Kidman Resource

Seite 1 von 15 Neuester Beitrag: 26.09.19 11:17 | ||||

| Eröffnet am: | 16.09.17 09:30 | von: Finanzm3344 | Anzahl Beiträge: | 363 |

| Neuester Beitrag: | 26.09.19 11:17 | von: Crazysurfer_. | Leser gesamt: | 153.298 |

| Forum: | Börse | Leser heute: | 22 | |

| Bewertet mit: | ||||

| Seite: < | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | ... 15 > | ||||

http://www.proactiveinvestors.com.au/companies/...qm-deal-180804.html

Optionen

| Boardmail an "Finanzm3344" |

Wertpapier: Kidman Resources |

As part of the joint venture, SQM will spend $110 million on a 50-percent stake in Mt Holland, the companies announced on Tuesday (September 12). Mt Holland will include a spodumene mine and lithium concentrator, and the integrated project will be centered on the Earl Grey hard-rock lithium deposit, located south of Southern Cross in Western Australia.

The outlook for the lithium market has never been stronger, and we view Mt Holland as the best undeveloped hard-rock lithium project in Australia, SQM Chief Executive Patricio de Solminihac said.

https://investingnews.com/daily/...-kidman-lithium-project-australia/

Optionen

| Boardmail an "Finanzm3344" |

Wertpapier: Kidman Resources |

Optionen

| Boardmail an "Finanzm3344" |

Wertpapier: Kidman Resources |

Kidman Resources Limited (ASX: KDR) is a fast-growing Australian resource company. Its flagship asset, is the Mt Holland Gold & Lithium Project located near Southern Cross, in the Archaean Forrestania Greenstone belt of WA. In December of 2016, Kidman delivered a Maiden Combined Mineral Resource of 128Mt at 1.44% Li2O for 1.84Mt lithium oxide (4.54Mt Lithium Carbonate Equivalent).

http://kidmanresources.com.au/

Optionen

| Boardmail an "Finanzm3344" |

Wertpapier: Kidman Resources |

Lithium Australia NL (ASX: LIT) ("das Unternehmen") hat es sich zum Ziel gesetzt, die weltweit größte Lithium ("Li")-Ressourcenbasis eines Unternehmens zu kontrollieren,

indem es Li-Carbonat in Batteriequalität aus der "vergessenen Li-Ressource" Li-Micas herstellt.

Um seine globale Li-Strategie voranzutreiben, hat das Unternehmen verschiedene strategische Beziehungen aufgebaut, die für die Gewinnung von Li-Carbonat aus Li-Micas auf kommerzieller Basis von entscheidender Bedeutung sind.

Zu den wichtigsten dieser Beziehungen gehört die Verbindung des Unternehmens mit der in Perth ansässigen Strategic Metallurgy Pty Ltd, die zur Entwicklung der innovativen Prozesstechnologie geführt hat, mit der das Unternehmen sein Ziel erreichen wird.

https://www.linkedin.com/company/3486097/

Optionen

| Boardmail an "Finanzm3344" |

Wertpapier: Kidman Resources |

Optionen

| Boardmail an "Finanzm3344" |

Wertpapier: Kidman Resources |

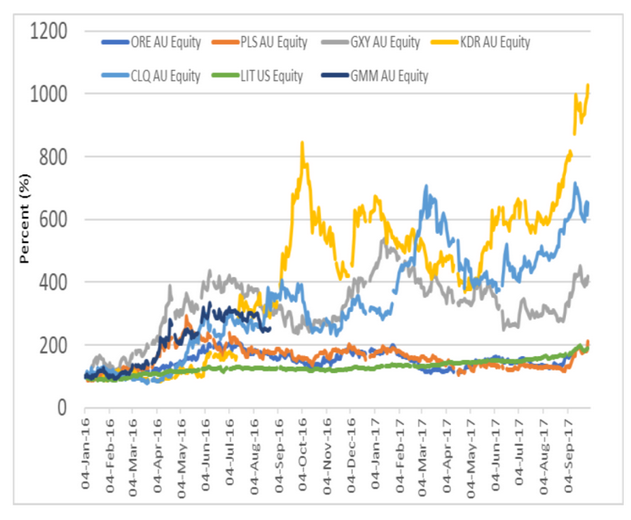

Angehängte Grafik:

kidman.png (verkleinert auf 80%)

kidman.png (verkleinert auf 80%)

Konnte bisher noch keine wesentlichen News erhaschen. Der SQM-Deal ist ja nun schon eingepreist. Was jemand mehr?

Bid an Euro-Börsen heute bei 0,68 EUR. Umsätze aber hierzulande noch lächerlich! Mal sehen, wann die Nächsten mit aufspringen. Der Aufwärtstrend ist jedenfalls intakt. Bisherige Korrekturen wurde schnell aufgekauft. Ich bin gespannt!

http://news.iguana2.com/macquaries/ASX/KDR/479316

Frage Eigentümerstruktur und Anteil Streubesitz der 338 Mio. Aktien?

Vllt. kennt sich ja hier jemand etwas besser aus?

Australian peer EV/Resource spodumene comparisons after the recent peer re rates per Oct. 6th 2017:

AJM:

Mcap $451M @ 28c fps (1614M fps, ~$13M cash, $140M debt facility)

Pilgangoora Ind/Inf resource 39.2Mt @ 1.02% Li2O (Prob reserve 30.1Mt @ 1.04% Li2O)

AJM value per resource Li2O tonne (~400,000t contained Li2O) = ~$1,127t

PLS:

Mcap $1,119M @ 76.5c fps (1467M fps, ~$87M cash, $130M debt facility)

Pilgangoora Ind/Inf resource 156.3Mt @ 1.25% Li2O (Prob reserve 69.8Mt @ 1.26% Li2O)

PLS value per resource Li2O tonne (~1.95Mt contained Li2O) = ~$573t

KDR:

Mcap $345M @ 99c fps (349M fps, $3M cash, $106M funds for mine development + $40M cash

upon SQM deal being executed/conditions ticked, no debt)

Mt Holland Li (KDR 50%) Ind/Inf resource 128Mt @ 1.44% Li2O + Au (KDR 100%) Ind/Inf resource >1M ozs

KDR value per resource Li2O tonne (50% of ~1.84Mt contained Li2O) = ~$375t

Currently and on the above basis KDR is still undervalued, IMO. On a peer on peer Australian average EV value @ $850t Li2O = $782M mcap or $2.24 per share potential. Either some of the Australian peers are overvalued on a simplistic EV/resource tonne value or KDR is still a screaming buy.

Source: hotcooper.com.au

Kidman: Ich denke Kurse unter 1,00 AUD sehen wir wohl nicht mehr! Zu wenig Seller an der ASX, wenngleich die Luft ab 1,20 dünner wird und erste Gewinnmitnahmen wahrscheinlich sind!

Zahlreiche News zum Förderstart in 2018 werden in 10.17 erwartet. Die dürften eher pushen, sofern es keine wesentlichen Marktkorrekturen gibt.

http://www.miningweekly.com/article/...lithium-concentrate-2017-10-03

Optionen

| Boardmail an "Finanzm3344" |

Wertpapier: Kidman Resources |

Kidman Resources shares hit an all-time high of $1.13 yesterday — but they could go up by another 50 per cent if one optimistic forecast is correct.

Analysts at Hartleys, a Perth-based stockbroker firm, reckon the WA-focussed gold explorer with a big side bet on lithium is heading for $1.71 largely because of its half stake in the potentially world-class Earl Grey joint venture with Chile’s lithium giant, SQM.

Not well understood by investors, the Earl Grey deal has been poorly explained by Kidman which won control of the lithium deposit about 100 km south of the WA wheatbelt town of Southern Cross after a bruising legal challenge from a rival explorer, Marindi Metals.

Within days of convincingly beating Marindi to the prize, Kidman (ASX:KDR) revealed its arrangement with SQM, a deal which some investors saw as a negative because it involved selling a 50 per cent stake in Earl Grey when they preferred 100 per cent.

Part of the promotion of the sale involved trying to convince the market that 50 per cent of a really big development was better than 100 per cent of a small mine.

But in doing that it also looked like any profits would be five years in the future rather than two years away.

Shares flatline after announcement

Confusion over the arrangement with SQM — which is one of the world’s biggest lithium producers — saw Kidman’s shares flatline at around 55c for weeks after it was announced.

That lack of positive response was despite the promise of becoming a half-owner of a project that could be much more than just another mine digging and delivering spodumene ore upgraded to a 6 per cent concentrate.

That’s because SQM has the technology to take lithium all the way to its hydroxide or carbonate form — the high-value material needed by battery makers.

Investors got a better understanding of what’s proposed last week when Kidman released a scoping study into Earl Grey with a clearer explanation that it was a two-stage project with the first stage being dig-and-deliver and the second, value-added stage, to follow.

Construction of the spodumene export phase could start in fewer than 12 months with first production roughly a year later.

Market still confused

Unfortunately for some investors in Kidman the initial reaction of the market was still confused — perhaps because of the lingering uncertainty over the project development process and the role of SQM and its Spanish speaking management which might have resulted in a “lost in translation” event, or because SQM has what might be called “interesting” lineage.

Whatever the explanation, what should have been a red-letter day for Kidman last Tuesday when the scoping study was released became a dog day with the stock falling 8 per cent from 97c to 89c.

Kidman did not regain its price before the release of the scoping study until Friday — perhaps with the aid of the Hartleys report.

The broker saw something that could have eluded investors — Kidman’s position as a fully-funded, 50 per cent partner in a major lithium project which will cost less to develop than first expected ($148 million versus $190 million), and deliver a 6 per cent spodumene concentrate for export at a cash cost of $US205 a tonne.

With the long-term price for the concentrate assume to be $US685/t, the first stage of Earl Grey should be handsomely profitable with the project generating an internal rate of return of 57 per cent — perhaps more because that long-term price estimate is well below the current spot market price for lithium concentrate.

Increased valuation

Hartleys, which is a financial adviser to Kidman and owns shares in the company, likes the idea of Kidman becoming involved in a lithium refinery because of the way it captures value lost to dig-and-deliver miners.

“We have increased our valuation [of Kidman] considerably by incorporating the refinery into our model,” the broker wrote in a report headed: ‘Scoping study very robust, Kidman is fully-funded’.

In fact, Hartleys has gone much further than simply tipping a future Kidman share price of $1.71.

The broker has run the numbers to demonstrate that the stock has a theoretical value of $4.87 using the spot-market price of lithium and after incorporating a 50 per cent stake in the proposed lithium refinery.

“Clearly, commodity price assumptions are very important,” Hartleys says in what must be one of the understatements of the year.

Whatever Hartley’s relationship with Kidman, there are four important points for investors to consider:

The company has not succeeded, yet, in providing a crystal-clear explanation of how the development of Earl Grey is likely to proceed, especially the timing of stage two, the refinery stage.

When that happens, the market will develop more comfort with a project that could become one of the world’s major sources of lithium.

SQM is not a well understood company, perhaps because it was once closely allied to Chile’s military dictator, Auguste Pinochet, who is the late father-in-law of SQM’s former chairman, Julio Ponce; and

As SQM shakes off the baggage of its unfortunate history it should become clearer to Kidman investors that they have a New York-listed partner which is a true global lithium leader keen to expand into Australia, bringing with it world’s best lithium processing technology

Qu: hotcopper.com.au

Aber das passt perfekt, weil ab 2018 auch die meisten Autohersteller ihre E-Autos auf dem Markt bringen - die Nachfrage nach Lithium wird wie flüssiges Gold gehandelt werden

Aber wir müssen noch Geduld haben... bis die Aktie zweistellig - dreistellig wird

Optionen

| Boardmail an "Finanzm3344" |

Wertpapier: Kidman Resources |

Alle anderen Minen, wer weiß wer dahinter steckt und ob sie je wirklich aus der Exploration je rauskommen???

Optionen

| Boardmail an "Finanzm3344" |

Wertpapier: Kidman Resources |

Dann doch lieber bei Kidman, in welches SQM selbst große Hoffnung steckt und investiert ist

https://www.automobil-produktion.de/hersteller/...um-sichern-366.html

Optionen

| Boardmail an "Finanzm3344" |

Wertpapier: Kidman Resources |

ganz einfach, weil es auch viele Fake-Lithium Aktien gibt und man deshalb unbedingt aufpassen muss, ob ein seriöser Gesellschafter in die die neue Mine sein Geld mit investiert hat

Und hier hat SQM 50% des Kapitals mit reingesteckt :-)

Deshalb wird es ganz sicher einen großen Deal mit Batterieherstellern geben... alleine schon durch die Verkaufskontakte von SQM

Optionen

| Boardmail an "Finanzm3344" |

Wertpapier: Kidman Resources |

Optionen

| Boardmail an "Finanzm3344" |

Wertpapier: Kidman Resources |