Kursverdoppelung bei Actua Corporation (vorm. Internet Capital)

Seite 60 von 385 Neuester Beitrag: 02.02.24 06:39 | ||||

| Eröffnet am: | 06.12.05 13:53 | von: Libuda | Anzahl Beiträge: | 10.605 |

| Neuester Beitrag: | 02.02.24 06:39 | von: ReeCoupons | Leser gesamt: | 1.381.868 |

| Forum: | Hot-Stocks | Leser heute: | 97 | |

| Bewertet mit: | ||||

| Seite: < 1 | ... | 57 | 58 | 59 | | 61 | 62 | 63 | ... 385 > | ||||

http://biz.yahoo.com/ap/070407/india_sca...

Internet Capital owns 34% of Freeborders, who will increase his chinese staff to 2,000 in 2007. 200 employers are in the headquarter in USA and other places in North-America and Europe and about 50 in a subsidiary in New York (Wall Street

ICGE

Internet Capital Group, Inc. NASDAQ-GM

Institutional Holdings Description | Hide Summary

Company Details

Total Shares Out Standing (millions): 39

Market Capitalization ($ millions): $454

Institutional Ownership: 72.3%

Price (as of 4/12/2007) 11.74

Ownership Analysis # Of Holders Shares

Total Shares Held: 101 27,926,784

New Positions: 11 1,941,384

Increased Positions: 38 4,958,548

Decreased Positions: 39 3,841,077

Holders With Activity: 77 8,799,625

Sold Out Positions: 15 1,734,439

Click on the column header links to resort ascending ( ) or descending ( ).

Owner Name Select a name below for more information. Date Shares Held Change(Shares) % Change(Shares) Value($1000)

GENDELL JEFFREY L 12/31/2006 3,262,780 0 0.00% $38,305

DIMENSIONAL FUND ADV... 12/31/2006 3,112,704 492,549 18.80% $36,543

CAPITAL RESEARCH & M... 12/31/2006 3,075,000 275,000 9.82% $36,101

SCHNEIDER CAPITAL MA... 12/31/2006 1,689,467 (10,125) (0.60%) $19,834

BARCLAYS GLOBAL INVE... 12/31/2006 1,634,229 167,653 11.43% $19,186

EMERALD ADVISERS INC... 12/31/2006 1,066,391 960,891 910.80% $12,519

COLUMBIA PARTNERS L ... 12/31/2006 1,026,385 (13,143) (1.26%) $12,050

MELLON FINANCIAL COR... 12/31/2006 971,192 (1,465,389) (60.14%) $11,402

ARIENCE CAPITAL MANA... 12/31/2006 960,556 (173,761) (15.32%) $11,277

EAGLE ASSET MANAGEME... 12/31/2006 747,920 1,045 0.14% $8,781

PEQUOT CAPITAL MANAG... 12/31/2006 740,000 269,000 57.11% $8,688

FMR CORP 12/31/2006 726,116 726,116 New $8,525

TCW GROUP INC 12/31/2006 646,976 251,620 63.64% $7,595

TUDOR INVESTMENT COR... 12/31/2006 596,388 0 0.00% $7,002

STATE STREET CORP 12/31/2006 580,293 (25,500) (4.21%) $6,813

VANGUARD GROUP INC 12/31/2006 503,002 18,700 3.86% $5,905

PLATINUM INVESTMENT ... 12/31/2006 450,000 - - $5,283

MASON CAPITAL MANAGE... 12/31/2006 422,742 422,742 New $4,963

DEUTSCHE BANK AG\ 12/31/2006 392,539 11,785 3.10% $4,608

ENGEMANN ASSET MANAG... 12/31/2006 390,080 84,493 27.65% $4,580

MORGAN STANLEY 12/31/2006 312,565 (118,972) (27.57%) $3,670

NORTHERN TRUST CORP 12/31/2006 311,725 28,798 10.18% $3,660

RENAISSANCE TECHNOLO... 12/31/2006 282,800 84,200 42.40% $3,320

HOCKY MANAGEMENT CO ... 12/31/2006 282,600 0 0.00% $3,318

BRUCE & CO., INC. 12/31/2006 273,300 (5,000) (1.80%) $3,209

GENDELL JEFFREY L

200 PARK AVE

NEW YORK, NY 10166

(212) 692-3694

Gendell Jeffrey owns near 3.3 million shares = more than 8%.

India's Infosys reports quarterly profit jumps 70% on outsourcing demand

Associated Press

NEW DELHI — India's Infosys Technologies Ltd. said quarterly net profit jumped 70.4 per cent from a year ago on sustained momentum in outsourcing and predicted on Friday that revenue would grow as much as 30 per cent this year.

Bangalore-based Infosys said net profit rose to $259-million (U.S.) in the January-March quarter compared with $152-million in the same period a year ago. Profit for the latest quarter included a tax refund of about $29-million, it said.

Revenues rose 46 per cent to $863-million during the quarter, taking annual revenues in the financial year ended March to $3.1-billion. Infosys' financial year runs from April through March.

The earnings numbers, which conform to U.S. accounting standards, beat analysts' expectations and lifted Infosys shares by 2.9 per cent in intraday trading on the Bombay Stock Exchange.

Related to this article

Latest Comments

Comments are closed for this story | Send a letter to the editor

Chief Executive Nandan Nilekani said the company expects its revenues to top $4-billion in the current financial year.

“It's a firm outlook. We are seeing robust growth. We are not seeing any slowdown (in outsourcing orders),” Mr. Nilekani said.

Scores of Western companies routinely hire Indian firms to handle software development, back-office operations and other work such as managing their information technology infrastructure. Outsourcing these tasks helps them save on costs as wages are low in India and skilled workers are easily available.

Infosys' forecast of 28-30 per cent growth in the 2007-08 financial year came despite concerns of an economic slowdown in the United States, where most of its clients are located, and an appreciation in the value of the Indian currency, the rupee.

The company, which works for firms like Goldman Sachs and J.C. Penney Co., said it added 34 new clients and 2,809 employees during the quarter.

Infosys' yearly guidance boosted other tech stocks.

The Bombay Stock Exchange's 30-share Sensex rose 2.2 per cent to 13,403 points in intraday trading as investors bought technology shares taking cue from Infosys, which was the first to report quarterly earnings.

Rivals Tata Consultancy Services Ltd. and Wipro Ltd., which are scheduled to release their earnings next week, climbed 4.2 per cent and 4 per cent respectively.

Infosys, however, lowered its earnings per share guidance for 2007-08 to 25.7 per cent to 27.7 per cent from last year's 45 per cent. The company said each of its shares listed on the Nasdaq is expected earn between $1.86 and $1.89 this year, compared with $1.48 last year.

Mr. Nilekani said the lower predicted EPS growth was largely because a large number of employees have recently exercised their stock options, resulting in a bigger pool of floating shares.

Google to Acquire DoubleClick for $3.1B (Not rated) 15-Apr-07 12:18 pm The fear will BIG SHORT and his frieds will become bigger, when they read about the 3.1 billions for Doubleclick and recognize that Internet Capital had a full pipeline of internet-companies.

Google to Acquire DoubleClick for $3.1B

Email Print Normal font Large font April 14, 2007 - 4:20PM

Seeking to expand its already well-honed ability to sell targeted Internet advertisements, online search leader Google Inc. said it has agreed to pay $3.1 billion in cash to acquire ad-management technology company DoubleClick Inc.

The two companies announced the deal after the markets closed Friday. The boards of both companies have approved the takeover, which is expected to close by the end of the year.

New York-based DoubleClick helps its customers place and track online advertising, including search ads, which Google _ more than its nearest search competitors Yahoo Inc. and Microsoft Corp. _ has turned into an extremely lucrative business.

DoubleClick had been the target of a fierce bidding war between Microsoft and Google, and Google's winning bid is nearly three times the amount DoubleClick fetched when it went private in 2005 for $1.1 billion.

The acquisition is the largest in Google's history, beating out the $1.76 billion deal for online video-sharing site YouTube Inc. late last year.

Though Google commands the lion's share of the online advertising search market, the addition of DoubleClick's technology and client network will help further its efforts to branch out beyond simple text ads and into more multimedia offerings.

Google and DoubleClick said their combination will offer media buyers and sellers more powerful tools for targeting and analyzing online advertisements and "serving," or placing them, on an even larger network of Web sites.

"It has been our vision to make Internet advertising better _ less intrusive, more effective, and more useful," Sergey Brin, Google's co-founder and president for technology, said in a statement. "Together with DoubleClick, Google will make the Internet more efficient for end users, advertisers, and publishers."

Shares of Mountain View-based Google fell $2.52 to $463.77 in after-hours trading. DoubleClick has been privately held since 2005.

The sellers are San Francisco-based private equity firm Hellman & Friedman, along with JMI Equity and DoubleClick management.

© 2006 AP DIGITAL

This story is sourced direct from an overseas news agency as an additional service to readers. Spelling follows North American usage, along with foreign currency and measurement units.

Sentiment : Strong Buy

Google kauft DoubleClick für 3,1 Milliarden US-Dollar

Online-Werbung soll effizienter und weniger aufdringlich werden

Im Rennen um das Online-Werbeunternehmen DoubleClick hat sich Google unter anderem gegen Microsoft durchgesetzt. Allerdings zahlt Google dafür einen stolzen Preis von 3,1 Milliarden US-Dollar, nachdem im Vorfeld darüber spekuliert wurde, DoubleClick könne für rund 2 Milliarden US-Dollar den Besitzer wechseln.

Ende März 2007 berichtete das Wall Street Journal, dass der Finanzinvestor Hellman & Friedman einen Käufer für DoubleClick suche, aber auch über einen Börsengang nachdenke. Hellman & Friedman kaufte DoubleClick 2005 für rund 1,1 Milliarden US-Dollar und hat seitdem einige Teile des Unternehmens veräußert, um an anderen Stellen hinzuzukaufen. So gehört der einstige deutsche DoubleClick-Konkurrent Falk eSolutions AG mittlerweile zu DoubleClick.

Nun geht DoubleClick für 3,1 Milliarden US-Dollar in bar an Google. Auch Microsoft hatte angeblich entsprechende Gespräche geführt. Das Unternehmen bietet Dienste rund um Online-Werbung an, betreibt unter anderem AdServer für zahlreiche Webseiten, machte 2006 etwa 150 Millionen US-Dollar Umsatz und ist weltweit Marktführer in diesem Bereich.

Künftig werde Google zusammen mit DoubleClick "überlegene" Werkzeuge für die Auslieferung und Analyse zielegerichteter Werbung anbieten. Die Relevanz von Anzeigen, die Nutzer zu Gesicht bekommen, soll steigen. Website-Betreibern verspricht Google Zugang zu neuen Kunden und eine effiziente Monetarisierung ihrer Werbeplätze. Agenturen und Werbekunden will Google künftig einen einfachen Weg bieten, klassische Online-Werbung und Keyword-Advertising über eine Schnittstelle abzuwickeln.

"Es war immer unser Ziel, Online-Werbung besser zu machen - weniger aufdringlich, effektiver und nützlicher. Zusammen mit DoubleClick wird Google das Internet für Nutzer, Werbtreibende und Website-Betreiber effizienter machen", kommentiert Google-Gründer Sergey Brin die Übernahme. Google-Chef Eric Schmidt geht davon aus, dass sich Google durch die Übernahme schneller am Markt durchsetzen wird. (ji)

http://messages.finance.yahoo.com/...d=246940&mid=246940&tof=16&frt=1

Durch die Übernahme von Doubleclick ergeben sich für ChannelIntelligence gigantische Chancen, denn viele Werbetreibenden die sich nicht vollständig in die Fänge von Google begeben wollen, werden zumindest was die Erfolgskontrolle anbetrifft nach einer Alternative suchen: eben ChannelIntelligence.

Seht einfach einmal in die obige Adresse rein.

http://channelintelligence.vnewscenter.c...

Internet Capital owns 40% of ChannelIntelligence.

Sentiment : Strong Buy

Börse

Frankfurt

Aktuell

8,67 EUR

Zeit

18.04.07 15:58

Diff. Vortag

-0,69 %

Tages-Vol.

19.845,97

Gehandelte Stück

2.325

Geld

8,65

Brief

8,82

Internet Capital hält hier 15% an einem Unternehmen, das einen Marktwert von ca. einer Milliarde Dollar haben dürfte.

Schon schön und gut was Internet Cap. so alles im Portfolio hat. Sicher ist Internet Cap. erheblich mehr wert als der Börsenkurs aussagt, aber solange die Jungs nicht auch mal Gewinne realisieren, dürfte ein entsprechender Kursaufschwung noch auf sich warten lassen.

Deshalb ist Internet Cap. ein Aktie, die nur gekauft werden sollte, wenn man wirklich langfristig - also mehr als 2 Jahre - investieren will! Dann allerdings gehört IC zu meinen absoluten Favouriten!

Optionen

| Boardmail an "CK2004" |

Wertpapier: Actua |

Meines Erachtens wird diese Strategie ins Auge gehen - und zwar dann wenn die erste größere Monetarisierung kommt. Meines Erachtens steht uns eine Monetarisierung bevor, zwar keine der BIG FIVE, aber doch eine die 50 Millionen in die Kassen spielen dürfte - mit denen keiner gerechnet hat, denn so viel hatten die meisten für die 5% an Emptoris nicht auf der Rechung.

Im folgenden Artikel wird Emptoris als heißer IPO-Kandidat gehandelt. Es unterscheidet sich sogar positiv von den anderen dort genannten Kandidaten, denn Emptoris ist wesentlich größer als die meisten der dort angeführten Kandidaten. In 2006 lag der Umsatz bei etwas 120 Millionen Dollar und er dürfte in 2007 zwischen 150 und 180 Millionen liegen. Emptoris schreibt zudem schwarze Zahlen - und das nicht nur beim Ebitda. Damit der IPO-Marktkapitalisierung bei mindestens einer Milliarde liegen.

The ipo of Emptoris is very near. It was named in the following article:

Boston Business Journal - April 13, 2007

by Todd WallackJournal staff

Dev Ittycheria’s BladeLogic is the latest profitless company to file for an IPO.

View Larger Who needs profits? A growing number of local tech companies are launching IPOs this year, despite never recording a profitable quarter.

Salary.com Inc. in Waltham, for instance, successfully went public in February, despite a history of red ink. And at least three other money-losing Massachusetts companies recently filed to go public as well: Netezza Corp. in Framingham, Bridgeline Software Inc. of Woburn and BladeLogic Inc. of Lexington.

That said, some profitable companies have recently filed to go public, too, including Starent Networks Corp. of Tewksbury and Monotype Imaging Holdings Inc. of Woburn. And many more local companies could also go public -- profitable or not -- taking advantage of an IPO market that has been sizzling since September.

"The IPO market that we are seeing today is probably the best six-month window that we have seen in the tech IPO markets since the bubble," said Brian Truesdale, managing director of Deutsche Bank in Boston.

According to conventional wisdom, companies used to have to post at least $50 million in annual revenue and two quarters of profitability to go the IPO route. But Truesdale said that doesn't necessarily apply to fast-growing tech companies. He said companies as a rule generally need $10 million to $12 million in quarterly revenue and positive cash flow to go public, but the ratios vary widely depending on the industry niche, business model and growth rate.

For instance, Salary.com had just $16 million in sales last year, but Salary.com also sells "on demand" software through a subscription model, ensuring that it will continue to reap revenue from most of the same customers in the future.

In addition, Truesdale said some companies could try to take advantage of the IPO market by going public earlier than they normally would. Truesdale estimated there are currently 15 to 20 tech companies in the region that may be poised to go public soon.

Nothing's been announced, but industry insiders say possible contenders include: Airvana Inc. in Chelmsford, Crossbeam Systems Inc. in Boxborough, Cedar Point Communications Inc. in Derry, N.H., Equallogic Corp. in Nashua, N. H., Emptoris Inc. in Burlington, Openpages Inc. of Waltham, Netcracker Technology Corp. of Waltham and Spotfire Inc. in Somerville. In addition, Hopkinton-based EMC Corp. recently announced plans to sell 10 percent of its VMware subsidiary to the public through an IPO.

BladeLogic, which makes software to run corporate data centers, is just the latest company to file for an IPO. Though the company's revenue is relatively modest by IPO standards ($37.4 million over the past 12 months), it has been growing quickly. In the latest quarter, BladeLogic took in $12.8 million in revenue, compared with $6 million for the same period a year ago.

The company has 229 workers and expects to hire "significant numbers of new employees, according to its filing with the Securities and Exchange Commission. The company's chief executive is Dev Ittycheria.

And though BladeLogic has never been profitable since it was founded in July 2001, it was close to breaking even in the latest quarter.

BladeLogic said it had more than 200 customers, including Lockheed Martin Corp., Time Warner Inc. and Priceline.com Inc.Rivals include BMC Software Inc. Hewlett-Packard Company, and IBM Corp.

Todd Wallack can be reached at twallack@bizjournals.com.

Re: Internet Capital has a full ipo-pipeline (Not rated) 1 minute ago But Emptoris is bigger than the most companies in the article. The revenues in 2006 was about 120 million and could increase to 150-170 million in 2007. And Emptoris had a positve net income.

Therefore we will have a one-billion-ipo or more. The result is, that the 5% of Internet Capital has a worth of 50 million or more.

Sentiment : Strong Buy

Sentiment : Strong Buy

Re: Internet Capital has a full ipo-pipeline (Not rated) 22-Apr-07 04:42 am Ready for an ipo or other monetarisation (sale): Creditex. The numbers are from the last presentation of Internet Capital

Business Description

• Leading position in the credit derivatives market with strong bank recognition

• First to launch E-trading and have gained significant traction in Europe

• T-Zero is being launched to address the processing needs of the derivatives industry

• Top 2 Market share in most of the macro products

• Will trade over $2 trillion notional

• CDS market continuing to grow at 50%+ per annum

• Net Income Positive

• Annualized revenue growth over 50% annually since January 2004

• 2006 Revenues at $135 Million

ICG Interest In Creditex

• 15% Ownership Interest

• Doug Alexander holds a board seat

Sentiment : Strong Buy

Re: Internet Capital has a full ipo-pipeline (Not rated) 26 second(s) ago Compare with Cbot, who had an offer of 9.9 billion. Revenues of Cbot a 4- or 5-fold of the the revenues of Creditex.

CBOT 1st-quarter profit increases

By ASHLEY M. HEHER

CBOT Holdings Inc., the holding company for the Chicago Board of Trade, said Thursday its first-quarter profit climbed 58 percent due to higher trading volume and increased average exchange fee rates.

The company, which is considering dueling acquisition offers from its crosstown rival Chicago Mercantile Exchange and Atlanta-based IntercontinentalExchange Inc., posted earnings of $55.4 million, or $1.05 per share. That's compared with $35.1 million, or 66 cents per share, a year ago.

Excluding $13 million in merger-related costs, net income for the January-March quarter was $68.4 million, or $1.29 per share.

"The positive momentum we built last year is carrying through into 2007, as we experience higher trading volume and continue to effectively manage expenses," Chief Executive Bernard Dan said in a statement.

Analysts polled by Thomson Financial were looking for a profit of $1.17 per share.

Text zur Anzeige gekürzt. Gesamtes Posting anzeigen...

Quarterly revenue at the financial exchange grew 34 percent to $187.7 million, falling short of Wall Street's estimate of $192.9 million. During the first quarter last year, CBOT had revenue of $140.1 million.

Chicago-based CBOT said sales were driven by record trading volume and higher average exchange fee rates.

Average daily volume for the quarter was 3.9 million contracts, up 24 percent from the prior-year period.

"All in all, there is little to complain about with BOT results and we expect the stock to react positively to the numbers," Bank of America analyst Christopher J. Allen wrote in a research note Thursday.

CBOT shareholders are scheduled to vote on the offer from Chicago Mercantile Exchange Holdings Inc. on July 9. The company also is reviewing ICE's unsolicited offer.

"The board and its special committee ... are carefully evaluating the ICE merger proposal," Dan said on a conference call with investors.

The ICE bid was said to be worth $9.9 billion when it was announced last month, or more than $1 billion more than the Merc's $8 billion-plus offer from October. Both totals fluctuate based on daily stock prices.

A Merc-CBOT combination would control 85 percent of the U.S. market for exchange-traded futures contracts, while a ICE-CBOT deal would account for about one-third.

The Chicago exchanges allow investors to bet on prices for stocks, metals, currencies, grains, bonds and other things without owning them by buying and selling contracts tied to the value of an underlying commodity or event.

CBOT shares fell $2.08, or 1.1 percent, to $192.42 Thursday on the New York Stock Exchange.

------

On the Net:

http://www.cbot.com

Sentiment : Strong Buy

That was quarterly numbers from Cbot. From Creditex we know about revenues from 135 million in 2006, maybe by the growth-rate of 50% about 180 million in 2007. The result is: The revenues of Cbot in a quarter are like revenues of Creditex in a year - that means the revenues of Cbot a four-fold of Crecdtex. And now listen: For Cbot exist an offer of 9.9 billion.

Aber selbst wenn Creditex nur einen Wert von einer Milliarde hätte ergäbe das für die 15% von Internet Capital einen Betrag von 150 Millionen, die auch nicht annähern im Kurs eingefangen sind. Von den 330 bis 375 Millionen, die sich bei einer Bewertung wie bei Cbot ergäben, wollen wir erst gar nicht reden, denn zusammen mit der Cash und Wertpapieren von 170 Millionen lägen wir dann schon weit über der momentanen gesamten Marktkapitalisierung von Internet Capital.

Internet Capital hält 70 Millionen Aktien von GoIndustry.

Das Management von GoIndustry versucht mit aller Gewalt und vielleicht sogar kriminellen Tricks den Kurs zu drücken. Geht z.B. der Kurs wie heute auf 24, wird sofort mit ein paar Miniorders ein Kurs von 21 angezeigt, obwohl Geld 23 und Brief 24 ist. In meinen Augen auch kriminell aufgemacht ist der letzte exzellente Geschäftsbericht. Es wird da nicht etwa von den von 30 auf 34 Millionen britischen Pfund gestiegenen Umsätzes berichtet - denn würden die Anleger ja merken, dass hier ein Unternehmen vorliegt, das einen Umsatz von 75 Millionen Euro vorliegt bzw. 100 Millionen Euro existiert. Dafür berichtet man über die Entwicklung des Rohgewinns, der von 16 auf 19 Millionen gestiegen ist. Beim Rohgewinn (direct profits) sind von den Umsätzen schon bestimmte Kosten abgezogen. Damit will man die Tatsache der vorhandenen 100 Millionen Umsatz und ein Kurs-Umsatzverhältnis verschleiern, das nur ein Zehntel von z.B. deutschen Internetbruchbuden wie beispielweise Abacho und anderen beträgt.

Good numbers of GoIndustry (Not rated) 27-Apr-07 09:49 am Important numbers:

CONSOLIDATED INCOME STATEMENT

In thousands of Pounds Notes Year ended

31 December 2006

Year ended

5 January 2006

Revenue 2 34,141 30,540

Cost of Sales (14,889) (14,622)

Direct profit 19,252 15,918

Da will doch Libuda tatsächlich weiterhin die Leser dieses Boards vollends auf den Leim führen.

Mal ausgehend von der Vorstellung, man hätte sich die von Libuda so vielgepriesene Internet Capital Aktie 2003 ins Depot gelegt, so würde ein aktueller Blick ausreichen um festzustellen, dass da außer Spesen nix gewesen ist.

Denn durch das Absinken des US – Dollar – Index seit dem Jahre 2002 um mehr als 30% ist die Performance dieser Aktie wohlwollend gesehen ein Nullsummenspiel.

Hätte man also im Jahre 2003, als die Aktienmärkte Fahrt aufnahmen, als der Dollar in etwa pari zum Euro stand, die Aktie von Internet Capital zu 7,50 Euro erworben, so dürfte einem beim Betrachten des aktuellen Kurses von 8,55 € (Nasdaq 11,74 $) die Augen feucht werden.

Unter der zusätzlichen Berücksichtigung von Transaktionskosten und dem Inflationsanteil wird somit auf den allerersten Blick klar und deutlich, dass diese Aktie in den letzten Jahren eine für europäischen Anleger fürwahr lausige Performance geboten hat.

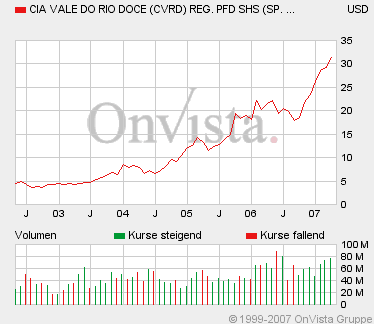

Gegenteilig dazu und begründet darin, dass Libuda auf diesem Board immer und immer wieder in den vergangenen Monaten das angebliche „Engültige und totale Abkacken der Rohstoffe“ posaunt hat, hier der einfach mal rausgegriffene 5-Jahres Chart von CVRD zur Sichtbarmachung von exorbitanten Kursgewinnen in den letzten Jahren und auch Monaten im Rohstoffbereich.

Also Libuda, um es mal in Deinem Jargon auszudrücken, höre einfach auf damit, weiterhin die Leser dieses Boards mit Deiner dümmlichen „Internet-Capital-kommt-groß-raus-macht-euch-reich-Verzockernummer“ zu verarschen. Wer Deinen Ausführungen hinsichtlich dieser Aktie gefolgt ist, hat im Prinzip an der hinter uns liegenden mehrjährigen Hausse nicht teilgenommen und somit eine Menge Geld verschenkt.

Angehängte Grafik:

CVRD.bmp

CVRD.bmp

Und es kommt noch besser: Libuda geht noch einmal von einer Verdoppelung seines Einsatzes bei Internet Capital in Dollar gerechnet aus. Und es gibt noch ein weiteres Zuckerl: Da sich langfristig Währungen immer auf die Kaufkraftparität zubewegen, kommt ein weiteres Plus von 15% bis 20% hinzu, wenn der Dollar auf Sicht von ein bis zwei Jahren auf 1,15 hinmarschiet - denn das ist nicht aufzuhalten. Es sei denn, dass sich Inflationsunterschiede zwischen den USA und Euroland massiv ausweiten, was ich nicht für sehr wahrscheinlich halte.

Statt über 7,409 Millionen britischer Pund Verlust in 2005 lag in 2006 ein Gewinn in Höhe 902.000 brititschen Pfund vor. Zu Dollarwerten kommt man durch die Multiplikation mit 2 und zu Eurowerten mit 1,5. Der Umsatz stieg von 30,54 Millionen britischen Pfund auf 34,141 Millionen britischen Pund, das sind immerhin knapp 70 Millionen US-Dollar oder etwa 52 Millionen Euro. Dafür ist auch den letzten Kursanstiegen die Bewertung mit ca. 100 Million Dollar oder etwa 75 Millionen Euro noch immer absurd niedrig. Inbesondere wenn man das mit deutschen Internetbruchbuden vergleicht, die tief in den roten Zahlen stecken. Einen Vergleich mit der Bruchbude Abacho, die mit dem 13,4-fachen ihres Umsatzes bewertet wird, habe ich ja auf dem anderen Board schon vorgenommen.

In thousands of Pounds Notes Year ended

31 December 2006

Year ended

5 January 2006

Revenue 2 34,141 30,540

Cost of Sales (14,889) (14,622)

Direct profit 19,252 15,918

Administrative expenses (18,213) (15,795)

Share based payments (517) (503)

Exceptional items:-

Actuarial gain / (loss) on defined benefit pension scheme 3 1,545 (457)

Exceptional operating charges 3 (349) (3,573)

Total administrative expenses (17,534) (20,328)

Profit/ (loss) from operating activities 1,718 (4,410)

Net finance costs (760) (980)

Exceptional finance costs 3 - (1,892)

Total net finance costs (760) (2,872)

Profit/ (loss) before income tax 958 (7,282)

Income tax expense 4 (56) (127)

Profit/ (loss) for the year 902 (7,409

"Set forth below is pro forma information relating to ICG’s current nine Core companies: Channel Intelligence, Freeborders, ICG Commerce, Investor Force, Marketron, Metastorm, StarCite, Vcommerce and WhiteFence. Our average ownership position in these nine companies was 45% at December 31, 2006. Please refer to the supplemental financial data at the end of this release for a reconciliation of such amounts to GAAP measures.

In the fourth quarter of 2006, aggregate pro forma revenue of ICG’s nine private Core companies grew 29% year-over-year, to $51.5 million from $40.0 million in the fourth quarter of 2005."

My estimate is, that the revenues of the nine core companies growth from 51.5 million in fourth quarter 2006 to 55 million in first quarter 2007.

In the three other quarters of 2007 my estimates for the revenues of the nine core companies are:

Second quarter = 59 Million

Third quarter = 63 million

Fourth quarter = 67 million.

An additon of the 55 million from the first quarter, the 59 million of the second quarter, the 63 million of the third quarter and 67 million of the fourth quarter has a result of 244 million. By an average in ownership of 45% the proportional revenues of the 9 core companies are 110 million.

Important are three of the other companies: Most important is Creditex, additional Emptoris and Anthem Venture.

Creditex will have revenues of about 170 million in 2007. By an ownership of 15% the proportional revenues in 2007 are 25.5 million.

Emptoris will have revenues of about 140 million in 2007. By an ownership of 5% the proportional revenues in 2007 are 7 million.

By Anthem Venture, an incubator is the estimate very difficult. In my estimate I chose proportional revenenus of Anthem Venture like the amount of Internet Capital = 150 million. By an ownership of 9% the proportional revenues are 10.5 million.

The revenues of other from the other private held companies are not important.

If I add the proportional revenues of nine core companies = 110 million and the three other proportional revenues (25.5 million + 7 million + 10.5 million = 43 million), the result = 153 proportional reveues from the private held core an other companies.

Sentiment : Strong Buy