Ariad Pharmaceuticals-Neu

http://www.ariva.de/ariad_pharmaceuticals-aktie/..._sales?boerse_id=1

Optionen

| Boardmail an "Heron" |

Wertpapier: ARIAD Pharmaceuticals, |

Optionen

| Boardmail an "Heron" |

Wertpapier: ARIAD Pharmaceuticals, |

aber hier ein Unternehmen ein neues Präperat vermarktet, und der Kurs fällt.

Optionen

| Boardmail an "Heron" |

Wertpapier: ARIAD Pharmaceuticals, |

Warum PFE oder anderen vermeintlichen Freier top-Dollar für ARIA zahlen ....

Danke, Kinghana ... diese Art der Analyse ist wichtig für die Bewertung von ARIA wie für jeden potenziellen Erwerber davon .... Also, wenn sie in Aus 60M über $ 1B jährlich zu löschen ... wenn du auf der EU hinzufügen und die USA nicht in Frage ...

Einige grobe Rückseite des Umschlags stuff:

1 Die Bevölkerung von Australien wird auf 23.364.244 , wie der 30. Januar 2014

2 Die Europäische Union besteht derzeit aus 28 Ländern und hat eine Gesamtbevölkerung von knapp über 500 Millionen Bürgerinnen und Bürger ( 504456000 ) .

3 US Census Bureau Projekte Bevölkerung von 317,3 Millionen am Neujahrstag ... 2014

Also von der oben die Bevölkerung von der EU und den USA sind 35,17 X , dass der Bevölkerung von Aus ..

Also, nehmen Sie diese 1500 -Nummer und multipliziert es mit 35.17X .

Dies gibt Ihnen unterstellten 52.785 Patienten in den USA und der EU ..

$ 60M x 35.17 ....

Dies gibt 2110200000 ... oder

Mehr als $ 2.1B in Umsatz ...

Nur konservativ zu sein auf $ 1,4 Milliarden jährlich klopfen diese Umsatz ..

Weiter hat ARIA Aktien im Umlauf von 185.66M

Nun wird angenommen, eine 35% ige Nettogewinnmarge auf $ 1.4B ... das gibt 490000000 oder 490m

490M/185.66M Aktien aus ..

Gibt $ 2,63 eps ... setzen nur ein 15X auf mehrere dieser Summe ... gibt eine projizierte ARIA Aktienkurs von 39,58 $ mit einem Umsatz ... ww in der EU , NA und Aus ... Beachten Sie, dass SA, RSA und Japan sind NICHT inbegriffen

Glauben Sie mir ... PFE top-Dollar für ARIA zahlen ... könnte dieses Medikament riesigen ww Jahresumsatz generieren .. und Berger weiß, was ist, was wird und nicht auf die billige verkaufen ... andere Meinungen willkommen ... weniger

Optionen

| Boardmail an "Heron" |

Wertpapier: ARIAD Pharmaceuticals, |

http://investor.ariad.com/...ewsArticle&ID=1894128&highlight=

Optionen

| Boardmail an "Heron" |

Wertpapier: ARIAD Pharmaceuticals, |

BY Adam Feuerstein | 01/31/14 - 06:00 AM EST

The current investment thesis for Cell Therapeutics centers on pacritinib, an experimental Jak-2 inhibitor for myelofibrosis. In November, Cell Therapeutics signed a development and marketing partnership for pacritinib with Baxter (BAX_). A phase III study of pacritinib in myelofibrosis is underway, with a second phase III study expected to start shortly.

Nothing else in Cell Therapeutics' pipeline has any significant value. Assume all other pipeline drugs fail. I'd also assign minimal value to the approved lymphoma drug Pixuvri because Cell Therapeutics will struggle mightily to generate sales in Europe and the drug isn't ever likely to receive U.S. approval.

Today and into the future, Cell Therapeutics is pacritinib. Those who know me and my combative history with Cell Therapeutics may be shocked at the next statement, so sit down.

Pacritinib could be a real myelofibrosis drug.

Sorry if that freaks you out a little, but it's true.

Based on the phase II data presented to date, pacritinib appears to be a bit less effective than Incyte's (INCY_) Jakafi but perhaps better tolerated. Jakafi causes low platelet counts and anemia, often requiring myelofibrosis patients to discontinue treatment or lower the dose. For the same reason, doctors are hesitant to prescribe Jakafi to myelofibrosis patients with low platelets at baseline.

Pacritinib doesn't appear to have a negative effect on platelet counts, so the most reasonable (conservative) assumption to make is that the drug, if approved, could find a niche as a treatment for myelofibrosis patients with 1) baseline low platelets, or 2) who are intolerant to Jakafi.

Of course, this pacritinib profile needs to be confirmed in the ongoing phase III studies. Pacritinib is not without its own safety concerns, either. The drug causes relatively high rates of diarrhea, nausea and vomiting, based on the phase II data. Whether these gastrointestinal side effects adversely affect the drug's tolerability profile overall (and efficacy) is something to consider.

Incyte doesn't report fourth quarter and 2013 financial results until next month but it looks like Jakafi will generate roughly $400 million in worldwide sales. This is the drug's second full year on the market since launch in November 2011.

Street consensus for 2014 U.S. Jakafi sales is approximately $330 million. Add in another $200 million or so in ex-U.S. sales and call Jakafi a $500-$600 million drug next year.

What does this mean for pacritinib sales? Hard to say without any phase III data on hand, but a reasonable -- generous -- assumption would be $300 million in myelofibrosis sales two years post approval. In other words, pacritinib sales will be about half of Jakafi.

Why half? It's a nice, round number. Jakafi has a healthy head start and a better oncology drug marketer behind it (Novartis (NVS_)) than pacritinib will with Baxter. I don't believe pacritinib will demonstrate superiority to Jakafi so it's going to be more of a second-line myelofibrosis drug. Half may prove overly optimistic if Gilead Sciences (GILD_) secures approval for its myelofibrosis drug momelotinib. That's another wild card to keep in mind. And then there's Geron (GERN_) and Imetelstat -- don't forget those guys.

What's pacritinib sales of $300 million in 2017-2018 worth to Cell Therapeutics today? Using reasonable assumptions, risk adjustments and sales multiples, my NPV calculator spits out an enterprise value of $400 million.

Cell Therapeutics' enterprise value today: Just about $400 million.

Valuation is a subjective art, but I don't see a lot of fundamental upside in Cell Therapeutics from here. The stock will certainly be volatile around the release of pacritinib phase III data later this year, so trade accordingly.

My explanation of the Ariad Pharmaceuticals (ARIA_) short thesis countering the rumor of an imminent takeover by Eli Lilly (LLY_) or some other large pharmaceutical company caused the Hostile React-o-Meter to melt.

Most of the comments I received were along these lines: "Go [bleep] yourself you illiterate bald [bleep.]" I recommend reading the messages published under my Ariad blog post. Angry Ariad speculators have fallen prey to confirmation bias. You should also read Kid Dynamite's wise take on the subject.

A couple of readers did post intelligent comments supportive of the Ariad takeover thesis.

"Kong" offered multiple reasons why Ariad is a good buyout candidate. I'll post each one followed by a response.

Kong: Ariad is exactly the kind of small biotech that the Big Pharma are looking for to augment their pipelines and drug development programs.

Me: Perhaps, but the same can be said for many other small biotech companies. Those with promising platform technologies or drugs that are growing, not regressing, are more attractive than a company like Ariad.

Kong: A proven commercial tyrosine kinanse inhibitor drug for CML [Iclusig] that is probably the best in class and already bringing in revenues.

Me: Hmm. Iclusig is not best in class. The drug has been re-introduced to the market with a restricted label for a small portion of CML patients with the T315i mutation. Iclusig's revenue potential has shrunk considerably. The drug will never be used in the CML front-line setting, as previously hoped.

Kong: [Iclusig] looks very promising for GIST (refer to the melting liver mets presentation, available online.) Same drug may have potential in several other cancers -- just needs clinical trials to verify.

Me: Ariad may expand Iclusig's use to other cancers, but the drug's troublesome toxicity profile remains an overhang. There is plenty of competition in GIST.

Kong: Late phase clinical ALK Inhibitor drug [AP26113] showing excellent results on NSCLC including brain mets and low toxicity -- may be best in class.

Me: The efficacy of Ariad's ALK inhibitor AP26113 in lung cancer is no different from Novartis' LDK378. This week, Novartis announced that LDK378 was filed for U.S. approval as a treatment for ALK-positive lung cancer patients who no longer respond to Pfizer's (PFE_) Xalkori. Ariad is only just starting a pivotal study of AP26113, so the drug is far behind.

AP26113 might be differentiated by its ability to better treat lung cancer patients with brain metastases, but comparable data from LDK378 has never been published, so we don't know if AP26113 is unique in this regard.

There is also substantial competition from ALK inhibitors under development by Roche, Tesaro (TSRO_) and others.

Stock quotes in this article: CTIC, PVCT, ARIA, ORMP, GALE, INCY

http://www.thestreet.com/story/12286892/1/...ct-o-meter-meltdown.html

Optionen

| Boardmail an "RoStock" |

Wertpapier: ARIAD Pharmaceuticals, |

News releases

http://investor.ariad.com/...zhtml?c=118422&p=irol-news&nyo=0

Optionen

| Boardmail an "Heron" |

Wertpapier: ARIAD Pharmaceuticals, |

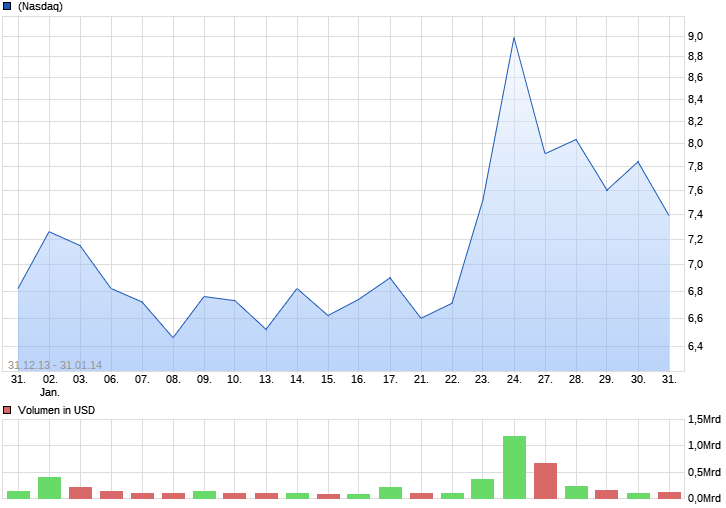

$7.67*0.17 negative 2.17%

*Delayed - data as of 01/31/2014 09:00

Read more: http://www.nasdaq.com/symbol/aria/premarket-chart#ixzz2rz7BtI48

Optionen

| Boardmail an "Heron" |

Wertpapier: ARIAD Pharmaceuticals, |

Optionen

| Boardmail an "Heron" |

Wertpapier: ARIAD Pharmaceuticals, |

Optionen

| Boardmail an "Heron" |

Wertpapier: ARIAD Pharmaceuticals, |

Optionen

| Boardmail an "Heron" |

Wertpapier: ARIAD Pharmaceuticals, |

Optionen

| Boardmail an "Heron" |

Wertpapier: ARIAD Pharmaceuticals, |

Optionen

| Boardmail an "Heron" |

Wertpapier: ARIAD Pharmaceuticals, |

http://investorshub.advfn.com/boards/read_msg.aspx?message_id=96635234

Optionen

| Boardmail an "Heron" |

Wertpapier: ARIAD Pharmaceuticals, |

Komisch, Ariad fällt.

Vor 1 Woche war das Volumen 20-fach Höher.

ca.1,17 Mrd. - 133.569.459 Shares

Optionen

| Boardmail an "Heron" |

Wertpapier: ARIAD Pharmaceuticals, |

Schlußkurs heut im Amiland $ 7,40-7,60 ?

24.01.14 17:11 #1760

Oder was meint Ihr? Schließlich haben wir heut Freitag.

Optionen

| Boardmail an "Heron" |

Wertpapier: ARIAD Pharmaceuticals, |

Optionen

| Boardmail an "Heron" |

Wertpapier: ARIAD Pharmaceuticals, |

Optionen

| Boardmail an "Heron" |

Wertpapier: ARIAD Pharmaceuticals, |

http://club.ino.com/trend/analysis/stock/ARIA/?mktcode=ihubtrenda

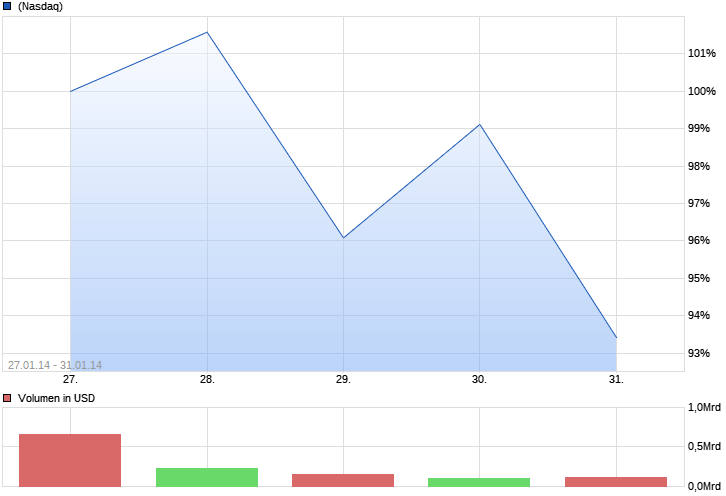

Vorbereitet für Sie am Freitag, 31. Januar 2014.

ARIAD Pharmaceuticals (NASDAQ: ARIA)

Smart Scan Chartanalyse zeigt eine Gegentrend-Rallye ist im Gange. Es zeigt auch, dass der aktuelle Abwärtstrend ändern könnte und Umzug in ein Trading-Range-Modus Sidelines.

Die Handelsdreiecke sind mit einem proprietären Algorithmus, der gewichteten Faktoren, die gehören zusammen erzeugt, sind aber nicht beschränkt auf - Preisänderung, prozentuale Veränderung, gleitende Durchschnitte, und neue Hochs / Tiefs. Der Markethandelsstrategie basiert auf den Dreiecken.

NASDAQ_ARIA

Öffnen Hoch Niedrig ARIA Preis Ändern

7,65 7,70 7,37 7,39 -0.45

Market Trade Dreiecke für ARIA

Der langfristige Trend hat sich seit dem 8. Oktober 2013 bei 16,95 gewesen

Der mittelfristige Trend ist seit dem 25. November 2013 bei 4,04 gewesen UP

Der kurzfristige Trend hat sich seit 31. Januar 2014 um 7.55 gewesen

Smart Scan-Analyse für ARIA

Basierend auf einer vordefinierten Formel für gewichtete Trend Chart-Analyse, hat ARIA -55 auf einer Skala von -100 (starke Abwärtstrend) bis +100 (starke Aufwärtstrend).

Optionen

| Boardmail an "Heron" |

Wertpapier: ARIAD Pharmaceuticals, |

Was ist der BEP

Der Break Even Point (BEP) ist der Punkt, an dem Erlös und Kosten einer Produktion (oder eines Produktes) gleich hoch sind und somit weder Verlust noch Gewinn erwirtschaftet wird.

Pipline Übersicht

http://www.ariad.com/pipeline

Wie aus der Pipline zu entnehmen ist, und allgemein bekannt ist, wird nur durch Inclusig Cash generiert.

Im Jahr 2013 wurde bisher von QI - QIII (9 Monate) ca. 37 Mill. $ generiert. Für das Gesamtjahr wird mit rund 60 Mill. $ gerechnet.

siehe unten

Income Statement

http://finance.yahoo.com/q/is?s=ARIA

Jetzt frag ich alle, ist der jetzige Kurs fair oder sollte er höher stehen?

Die Antwort sollte/kann sich jeder selbst beantworten.

Optionen

| Boardmail an "Heron" |

Wertpapier: ARIAD Pharmaceuticals, |

Es gibt wohl Berechnungs- Modelle aus dem Oktober die einen Kurs rechtfertigen würden von über 30$ bei einem erwirtschaften Einsatz von 600 Einheiten.

Sollten wir jetzt bei geschätzen Einheiten von 400-450 nur noch 7,30$ Wert sein ????

Selbst bei Zweitlinien Therapie mit eingeschränkten Patientenkreis und Halbierung würde dies einen Kurs um die 15$ rechtfertigen.

Derzeit wie ich ich schon mal angeführt habe, tappen „Alle“ im Dunkeln wie der Neustart angelaufen ist. Sobald hier eine Information veröffentlicht wird der Kurs wieder da hin laufen wo er hin kam.

Persönlich sehe die Kurse als Geschenk um weiter aufzustocken, aber das muss jeder für sich entscheiden. Man kann auch mit Fallenden Kursen Geld verdienen so wie es uns wieder die US Boys vormachen oder auch mit manchen sonderbaren Meinungswechsel hier zu Lande. ( sollte sich jemand angesprochen fühlen, so ist das rein Zufällig)

Nur zu Deiner Frage: 95% ALLER Biotech Unternehmen sind überbewertet man errechnet in Statistiken zukünftiges Marktpotenzial mit Erfolgsaussichten, Pipline mit entsprechenden Marktchancen,diese Berechnungen haben nicht mit Einspielungen mit Cash Generationen zu tun.

Auch ich kenne den den Feuerstein Report und Biotech Report, wo jetzt alles wie eine Schafherde nach plappern.

Nenne mir 1 Unternehmen das gutes Geld in der Branche verdient und ich nenne Dir 500 die Überbewertet sind und nach den Kriterien bewertet wurden.

Also ist die Agumentation recht schwammig was ich derzeit lese.

Das ist das 1x1 dieser Branche..........Zauberwort in der Biotechbrache +++Zukunftsaussichten