milestone payments, and will receive double-digit royalties on iSONEP sales. This explains why investors were so dismayed in late January, when the FDA suspended both the PEDigree trial (in phase I) and Nexus trial (in phase II).

Lpath took longer than expected to get the FDA to remove its clinical hold, but LPTN finally got relieved on August 27th - and saw a subsequent 12% drop in share price. Quite a strange reaction to the good news. On October 3rd, Lpath announced that it had initiated dosing in the Nexus trial back in September, and saw some amazing results in some of the patients. Again, the market showed very little enthusiasm.

Those who follow biotech science closely know that bioactive lipids are seen as the next generation of drug development

Acting as tiny messengers, bioactive lipids play important roles in cellular function (e.g. cell division, cell death, cell migration) and their dysregulation can therefore contribute to disease. Bioactive lipids, for example, can:

One can treat disease by neutralizing certain lipids (the ones that become dysregulated and thereby contribute to disease). The only known method to neutralize a bioactive lipid is to generate an antibody that binds to it

Antibodies are designed to bind to "foreign" things in the body; these things are typically fairly large, however, lipids are neither foreign nor large. In fact, they are quite tiny.

As such, everyone that tried to generate this type of antibody failed until Lpath unlocked the code (patent protected).

Those focused on fundamentals may have shrugged off Lpath's renewed progress, but smart money is betting on the future of this firm. One can see that reflected in the number of institutional investors who own stock and believe in the science here. Another strong validation of their technology comes from the Pfizer partnership seeking the commercialization of their ocular drug, iSONEP™-- a deal valued at more than $500M.

We wouldn't ignore strong phase II results and might consider placing bets now since prices may not stay at these levels for long

MFG

Chali

Optionen

| Boardmail an "Chalifmann3" |

Wertpapier: Apollo Endosurgery |

To date, Lpath is the only company to have developed functional therapeutic monoclonal antibodies against lipids. This is made possible by their proprietary ImmuneY2TM platform developed by its founder, Roger Sabbadini, Ph.D. With this technology, Lpath is capable of expanding the company's pipeline of monoclonal antibody candidates to target other bioactive lipids in disease. Moreover, Lpath is in partnership with Pfizer (PFE) for its lead antibody, iSONEP and the first right of refusal agreement for ASONEP, which are both in Phase II trials for wet age-related macular degeneration (AMD) and renal cell carcinoma (RCC), respectively.

Wet AMD

Age-related macular degeneration is a leading cause of adult blindness in industrialized countries. It is a chronic condition affecting the macula, a spot near the center of the retina specialized for high visual acuity. There are two basic types of AMD: dry and wet. Dry AMD is by far the more common (90%) and progresses gradually, whereas wet AMD can cause rapid vision loss and accounts for 90% of severe vision loss caused by macular degeneration. In wet AMD, blood vessels grow abnormally under the retina in a process known as choroidal neovascularization (CNV). Blood or fluid may leak from these newly grown blood vessels, and lift the macula up from its normal position, thus distorting or destroying central vision.

AMD affects a significant number of people aged 40 years and above. US National Eye Institute's Prevalence of Blindness Data show that ~ 1.7 million people (1.5% of the age group) have advanced AMD, amongst which about 1.1 million have wet AMD (Selvaraju and Chen, Aegis Capital Corp, 2012). This number is projected to increase to 2.9 million by 2020 (National Eye Institute). Similarly, Owen et al. found that in the UK population aged above 50 years, 2.4% (~ 500,000 patients) have late stage AMD, about half of which (~250,000 patients) have CNV.

Currently there is no cure for AMD. For wet AMD, there are currently two main treatment options: laser treatment and VEGF inhibitors. The first laser treatment, laser photocoagulation, is limited in effectiveness and may cause macular scarring and additional vision loss (macular.org). The newer Photodynamic Laser Therapy uses the light-activated drug Visudyne to selectively destroy CNV upon laser irradiation. However, its use is limited to a subtype of wet AMD, or a quarter of the patient population. Furthermore, it is mostly palliative, does not restore lost vision, and CNV may recur and require repeated treatments.

The other type of treatments originates from the discovery made in cancer research that the protein Vascular Endothelial Growth Factor (VEGF) promotes the growth of blood vessels. Inhibiting VEGF thus may prevent and disrupt CNV. Presently four VEGF inhibitors are in use: Macugen, Avastin, Lucentis, and Eylea. Macugen is a small molecule (single strand aptamer) and was first approved in 2004. However, it loses market share to Lucentis ($1.6B of US sales in 2012) and Avastin due to the superior effectiveness of the latter. It is noteworthy that Avastin is not officially approved by the FDA to treat wet AMD, so is used off-label. Nevertheless, it was shown to be as effective as Lucentis, but is significantly cheaper (see Table 1). Therefore it became strongly preferred by US retinal specialists (63% patient share vs. 23% for Lucentis). This contrasts with the situation in EU5 (France, Germany, Italy, Spain, and UK), where 66% of patients were treated with Lucentis, compared to 27% with Avastin. Eylea, approved in 2011, is a synthetic fusion protein, and has a bi-monthly regimen compared to the monthly injections required by Lucentis (although in practice the average patient receives Lucentis bimonthly, see notes to Table 1). This may underlie the success of Eylea, which sold $837.9 million in the US in 2012.

iSONEP

The product iSONEP developed by Lpath takes a different approach. It is a monoclonal antibody against a lipid, sphingosine-1-phosphate (S1P). S1P is linked to several molecular pathways in addition to VEGF, and is implicated in inflammation, pathogenic fibrosis, and abnormal angiogenesis. Therefore anti-S1P treatment may address wet AMD-related vision loss by targeting pathologic disruption and remodeling of the retinal and sub-retinal architecture caused collectively by CNV, sub-retinal fibrosis, edema, and inflammation. This approach may either confer advantages over approaches that exclusively target VEGF, or act synergistically with anti-VEGF treatments. Indeed, Phase I trial of iSONEP demonstrated very encouraging outcome in patients who had failed to respond to Lucentis/Avastin; even a single dose of iSONEP may significantly reduce the CNV lesion size, which is typically unobserved with VEGF inhibitors. Notably, in two patients with retinal pigment epithelial detachment (PED, prevalent in 15-20% of wet AMD cases), a single dose of iSONEP led to near-complete resolution of the condition. While this was a small sample size, now iSONEP is undergoing Phase II trials in which its efficacy and safety with and without Lucentis/Avastin will be tested.

Potential Outcomes of iSONEP Approval

If the FDA eventually approves iSONEP, we can envision three scenarios. First, it may replace anti-VEGF drugs as the first-line treatment of wet AMD. Second, it may be used in conjunction with anti-VEGF drugs. Third, it may be used as a second-line treatment for patients who fail to respond to anti-VEGF drugs. In order to project the market size of iSONEP, we first estimate the current market size of its competitors. The current US sales volume of Lucentis suggests that about 800,000 doses were prescribed in 2012, which translates into ~130,000 patients (assuming six doses per year on average). The US preference for Avastin (see above) suggests that approximately 356,000 patients were treated in the same year. Eylea's sales volume translates into approximately 75,500 patients in 2012 (assuming bi-monthly injection). The total number of patients treated with these anti-VEGF drugs is thus about 561,000 in 2012. We assume a proportionate growth of the number of patients treated with anti-VEGF drugs with the total patient population.

The iSONEP is expected to launch in 2017. We project that in 2025 its market share will peak at 10% of the market currently captured by anti-VEGF drugs, and at 20% of the market currently not captured. We assume its cost to be $2,000 per dose, or $12,000 per year. Historical data suggest that a drug entering Phase II clinical trial has about 16% probability of eventual FDA approval. Taking all these into consideration and using a 20% discount rate, we project that iSONEP can contribute about 148.3 million USD to the NPV of the company, or $14.4 per share outstanding.

Treatment

Mechanism

Approval

Effectiveness

Cost / dose ($)

Annual Cost ($)

Visudyne

Photoactivated small molecule

60% stabilized;

3% vision improved

~ 2000

Macugen

(pegaptanib sodium)

Small molecule binding to VEGF

2004

65% stabilized;

6% vision improved (with early diagnosis)

800

Lucentis (ranibizumab)

Monoclonal antibody fragment against VEGF

2006

95% stabilized;

40% vision improved

2000

23,4001 or 12,8002

Avastin (bevacizumab)

Monoclonal antibody against VEGF

Off-label

Equivalent to Lucentis6

50

5953 or 3854

Eylea (aflibercept)

Synthetic fusion protein binding to VEGF

2011

Comparable to Lucentis7

1850

11,1005

Table I. Currently available treatments for wet AMD

1,3: monthly injection; 2,4: injection as needed (on average 5 - 7 doses per year); 5: bimonthly

Renal Cell Carcinoma

Renal cell carcinoma is one of the ten most common cancers in both men and women and is the most common type of kidney cancer in adults. More men develop renal cell carcinoma than women. In the United States in 2013, there are about 65,150 new cases of renal cell cancer and 13,680 deaths. Since the late 1990s, the rate of people developing renal cell cancer has increased. One reason for this is likely the development of newer, more sensitive imaging tests.

Renal cell carcinoma can often be cured if diagnosed early and treated while the cancer is still localized to the kidney and surrounding tissue with surgery. When the cancer has spread beyond the kidney, there are five main types of standard treatment: surgery to remove the cancer, radiation therapy, chemotherapy, biologic therapy, and targeted therapy including monoclonal antibody therapy. Adjuvant therapies, which include a combination of the five standard treatments, are also used.

Currently, the FDA has approved 14 drugs for renal cell cancer treatment. Of these 14 drugs, three (Avastin, Sutent, Sorafenib) block angiogenesis. Recently, Axitinib (Inlyata) was approved for renal cell cancer treatment in 2012 for patients with advanced renal cell cancer and have had one prior systemic treatment. Patients treated with Axitinib had a progression free survival of 6.7 months, while patients treated with sorafenib, the standard treatment, had a progression free survival of 4.7 months. Axitinib is an oral pill that inhibits tyrosine kinases. Side effects, which are seen in about 20% of the patients, include weight loss, nausea, hypertension, vomiting, and constipation.

Treatment

Mechanism

Approval

Effectiveness

Avastin (bevacizumab)

Injections of monoclonal antibody against VEGF.

2009

Drug combination can increase progression-free survival time by 5.7 months.

Axitinib (Inlyata)

Oral pill. Small molecule tyrosine kinase inhibitor.

2012

Second in line treatment. Progression-free survival time extended by 6.7 months.

Sutent (sunitinib)

Oral pill. Small molecule against receptor tyrosine kinase.

2006

Progression-free survival time extended by 6.3 months.

Sorafenib (Nexavar)

Oral pill. Small molecule inhibitor of VEGFR, PDGFR, and Raf kinases.

2005

Progression-free survival time extended by 3 months. Standard treatment until Axitinib.

Table II. Leading Treatment Options for Renal Cell Carcinomas

ASONEP

ASONEP is an alternative formulation of iSONEP that also targets Sphingosine 1 Phosphate (S1P) using a humanized monoclonal antibody. Whereas iSONEP is administered ocularly for AMD, ASONEP is administered through intravenous infusion (Selvaraju and Chen, Aegis Capital Corp, 2012).

In animal models, ASONEP has been shown to achieve anti-angiogenic and anti-tumor activity. If this is the same case in humans, ASONEP may also help cancer patients overcome drug resistance as S1P is correlated with the development of drug resistance in multiple tumor types.

Lpath finished Phase I clinical trials for ASONEP in 2010 and found that ASONEP was tolerated at all dose administered. ASONEP was tested in cancer patients with various forms of late-stage cancer. From the Phase I data, ASONEP appears to have fewer adverse effects than Avastin, including no hypertension, no significant hemorrhage, and only infusion-related reactions at high doses (24 mg/kg).

Lpath is currently recruiting patients for Phase IIa clinical trials for ASONEP. Phase IIa trials started February 2013 and are expected to finish in March 2015. Eligible subjects include patients who have tumors that cannot be removed by surgery and patients who have failed three prior treatments including VEGFP and/or mTOR inhibitors. An estimated thirty-nine subjects have been enrolled in the trial for eight weeks. The primary endpoint that will be measured is progression-free survival of > 60% of patients. If this endpoint were met, it would allow a second cohort would start enrollment. If ASONEP shows no efficacy after the first cohort, the trial may be stopped. The trial will also be measuring safety and tolerability, pharmacokinetics through concentrations, tumor response rate, changes in selected markers, and changes in anti-drug antibodies. Pfizer has the first refusal rights to in-license ASONEP if initial Phase II trials of ASONEP look promising.

Conclusion

It is quite rare to see a company with a ~$65M market cap, a great business plan and positive characteristics for success in biotechnology. Lpath is likely to succeed for three reasons:

The lead candidate drug, iSONEP has a unique multimodal mechanism of action that demonstrated great efficacy and differs from the three leading products in the wet AMD market today. Moreover, the lead product targets a high value industry and indication (ophthalmology) that also has a lower risk profile due to the absence of systemic exposure. In addition, this is the first drug of its class, which would set the company as a leader in lipidomics; however, it may also face resistance from the FDA due to the same reason.

The monoclonal antibody technology platform ImmuneY2TM is unique in a niche environment. The technology directly targets the lipid rather than its downstream proteins, thus differentiating it from the strategies taken by most of the protein-centric companies. Moreover, lipidomics is a nascent field though research is progressing with new evidence of lipids as a potential therapeutic target; new product candidates and additional disease indications will emerge as research advances, which will serve the company well, a leader in this field. Currently, Lpath has two other candidate products in addition to its lead product, which is great planning and business management.

Lpath is in a high-value industry: Over the past decade multiple monoclonal antibody companies have been acquired in deals ranging from $1.1 to $15 billion (Selvaraju and Chen, Aegis Capital Corp, 2012). It is highly probable that Pfizer, having agreed on $497 milestone payment for Lpath's lead indication, would acquire Lpath upon favorable Phase II trial results. Such an early acquisition may enable Lpath to expand its pipeline with the current Immune Y2TM platform. Indeed, this partnership with one of the world's largest pharmaceutical companies indicates that the drug has a high chance of success. In addition, Lpath is expanding its revenue stream through partnership in diagnostics with Provista Diagnostics, which should generate enough cash until the projected approval and launch date of its lead product, iSONEP in 2017 or an acquisition bid after its Phase II trials by Pfizer

MFG

Chali

Optionen

| Boardmail an "Chalifmann3" |

Wertpapier: Apollo Endosurgery |

MFG

Chali

Optionen

| Boardmail an "Chalifmann3" |

Wertpapier: Apollo Endosurgery |

Optionen

| Boardmail an "Chalifmann3" |

Wertpapier: Apollo Endosurgery |

Angehängte Grafik:

z.png (verkleinert auf 63%)

z.png (verkleinert auf 63%)

Lpathomab functions like a 'molecular sponge' that binds to and neutralizes the bioactive lipid signaling molecule, lysophosphatidic acid (LPA). In this way, the LPA receptors associated with the transmission of pain through the nervous system are silenced. Lpathomab was discovered using Lpath's proprietary ImmuneY2™ drug-discovery technology.

In collaboration with researchers at the University of California, San Diego, Lpath has already generated strong, reproducible data in an accepted animal model in which significant pain relief was observed in diabetic rats after Lpathomab treatment.

The Small Business Innovative Research (SBIR) program of the NATIONAL INSTITUTE OF DIABETES AND DIGESTIVE AND KIDNEY DISEASES granted this award (1R43DK098829-01), which will provide Phase 1 funding to conduct in vivo studies of diabetic neuropathy in diabetic rats that will be treated with Lpathomab. Diabetic peripheral neuropathy (DPN) is the most common long-term complication of diabetes mellitus and affects about 50% of patients with either type-1 or type-2 diabetes. Patients with DPN often experience debilitating pain symptoms that affect day-to-day functioning and quality of life. Many patients with DPN-related pain do not respond adequately to any treatment option currently available, signifying a strong unmet need to develop new, more efficacious drugs.

"We are pleased the NIH has recognized the value of Lpath's innovative approach of neutralizing LPA to treat diabetic neuropathic pain," stated Dr. Rosalia Matteo, associate director at Lpath and the principal investigator on the grant. "With NIH support, we plan to continue generating compelling data and advancing Lpathomab, a compound that could potentially fill the tremendous void that exists in the neuropathic pain market."

About Lpathomab and Lpath's proprietary ImmuneY2™ technology

Lpathomab was generated using Lpath's proprietary ImmuneY2™ technology. This drug-discovery engine provides Lpath with a unique platform from which to generate antibodies against bioactive lipids, opening up an entire new array of drug-discovery possibilities. About 1,000 bioactive members of the lipidome are believed to exist, but the number could be considerably larger as the study of lipidomics continues to expand. Nature Reviews stated that bioactive lipids promise to occupy center-stage in cell-biology research in the twenty first century. No other company or research institution has demonstrated an ability to generate therapeutic-grade monoclonal antibodies against lipids.

MFG

Chali

Optionen

| Boardmail an "Chalifmann3" |

Wertpapier: Apollo Endosurgery |

Lpath demonstriert vorklinische Wirksamkeit von Lpathomab(TM) und startet Humanisierungsprozess

San Diego (ots/PRNewswire) -

- Ergebnisse liefern weitere Bestätigung von auf Lipidomen

basierenden Therapeutika als aufkommendes Gebiet der

Medikamentenforschung

Lpath, Inc. (OTC Bulletin Board: LPTN), der Branchenführer bei

therapeutischen Wirkstoffen gegen bioaktive Lipide, meldete heute

positive Ergebnisse in zahlreichen Mausmodellen von Humankrebs und

AMD mit Lpathomab(TM), dem monoklonalen Mausantikörper des

Unternehmens gegen LPA (Lysophosphatsäure). Diese Ergebnisse

bestätigen die erwarteten starken anti-angiogenen und

anti-metastatischen Wirkungen von Lpathomab. Lpathomab wurde unter

Verwendung der firmeneigenen geschützten Technologieplattform

ImmuneY2(TM) entwickelt.

Basierend auf diesem positiven Ergebnis wird Lpath mit DataMabs in

London, England, zusammenarbeiten, um Lpathomab zu humanisieren und

einen führenden Antikörper für die vorklinische Entwicklung zu

erzeugen.

LPA ist ein bioaktives Lipid, das seit langem als bedeutender

Promotor des Krebszellwachstums und der Metastasenbildung bei einer

Vielzahl von Tumorarten bekannt ist und ausserdem signifikant zu

neuropathischen Schmerzen beiträgt.

"Die Humanisierung unseres Lpathomab Antikörpers ist ein

entscheidender nächster Schritt bei der Weiterentwicklung des

Projektes zur klinischen Reife", sagte Dr. Genevieve Hansen, Vice

President von Research bei Lpath. "Wir hatten in der Vergangenheit

viel Erfolg bei der Zusammenarbeit mit DataMabs und freuen uns auf

die erneute Kooperation bei unserem Lpathomab Projekt."

Dieses erfolgreiche Ergebnis mit Lpathomab folgt dem Erfolg von

Lpath mit seinem Sphingomab(TM) Programm auf dem Fusse. Sphingomab

ist ein Antikörper gegen ein weiteres bioaktives Lipid, das S1P.

Lpath humanisierte den Antikörper im Jahr 2006 und plant die

Einreichung eines IND-Antrags im November dieses Jahres für die

Verwendung von ASONEP(TM) (der systemischen Rezeptur der

humanisierten Form von Sphingomab) zur Behandlung von Krebs. Das

Unternehmen plant ausserdem die Einreichung eines zweiten IND-Antrags

zu Beginn des nächsten Jahres für die Verwendung von iSONEP(TM) (der

okularen Rezeptur der humanisierten Form von Sphingomab) zur

Behandlung von AMD. Die Einreichung eines IND-Antrags für die

Verwendung von humanisiertem Lpathomab ist für das Jahr 2009 geplant.

Dr. Roger Sabbadini, der Gründer und CSO von Lpath, merkte an:

"Diese hoch interessanten Ergebnisse liefern eine weitere Bestätigung

von auf Lipidomen basierenden Therapeutika als ein wichtiges neues

Gebiet der Medikamentenforschung. Lpath war eines der ersten

Unternehmen, das erkannt hat, dass bioaktive Lipid-signalisierende

Moleküle wie S1P und LPA ausgezeichnete Targets für rationales

Drug-Design darstellen können. Durch Verfolgung dieser Targets und

Demonstration der überzeugenden Wirksamkeit haben wir eine gesamte

Klasse von auf Lipidomen basierenden Therapeutika für die Behandlung

von Krebs, Diabetes, neurodegenerativen Erkrankungen,

Immunfunktionsstörungen, Entzündungen, Schmerzen, psychischen

Störungen und Herz-Kreislauf-Erkrankungen eröffnet."

Wissenschaftler sind heute davon überzeugt, dass es mehr als 1.000

Mitglieder des funktionellen Lipidoms gibt, von denen jedes ein neues

potenzielles Ziel für therapeutische Intervention darstellt.

Informationen zu Lpath:

Lpath, Inc., mit Hauptsitz in San Diego in Kalifornien, ist der

Branchenführer bei der Herstellung von auf Lipidomiden basierenden

Therapeutika, einem aufkeimenden medizinischen Forschungsbereich, bei

dem der Einsatz bioaktiver Signal-Lipide zur Behandlung wichtiger

Krankheiten des Menschen untersucht wird. ASONEP(TM) (die systemische

Rezeptur der humanisierten Form von Sphingomab(TM)) ist ein

Antikörper gegen S1P mit vielversprechenden Resultaten bei der

Behandlung von Krebs und anderen Krankheiten. Ein zweiter

Produkt-Kandidat, iSONEP(TM) (die okulare Rezeptur der humanisierten

Form von Sphingomab), hat bereits überzeugende Ergebnisse in

verschiedenen vorklinischen AMD- und Retinopathiemodellen erzielt.

Lpaths dritter Produkt-Kandidat, Lpathomab(TM), ist ein Antikörper

gegen LPA, einem wichtigen bioaktiven Lipid, das schon seit längerem

als ein geeignetes Target für bestimmte Krankheiten bekannt ist. Die

einzigartige Fähigkeit des Unternehmens, neuartige Antikörper gegen

bioaktive Lipide zu erzeugen, basiert auf seiner ImmuneY2(TM)

Plattform zur Medikamentenforschung, die vom Unternehmen dazu

verwendet wird, seine Produkt-Pipeline zu erweitern. Weitere

Informationen erhalten Sie im Internet unter http://www.Lpath.com

MFG

Chali

Optionen

| Boardmail an "Chalifmann3" |

Wertpapier: Apollo Endosurgery |

Optionen

| Boardmail an "Chalifmann3" |

Wertpapier: Apollo Endosurgery |

Angehängte Grafik:

z.png (verkleinert auf 63%)

z.png (verkleinert auf 63%)

http://www.ariva.de/forum/...-Apple-in-1997-buy-Organovo-today-470965 (200% im Plus)

http://www.ariva.de/forum/Astex-Pharmaceuticals-Hammer-459048 (300% im Plus)

http://www.ariva.de/forum/...uticals-erwartet-top-line-results-484717 (150% im Plus)

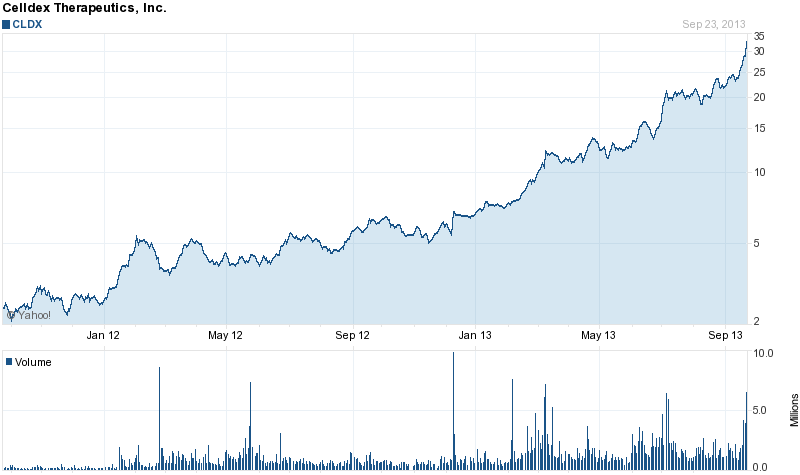

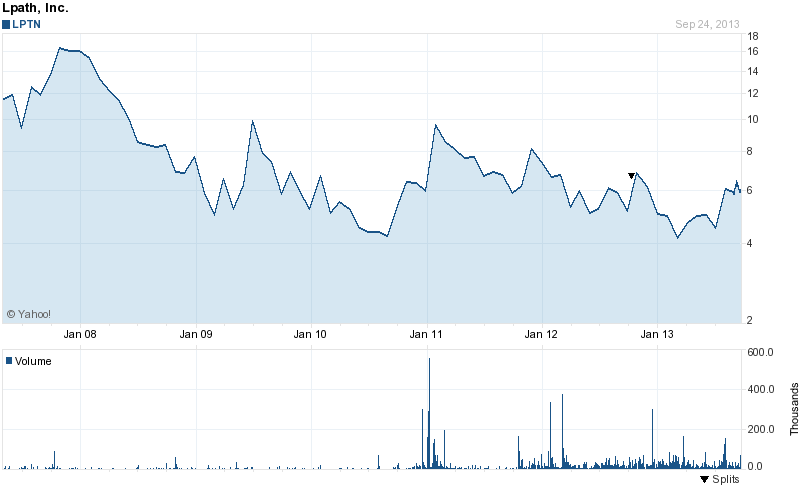

..... aber das ist alles nichts gegen das was uns bei Lpath in zukunft erwarten soll ! Schau dir einfach mein Post nr.24 mit Celldex an,die wesentlich weniger auf der Pfanne haben ,aber schon knapp 3 Mrd wert sind ! Das liegt daran ,dass Antikörperaktien in der Regel sehr hoch bewertet sind,auch Seattle Genetics mit 5 MRD oder Regeneron mit 28 MRD ! Alle,nur meine Lpath mit 80 Mio noch nicht ! Ich halte es in der Tat für nicht ausgeschlossen ,dass Lpath in 10 Jahren so hoch wie Regeneron bewertet sein könnte (28 MRD),aber 5 MRD würden mir schon reichen,um 5000% mit meinem Invest einzustreichen,gerade wegen ISONEP ,das Medi hat in Phase 1 bessere Resultate als das von Regeneron bei macluar Degeneration (altersbedingte Blindheit) gezeigt !!!!! Die Finanzierung der Clinicals ist durch eine Partnerschaft mit Pfizer voll abgesichert,keine Insolvenzgefahr,ich warte auf die Phase-2 Ergebnisse ! Die Aktie Lpath ist völlig unter Radar,auch im Amiland nur kleine Umsätze ,so erkläre ich mir die geringe Mkap.

Nunja,ist dir eigentlich schon aufgefallen,dass hier bei Ariva eigentlich ausschliesslich Schrottaktien diskuttiert werden ? Da ist man eben relativ alleine,wenn man eine Biotechperle entdeckt hat,aber der Bierro und die LadyLuck schauen wenigens ab und zu mal hier rein,und jetzt auch du .....

Chali

Optionen

| Boardmail an "Chalifmann3" |

Wertpapier: Apollo Endosurgery |

http://www.ariva.de/forum/Schach-Thread-Provisorium-463012

Wir können sofort starten ......

Optionen

| Boardmail an "Chalifmann3" |

Wertpapier: Apollo Endosurgery |

MFG

Chali

Optionen

| Boardmail an "Chalifmann3" |

Wertpapier: Apollo Endosurgery |

Optionen

| Boardmail an "Chalifmann3" |

Wertpapier: Apollo Endosurgery |

Optionen

| Boardmail an "Chalifmann3" |

Wertpapier: Apollo Endosurgery |

Optionen

| Boardmail an "Chalifmann3" |

Wertpapier: Apollo Endosurgery |

Angehängte Grafik:

z.png (verkleinert auf 63%)

z.png (verkleinert auf 63%)

neugierig was da veröffentlicht wird - wechsel der CRO (auf verlangen von pfitzer) sowie details zur ISONEP zukunft ... ?

http://finance.yahoo.com/news/...s-plans-isonep-option-203000327.html

Optionen

| Boardmail an "lady luck" |

Wertpapier: Apollo Endosurgery |

Optionen

| Boardmail an "Chalifmann3" |

Wertpapier: Apollo Endosurgery |

Angehängte Grafik:

smilie_happy_011.gif

smilie_happy_011.gif

Anti-leukotriene antibodies were generated with ImmuneY2™, Lpath's drug-discovery engine

.....

SAN DIEGO, Nov. 21, 2013 /PRNewswire/ -- Lpath, Inc. (LPTN), the category leader in lipid-targeted therapeutics, has used its proprietary discovery technology to generate several monoclonal antibody product candidates targeting the leukotriene family of bioactive lipids. Leukotrienes are implicated in numerous inflammatory processes. The lead antibody, which binds to and neutralizes several different leukotriene isoforms, has shown positive in vivo results, and testing in animal models of respiratory disease, including asthma, is now underway.

"The scientific literature on the leukotriene pathway, coupled with our preliminary in vivo data, suggests that Lpath's approach of specifically targeting the bioactive lipid rather than the proteins themselves may have significant benefits over prior drug-discovery efforts in this area," said Gary Woodnutt, Ph.D., Lpath's senior vice president of research. "If the data continue to be positive and our preclinical development efforts are successful, we intend to file an IND sometime in late 2015."

Lpath's CEO, Scott Pancoast notes, "Our ImmuneY2 platform has again provided Lpath with a new promising program, underscoring the power and value of the technology. We look forward to updating investors on this and other advancements in the future."

Optionen

| Boardmail an "Chalifmann3" |

Wertpapier: Apollo Endosurgery |

The Pipeline

LPath has a mid-stage pipeline with its lead product candidate in Phase II testing. Below is a diagram detailing the pipeline at LPath:

iSONEP ASONEP Lpathomab Nextomab§

Partnered with Pfizer (PFE) Pfizer right of first refusal Not partnered Not partnered

Indicated for Wet AMD,RPE Detachment, and Diabetic Retinopathy Indications:Cancer, MS, Inflammation, Colitis Indications: CNS Disorders, Pain, Fibrosis, TBI Indications:Inflammation, Cancer, Ocular

Phase 2 testing Phase 2 testing Preclinical Discovery

This chart allows for us to draw some very interesting conclusions right off of the bat. First of all, LPath is partnered with Pfizer for its lead product candidate (which would of course mean that there is a large amount of potential) and secondly the pipeline is not very advanced yet, which could of course help to explain why the stock price and the market cap are rather low for this company. In order to evaluate the merits of an investment in the company, and in order to chart the potential for the company it becomes necessary for us to dive in much deeper into the actual pipeline candidates at LPath in order to truly see the potential.

iSONEP

iSONEP is perhaps the most important immediate product to the future of LPath. iSONEP is designed to help treat a myriad of different opthomological problems. While we do not have a great deal of data on the product, due to the product only being in phase II testing, it appears as though the product has significant potential over the long run.

Up to this point the Phase I trials in wet AMD have been rather good. First of all the drug was well tolerated by the patient population, and investors were given hints as to the efficacy of iSONEP as either a first line treatment or as an adjunct therapy. In the phase I trial a positive biological effect was observed in most patients, do not forget that these are the patients who failed treatment with the current standard of care Lucentis and Avastin. This patient population, failing the current standard of care, would of course be harder to treat, and therefore any hint of efficacy within the population can be positive for LPath.

The product is currently being studied in Wet-AMD, with results expected in the third quarter of 2014. The Phase I study was completed quite a while ago, and the delay heading into Phase II testing is solely based upon an FDA hold. Now, I know what you are thinking, but this was not an FDA hold that had anything to do with the product in question. LPath's fill/finish contractor was not in compliance with the FDA's Good Manufacturing Practice Requirements and as such the FDA put a clinical hold on LPath until the supplier either came into compliance or until LPath found a new supplier. With the supply issues now having been worked out, this should not be an issue going forward for shareholders and should not delay the development timeline any further.

This product is important, as it is currently partnered with Pfizer.Pfizer has the worldwide commercialization rights for the product candidate. Pfizer is currently sharing the costs of the Phase II Nexus trial with LPath, at which point Pfizer will have to make a very important decision after the data readout. Under the terms of the agreement Pfizer has two options: 1) Exercise its option to develop the product candidate, or 2) Lose all of its development rights. Should the data be positive, the decision of Pfizer will likely be the former. This can be very lucrative for LPath for the following reasons. Upon Pfizer exercising its option, Pfizer will pay an undisclosed sum to LPath, Pfizer would be responsible for the costs of all future commercialization activities, LPath would be eligible for milestones of up to $497.5 million in development and commercialization goals, and LPath would receive a tiered double digit royalty on any product sales.

This agreement has the potential to be very important for a company that has a rather small market cap and could provide a very large amount of revenue going forward. However, Pfizer recently announced that it is looking to divest some of its ophthalmology assets, and that its iSONEP worldwide rights is one of the assets being divested. The bright side of this is that a sale to a third party does not change the terms of the partnership agreement, and that third party would still have to pay all of the money that Pfizer would have to pay. There also appears to have been substantial interest in the iSONEP option as it was recently announced that iSONEP's bid to regain the rights to worldwide commercialization was not the highest and that there were other offers that were more competitive. With this in mind, there appears to be significant interest in the iSONEP asset which bodes well for the future of the program.

The phase II nexus trial seems as though it will be quite extensive, and that is should provide a much better idea as to the future of the iSONEP asset. From a risk-reward standpoint, should the trial be positive then the stock should go up significantly based on the future partner exercising their development rights to the product. Whereas if the trial fails then that would likely be a rather big blow to the overall future of LPath. However, given the promising phase I trial results I am predicting success for the Phase II trial.

iSONEP is also looking at potential indications in retinal pigment epithelium detatchment (RPE). Any additional indications would, of course, add value to the asset and would increase the commercialization potential of the asset. The significant sales potential of the asset, coupled with the fact that LPath would get the revenue for almost free (considering that past phase II trials the revenue would come in as development milestones and royalties), this product has the potential to help guide the future of LPath for years to come.

ASONEP

Asonep is another very promising product in LPath's pipeline which is capable of helping to drive long term shareprice growth going forward. ASONEP is being studied in a variety of indications, but is also a product associated with the Pfizer agreement. Pfizer currently has for a limited time the right to first refusal to partner on ASONEP. This product has the potential to generate significant revenue going forward for LPath, should Pfizer choose to partner on the product.

ASONEP is also currently in phase II testing in Renal Cell Carcinoma (RCC). What is significant about the phase II trial is that LPath is choosing patients who have either failed three prior treatments for RCC, or who have RCC that is inoperable. These patients would be harder to treat than average RCC patients, and this is significant because if ASONEP is able to show benefits with a rather clean adverse effect record it should be well on its way to achieving FDA approval. According to clinicaltrials.gov (linked earlier on in the paragraph), the estimated Primary Completion Date for the trial is in December of 2014. This means that we should see data pretty soon after the primary completion date for the trial so I would tentatively predict data in either January or February, this would mean that while results are far away investors might be able to get in now at a low price and then benefit from a significant runup heading into the final release of the data. with the importance of the Phase II data in mind, lets take a quick peak at the Phase I data and see if that can give us any insight as to the possible outcome of the Phase II trial.

The Phase I trial was largely successful. The drug was well tolerated with no adverse side effects. Significantly many of the patients that were studied achieved 'stable disease' in regards to their cancer size. This is important because that would mean that the drug stopped the growth of cancer and would help to suggest that the drug does have the potential for a rather large amount of efficacy.

It is also worth pointing out that while LPath is paying for the trials, the phase I and IIa trials are being funded in part by a $3 million grant from the National Cancer Institute. This will help to offset some of the funding costs for the trial and should help to save LPath money over time. Further clinical trials may be paid for by Pfizer, should it execute an agreement similar to the one existing for iSONEP. Also, having such a well respected agency such as the National Cancer Institute helps to show that this program is needed amongst the cancer community and that the treatment represents a meaningful step forward for patients.

The market for ASONEP could be very large, even if it is considered to be a second line therapy. There are, unfortunately, 225,000 new cases of Renal Cell cancer every year in the world. With a market of this size, it would be possible for LPath to carve out a very lucrative niche, especially should it successfully partner with a large pharmaceutical company like Pfizer. ASONEP will be an asset that investors will pay close attention to and the possible addition of a Pfizer partnership would only add value to the program. ASONEP has the potential to help drive long term shareprice growth and to provide significant returns for investors.

Other Pipeline Products

The two pipeline products covered above are well ahead of the other development programs in LPath's pipeline. As the pre-clinical Lpathomab continues to advance within the clinical trial process it should help to drive shareholder growth. Interestingly, the Lpathomab program was recently the recipient of a $145,000 grant from the National Institute of Health to help fund the expenses associated with a phase I trial.In pre-clinical data Lpathomab showed the ability to significantly reduce pain, which represents a potential path forward for the development of the product.

Nextomab is still in the discovery phase and as such investors do not know a great deal about the program. It has the potential to help drive shareprice growth as more information about the program is released and as the product candidate advances through clinical testing.

Finally, LPath recently announced yet another new drug discovery program called Altepan. The potential indication for this program is in respitory disease, which would of course be a rather large market depending upon the specific indication. The company expects that if the preclinical results continue to come back positive, that they will file an IND with the FDA towards the end of 2015. While this is a rather long period of time away, as the product advances it could have the potential to increase the shareprice and it could be very important for long term oriented investors.

Financial Position

Another key consideration when looking at investing in any company is the financial position of the company. For a company that is primarily engaged in researching its drug candidates we can expect for LPath to be operating at a loss. It is important going forward, however, for investors to monitor LPath's cash and cash equivalents in order to avoid dilution.

As of September 30, 2013 LPath had cash and cash equivalents of $14.9 million. This should be sufficient, given LPath's current cash burn rate, to fund their operations through the third quarter of 2014. Given that fact, it appears as though the immediate risk of dilution is off of the table and I would expect for the company to hold off on dilution until the stock moves higher in anticipation of the upcoming clinical data for iSONEP. The company also has an at the market issuance program which may allow for the company to issue shares to the public from time to time. While this is not necessarily a good thing, the fact that it is in place suggests that LPath might not dilute all at once and instead spread the dilution over time which would be preferable. The limit is $20 million which would help to substantially increase LPath's cash coffers. Also, do not forget that the partnership agreement on iSONEP would provide for a significant payment should Pfizer elect to continue developing iSONEP.

LPath does at least receive some revenue due to the grants and reimbursable costs that it has as a result of its partnership programs. This revenue helps to offset some of the impact of the operating loss at LPath. The research and development costs have been increasing through recent quarters, as a result of having to take over the next $6 million in clinical trial costs related to iSONEP and also due to the other drug development programs in LPath's pipeline.

While a large loss is usually a concern, for a developmental stage company I am usually willing to overlook the loss. The company is still trying to research its products and as the products advance through the pipeline, investors should see the share price go up despite the losses at LPath. Furthermore, if Pfizer elects to exercise its option this could do a great deal towards helping to minimize the operating loss as LPath would no longer have to spend money on the development of iSONEP. So, in summary, I believe that with sufficient cash through the third quarter of 2014 and the possibility of a Pfizer partnership, that LPath is in a good enough financial position to merit investment consideration.

Conclusion

LPath's development pipeline will be the long term driver of shareprice growth. The upcoming results for the iSONEP trial represent a meaningful catalyst for long term oriented investors and should help to apprise the true value of LPath's pipeline. It appears as though with LPath trading well off of its 52 week high, that now might be a good time to get into the stock. It also appears as though for the long term, LPath is set up to provide significant returns to patient investors.

Optionen

| Boardmail an "Chalifmann3" |

Wertpapier: Apollo Endosurgery |

Hals und Beinbruch wünscht .....

MFG

Chali

Optionen

| Boardmail an "Chalifmann3" |

Wertpapier: Apollo Endosurgery |

Publication Further Validates Lpath's Approach to Targeting Bioactive Lipids for Drug Discovery

Lpath, Inc. March 5, 2014 7:30 AM

SAN DIEGO, March 5, 2014 /PRNewswire/ -- Lpath, Inc. (LPTN), the industry leader in bioactive lipid-targeted therapeutics, has brought scientists one step closer to finding a potential treatment for traumatic brain injury (TBI) with a recent publication showing that Lpathomab™, a therapeutic antibody, reverses much of the damage caused by trauma to the nervous system.

As published by the Journal of Neuroinflammation (vol. 11, article 37), Lpathomab can be used to reduce the size of a TBI and to improve functional behavioral outcomes in experimental animal models. The antibody works as a molecular sponge by soaking up lysophosphatidic acid (LPA), a molecule that can damage neurons and promote dangerous inflammatory responses in the central nervous system.

In collaboration with scientists at the University of Melbourne, the antibody was tested in mice that had TBIs. A key finding of the study was the significant efficacy of administering Lpathomab after an injury, thus demonstrating a potential therapeutic benefit. Also shown for the first time in this groundbreaking paper was that human patients with TBI exhibited substantial increases in the levels of LPA in the cerebrospinal fluid (CSF) after injury, a finding also seen in the injured mouse model of TBI; such data suggest that LPA is a valid target for therapeutic intervention.

Lpath and its Melbourne collaborators have recently shown that Lpathomab provides protection against neuronal cell death and scarring in experimental models of spinal cord injury (SCI), published recently in the American Journal of Pathology (Goldschmit et al., vol. 181, p. 978-992). Currently, there are no FDA-approved drugs for the treatment of neurotrauma such as TBI and SCI.

"This research provides new hope for therapeutic treatments for many forms of neurotrauma, including TBI and SCI as well as other forms of neurodegenerative disorders," said Roger Sabbadini, Ph.D., vice president and founder of Lpath and co-author on the paper. "We believe that LPA may be a biomarker that could be used to aid in the diagnosis of TBI, as the 'LPA pulse' that occurs in the injured brain can also be detected in blood."

The research team was comprised of Lpath scientists and collaborators from the University of Melbourne, Monash University and the University of Kentucky.

As a promoter of tumorigenesis, metastasis and fibrotic disease, LPA is a well-validated drug target and has been shown to play a significant role in neuropathic pain and now neurotrauma. The role of LPA in the nervous system has been described in a recent review published in the International Review of Cellular and Molecular Biology (Frisca et al., vol. 296, p. 273-322).

Lpathomab is currently in IND-enabling studies for neuropathic pain and neurotrauma.

Lpathomab was generated using Lpath's proprietary ImmuneY2™ technology, a drug-discovery engine that provides Lpath with a platform to generate antibodies against bioactive lipids, opening up a new array of drug-discovery possibilities. About 1,000 bioactive members of the lipidome are believed to exist, but the number could be considerably larger as the study of lipidomics continues to expand. Nature Reviews stated that bioactive lipids promise to occupy center-stage in cell biology research in the twenty-first century.

Lpath utilized ImmuneY2 to discover an antibody against another bioactive lipid, sphingosine-1-phosphate (S1P). This antibody, sonepcizumab, is formulated as iSONEP™ for ocular delivery and as ASONEP™ for systemic delivery. In addition, the ImmuneY2 platform was used to generate Altepan™, an antibody against key leukotrienes that have been implicated in various respiratory diseases, including asthma

Optionen

| Boardmail an "Chalifmann3" |

Wertpapier: Apollo Endosurgery |

Chalif, was sagst Du?

http://finance.yahoo.com/news/...trial-progress-poster-120000597.html