Absturz von Targacept

Seite 2 von 3 Neuester Beitrag: 25.04.21 13:12 | ||||

| Eröffnet am: | 08.11.11 16:02 | von: butzerle | Anzahl Beiträge: | 63 |

| Neuester Beitrag: | 25.04.21 13:12 | von: Ulrikenhtxa | Leser gesamt: | 13.513 |

| Forum: | Hot-Stocks | Leser heute: | 3 | |

| Bewertet mit: | ||||

| Seite: < 1 | | 3 > | ||||

Fast forward to Phase III, and the first of four Phase III studies looking at efficacy, Renaissance 3 (R3) was a bust. 624 European patients were recruited to receive standard therapy of SSRI and SNRI. After eight weeks of treatment, 295 patients who did not respond adequately were randomized to receive either a flexible dose of TC-5214 or placebo on background therapy. The dosage of TC-5214 was initially 2 mg/day and could be increased at the discretion of the investigator to 4 mg/day and 8 mg/day based on tolerability and therapeutic response.

So what happened in Phase III? How could a drug that was so promising in Phase II fail in Phase III? Several points need to be considered.

1. STUDY SITE: The Phase II trial was conducted in U.S. and (repeat and) India, not just India alone. The R3 was conducted in Europe. There are several cultural differences between the East and West that people conducting trials should be aware of. Indian patients are much more trusting than patients in the U.S. or Europe. Thus, even when told they could be getting placebo, they are liable to show a higher response rate than those in the West. In a highly subjective disease such as depression, where there are no objective measures, that can have a huge effect. But, as mentioned, the Phase II study was in U.S. AND India, not just India alone. Were there too many Indian patients that skewed the data in the Phase II study? Possible and I’m sure both companies have already evaluated that possibility. Looking at efficacy in just the U.S. patients of the Phase II study and comparing it to the Indian patients should have been done. If there was a huge difference, that would have been a red flag. If there was no difference, the answer lies elsewhere.

2. STUDY DESIGN: Both studies had an unusual “flexible design” rather than the standard parallel study design. The putative advantage of this study design is that it is supposed to give an answer with fewer patients. I have read several articles on this study design, but I’m still skeptical. I have yet to see a Phase III study, irrespective of the indication, that confirms the Phase II data of this design. I hope some reader who is better than me in statistics will comment on this below and educate U.S. all. Also in the design, were the inclusion and exclusion criteria the same in both studies? For example, in Phase II, only citalopram failures or partial responders were included whereas in the R3, failures could have been with any SSRI or SNRI. The populations, strictly speaking, are not the same.

3. MECHANISM OF ACTION: A single negative study, even if in Phase III, may not kill new mechanisms of action, but it will make it much harder to interest big pharma to go after novel targets. It will further decrease an already depressed CNS focus in big pharma, with many companies exiting this therapeutic area. For a small company with CNS focus, the job just got harder. An additional point about MOA – were there genetic differences that can explain the differences? Indians are genetically not that different from Caucasians, especially Germans (bet that surprises a lot of readers), but it should still be considered since this study was conducted in Poland, Baltic states, Finland, Czech Republic, France and Sweden in addition to Germany.

The other Phase III studies have already started. The data should be intriguing

MFG

Chali

Optionen

| Boardmail an "Chalifmann3" |

Wertpapier: Gyre Therapeutics Inc |

Optionen

| Boardmail an "butzerle" |

Wertpapier: Gyre Therapeutics Inc |

Optionen

| Boardmail an "lady luck" |

Wertpapier: Gyre Therapeutics Inc |

vielleicht funzt´s jetzt

Optionen

| Boardmail an "lady luck" |

Wertpapier: Gyre Therapeutics Inc |

Optionen

| Boardmail an "lady luck" |

Wertpapier: Gyre Therapeutics Inc |

besonders schön finde ich den passus "we find that the company has not been very careful in the management of its balance sheet".

Optionen

| Boardmail an "lady luck" |

Wertpapier: Gyre Therapeutics Inc |

Optionen

| Boardmail an "lady luck" |

Wertpapier: Gyre Therapeutics Inc |

Grummel

Optionen

| Boardmail an "Chalifmann3" |

Wertpapier: Gyre Therapeutics Inc |

Dazu einen 1,2 Milliarden Vermarktungsvertrag mit Astra Zeneca für das erst mal gefloppte TC-5214. Unter welchen Umständen Astra dort aussteigen kann, habe ich nicht in Erfahrung bringen können.

Mal angenommen, die weiteren Renaissance-Parallel-Studien floppen auch, dann wäre aufgrund der herausragenden Phase II -Ergebnisse auch ein anderes Design bzw. andere Auswahl des Probandenprofils denkbar.

Dazu noch eine Pipeline von weiteren Kandidaten.

Also, da gibt es weiß Gott zig Buden, die deutlich weniger zu bieten haben....

Optionen

| Boardmail an "butzerle" |

Wertpapier: Gyre Therapeutics Inc |

Optionen

| Boardmail an "butzerle" |

Wertpapier: Gyre Therapeutics Inc |

Da war das schon das Volumen in der Vorbörse...

Optionen

| Boardmail an "butzerle" |

Wertpapier: Gyre Therapeutics Inc |

MFG

Chali

Optionen

| Boardmail an "Chalifmann3" |

Wertpapier: Gyre Therapeutics Inc |

Die Erwartungshaltung für die kommenden Ergebnisse in 2012 dürften nun gering sein, da sollte bei weiteren schlechten Ergebnissen das Abwärtspotenzial begrenzt sein.

Targacept müsste wirklich viel Geld verbrennen, dass sie auf 80 Millionen absacken. Das droht unmittelbar nicht, allein schon wegen der Kohle von Astra Zeneca.

Aber klar ist auch, nur mit viel versprechenden News geht es da auch wieder aufwärts. Immerhin, am Dienstag nehmen sie an einer Analystenkonferenz teil. Da sie Cash bewahren wollen und Teilnahme an solchen Veranstaltungen auch was kostet, hoffe ich doch mal auf ermutigende Insindernews

http://finance.yahoo.com/news/...azard-bw-3581321513.html?x=0&l=1

Optionen

| Boardmail an "butzerle" |

Wertpapier: Gyre Therapeutics Inc |

http://finance.yahoo.com/news/...eca-Targacept-bw-4000131622.html?x=0

Optionen

| Boardmail an "butzerle" |

Wertpapier: Gyre Therapeutics Inc |

http://seekingalpha.com/article/...c-5214-disappointment?source=yahoo

Nun ist TC-5214 als großer Hoffnungsträger mehr oder weniger zerplatzt. Astra Zeneca hat den Wert der Patente schon mal um 50% gleich heute in einer Adhoc abgeschrieben

Optionen

| Boardmail an "butzerle" |

Wertpapier: Gyre Therapeutics Inc |

MFG

Chali

Optionen

| Boardmail an "Chalifmann3" |

Wertpapier: Gyre Therapeutics Inc |

Dieser Abschlag heute ist die blanke Panik, allerdings ist eine Rückkehr zu 8 Dollar nun sehr, sehr steinig. Da muss schon die Phase II, deren Ergebnisse Anfang des Jahres kommt, wieder ein Kracher sein.

Optionen

| Boardmail an "butzerle" |

Wertpapier: Gyre Therapeutics Inc |

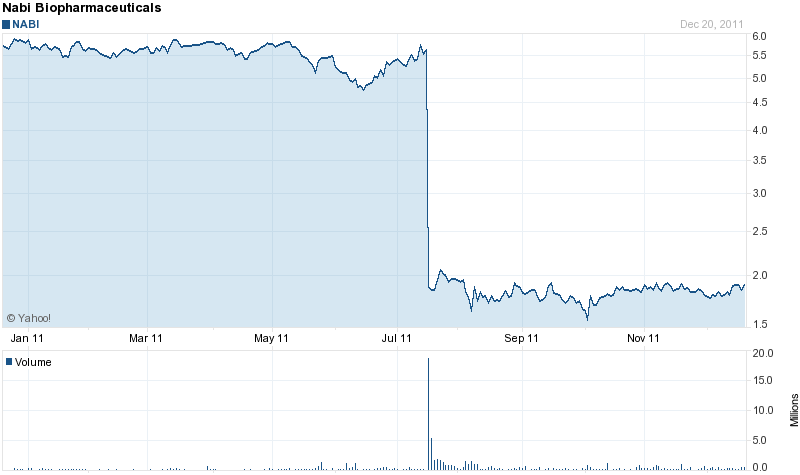

'Und so sieht es aus: Wenn die Technologie nix taugt ,wird TRGT auch noch auf unter 2 Dollar fallen,da nützen dir die 200 Mio.-cash garnüscht:

Hier der chart von NABI

Optionen

| Boardmail an "Chalifmann3" |

Wertpapier: Gyre Therapeutics Inc |

Angehängte Grafik:

z.png (verkleinert auf 63%)

z.png (verkleinert auf 63%)

Nur weil zwei Firmen mit ähnlichen Substanzen 2x Schiffbruch erlitten haben, ist das berhaupt kein Grund, dass Biotech auf Nikotinderivaten generell floppen muss.....

Generell ist es schon schlüssig. Raucher benötigen Nikotin als Glückssubstanz, also kann ein Derivat davon durchaus als Antidepressivum wirken....

Ich habe heute nachgekauft!

Optionen

| Boardmail an "butzerle" |

Wertpapier: Gyre Therapeutics Inc |

http://www.bizjournals.com/triad/news/2012/01/05/...ug.html?ana=yfcpc

Also, auch nach dem vermeintlichen Scheitern von TC-5214 glaubt der britische Pharmariese an die "Neuronal Nicotinic Receptors (NNR)"

Sind die, wenn man Chalifman glauben kann, blöd.

Die gute Nachricht ist aber auch, dass die Cash-Kuh nicht die Weide verlässt und weiterhin Targacept mit der Finanzierung versorgt - trotz Fehlschlag.....

Optionen

| Boardmail an "butzerle" |

Wertpapier: Gyre Therapeutics Inc |

The Bad News, In Brief

The failure of Targacept's TC-5214 got plenty of attention in late 2011; earlier studies had been quite encouraging and there was optimism that Targacept and partner AstraZeneca (NYSE: AZN) had a potential blockbuster on their hands with a very new approach to treating major depression. In marked contrast to earlier studies (including a Phase 2b study run in India), the pivotal REN 2 and REN 3 studies failed to show a clinical benefit.

There are still ongoing studies (notably the fixed-dose REN 4 and REN 5) with this drug in major depression, but nobody expects anything from them now. At best, any success in these remaining studies would confuse the heck out of scientists and biostatisticians and require at least another pivotal study.

This is not the only failure in Targacept's books, though. TC-5619 did show enough efficacy in ADHD for AstraZeneca to license the compound, though Targacept is giving it another shot in inattentive-predominant ADHD.

Still Addressing At Least Two Major Markets

The encouraging news for shareholders is that these weren't the only shots on goal the company had.

In addition to the inattentive ADHD indication, Targacept is investigating TC-5619 for use in treating what are called residual symptoms in schizophrenia. While plenty of people are aware of the “positive” symptoms of schizophrenia like hallucinations, delusions, and agitation, less attention is given to the “negative” symptoms like blunt affect, anhedonia, and emotional withdrawal.

Atypical antipsychotics are some of the best advances in the history of drug therapy, sparing many schizophrenia patients from being sedated into oblivion, and have produced blockbusters like Abilify (marketed in the U.S. by Bristol-Myers Squibb (NYSE: BMY), Lilly's (NYSE: LLY) Zyprexa, AstraZeneca's Seroquel and Johnson & Johnson's (NYSE: JNJ) Risperdal. That said, these drugs can have serious side-effects and they aren't often very effective in dealing with the “negative” symptoms of the disease, leaving a real unmet clinical need.

Targacept also has two drugs in trials for one of the holy grail's of biotechnology – Alzheimer's disease. AZD-3480 is already in a Phase 2 study comparing the drug with Aricept after an encouraging earlier Phase 2 study, and Targacept announced during the first week of January that AstraZeneca had elected to move AZD-1446 into a Phase 2 study in Alzheimer's as well, despite a prior unsuccessful trial in ADHD.

Although Alzheimer's has chewed up many biotechs and only a handful of drugs have made it to approval (Forest Labs' (NYSE: FRX) Namenda and Pfizer (NYSE:PFE)/Eisai's Aricept among them), it too is a multi-billion dollar opportunity for an effective drug.

And Two More After That...

Those aren't the only ongoing clinical programs at Targacept. The company also has its TC-6987 drug in Phase 2 studies in both asthma and diabetes. Data from both studies are expected at some point in the first half of 2012. This a very new approach to these diseases and likely a long-shot for the company, but the size of the asthma and diabetes markets is huge and it would likely not be hard to find interested parties to partner for pivotal studies if the Phase 2 data is strong enough.

Balancing Opportunity And Cost

While Targacept is in solid shape today from a cash perspective (management expected to end the year with about $240 million in cash), Phase 3 trials are famously expensive. Targacept certainly has the funds to wait to see the outcome of the schizophrenia trial and AstraZeneca will be funding those trials in Alzheimers.

If TC-5619 shows enough efficacy to merit a Phase 3 study and/or if TC-6987 likewise shows enough efficacy to lead to further trials in asthma or diabetes, the company could face some tough decisions. AstraZeneca would presumably be interested in TC-5619 for schizophrenia, and the company has certainly shown its willingness to stand by Targacept's therapy platform despite numerous clinical setbacks. Still, investors cannot completely rule out the possibility that the company may have to try to go it alone in one or more of these drugs and raise the funds to sponsor further clinical development.

Failure Isn't The End

Just a few months ago, it looked like Targacept may have held the keys to a valuable platform therapy based around nicotonic receptors. With another clinical failure in hand now, though, the Street has soured on this stock to the point where it believes management will only destroy value by pursuing additional studies.

That seems a bit extreme given AstraZeneca's apparent willingness to continue its relationship with the company. Admittedly, the cost of Phase 2 studies in Alzheimer's is modest relative to the huge potential of an effective drug, but it could have walked away entirely if it didn't believe the drugs had some chance to work. Likewise, there are reasons to worry about the company's patent estate (patents for TC-5619 and AZD-3840 start expiring at the end of the decade), but that hardly seems to be a topic of discussion today.

A Sharper Risk/Reward Trade-Off

Given the dismal history of clinical drug development in schizophrenia and Alzheimer's, it's hard to be optimistic about any of those opportunities. That said, a long-shot is not the same as no shot and Targacept at least bears watching until data on TC-5619 are available. Likewise, this stock is basically a binary outcome at this point – if schizophrenia and Alzheimer's indications work out, the stock is a multi-bagger from today's price, while more clinical failure (coupled with cash consumption) will push this close to worthless.

Targacept may not be the best risk-return tradeoff out there today, but the company is not as hopeless as a negative enterprise value would suggest

MFG

Chali

Optionen

| Boardmail an "Chalifmann3" |

Wertpapier: Gyre Therapeutics Inc |

Der anstehende Merger mit CBIO scheint der Aktie wohl einen Boden zu verleihen.

http://www.targacept.com/newsroom/...ment%20Company&newsyear=2015

Optionen

| Boardmail an "Rudini" |

Wertpapier: Gyre Therapeutics Inc |