ADX Energy (WKN: 875366): Millionenchance?????

Seite 392 von 495 Neuester Beitrag: 25.04.21 01:37 | ||||

| Eröffnet am: | 27.05.10 16:54 | von: DukeLondon8. | Anzahl Beiträge: | 13.36 |

| Neuester Beitrag: | 25.04.21 01:37 | von: Klaudialfbda | Leser gesamt: | 2.047.769 |

| Forum: | Hot-Stocks | Leser heute: | 675 | |

| Bewertet mit: | ||||

| Seite: < 1 | ... | 390 | 391 | | 393 | 394 | ... 495 > | ||||

http://www.ad-hoc-news.de/...idi-dhaher-mit-kurzer--/de/News/21994723

bayerber

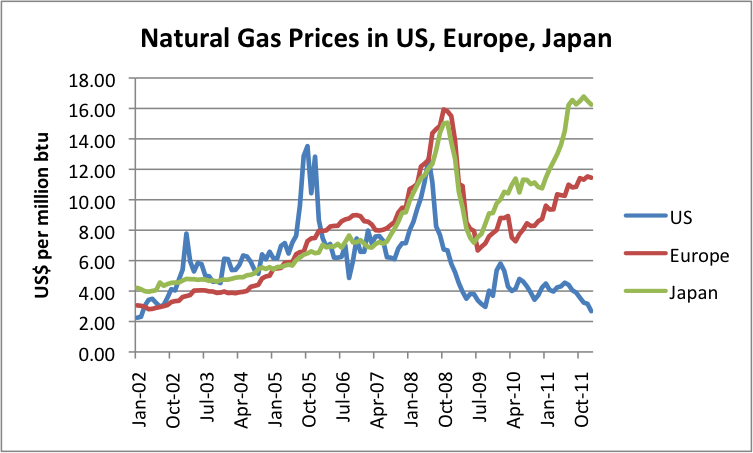

Aber ich hab was anderes interessantes gefunden. ADX hat die Offshore Lizenzen nach letzten Recherchen doch 2001/2002 o.ä. übernommen.

Da es dort unten hauptsächlich Gas gibt - werft mal einen Blick auf die Preisentwicklung

http://gailtheactuary.files.wordpress.com/2012/03/...europe-japan.png

{kind=link}

Der Erdgaspreis hat sich versechsfacht. Logisch dass Shell vor dem Millenium noch weniger Interesse daran hatte - da lagen ja die Preise noch niedriger!

Bis die USA nen Exportmarkt geschaffen haben blieben die Preise oben (mindestens 3 Jahre schätze ich). Das erhöht die Chance auf Joint Venture Partner für Dougga etc..

http://cb.iguana2.com/netwealth2/depth/adx

Beste Grüsse,

Oki-Wan 2.0

Ersstaunlich nur dat dem ADX Team die Sicherheit in der letzten Woche des Quartals so in dem Sinn kommt.

Die sollen mal langsam in die Pushen kommen und nicht wieder auf Verzögerungstaktiken umlenken.

Aber die Gaspreise stimmen :D

Verdammt, jetzt erst mal die Herzpillen einschmeissen

Schaut Euch mal die erste Seite vom Annual Report an, da war Gulfsands 600 Millionen wert: (2010 Ende des Jahres in etwa doppelter Kurswert)

http://www.gulfsands.com/i/pdf/2010ARA.pdf

Bei nur 50 mmboe Reserven und ner laufen Produktion von knapp 4mmboe

Zugegeben - ADX schafft im idealfall 1/3 aber dann hätten wir auch 30 Millionen im Jahr EBIT die wir ausgeben können. Nehmen wir Gulfsands KGV (6) von 2010 entspricht das einer ADX Bewertung von 180 Millionen. Also einem Kurs von 42 cent?

(180 Millionen : 30 Millionen aktuelle Marktkapitalisierung = 6 -> 6 * aktuellen Kurs)

Klingt wirklich zu gut um wahr zu sein.

aber bis der Kram in Produktion geht ...., falls das erwartete da ist ...

... Öl- und Erdgasschätze.

Ich stelle mal hier einen, wie ich finde durchaus interessanten Beitrag eines users "KoKo" auf HotCopper ein. Wem er zu lang ist, der kann ihn ja überspringen.

"With many good discoveries in onshore Tunisia mostly with over 1000 B/D and Tunsia having the highest exploration success rate in North Africa the testing and possible production of Hydrocarbons at SD should be well worth the wait .

Onshore Tunisia

published April 2010

The geological elements which are best developed in Libya and Algeria enter into Tunisia and cross the country. The Triassic, a prolific petroleum region in Algeria, enters into the southern tip of Tunisia. The Cretaceous trend for oil onshore is best developed in Tunisia. It is also found on the Algerian side of the border. Several oil and gas fields have been developed on the Tunisian side, with the main reservoirs in Triassic sandstones and subordinate reservoirs in Silurian clastics. Traps are found in faulted anticlines.

The Ghadames Basin straddling Algeria, Libya and Tunisia has become an interesting prospect for firms investing on the Tunisian side. Of particular interest to Tunisia-based operators is the TAGI sands play.

Big oil discoveries in TAGI sands on the Algerian side include fields in the prolific Berkine Basin, where large oil reserves have been proven. Agip in 1964 was the first foreign operator in Tunisia to find the TAGI horizon, having discovered and developed the billion-barrel field of el-Borma in those sands.

The series of Berkine fields and Qoubba discovered in the more recent years has also led new E&P operators in Tunisia, like EuroGas of Canada, to identify many targets on their blocks. TAGI reservoirs typically produce oil at high rates from relatively shallow depths giving low development costs.

The Ghadames Basin extending from Algeria has been relatively unexplored. Several companies are now drilling exploration wells on the Tunisian side, to the east of Algeria's Berkine Basin where large oil reserves have been found. Agip, active in Algeria and Libya, has made some oil and gas finds on the Tunisian side in a Silurian Fm called Acacus and a lower Fm called Tannezuft. Agip is an oil producer in Tunisia, Libya and Algeria.

(On the Tunisian side of the Berkine Basin, Agip's Hammouda-1 wildcat was in 1998 tested at 3,508 b/d of 42? API oil, 1,400 b/d of condensate and 14.2 MCF/d of gas in the Tannezuft Fm. In March 2001 Agip completed the drilling of Hammouda North-1 well at a depth of 3,507 metres. Two drill-steam tests were run in the Acacus sands and these flowed 3,873 b/d of oil and 2.9 MCF/day of gas.

Further finds have been made by Agip and other firms in the past six years and they now are producing. Agip in May 2005 had its Nour-1 in the Adam block in the south tested successfully for oil and gas. The well encountered an aggregate 48 metres of net oil and condensate pay and 10 metres of net gas pay in the Acacus and Tannezuft Fms, over a gross interval of about 300 metres at depths of 3,200-3,500 metres. The zones were equivalent to productive areas in the nearby Adam, Hawa and Dalia fields, discovered in the last eight years - see Part 2)

To the north of the country, a series of oilfields associated with the southern margin of the Atlas Mountains is found in a north-east and south-west trending basin. Reservoirs are in Cretaceous carbonates, mostly dolomites sourced by Cretaceous shales, and traps are anticlinal closures.

In the Cap Bon region, in the north-east, an interesting oil discovery was made in 1998 by Ecumed. The weld flowed at 3,007 b/d of 52? API oil and about 0.57 MCF/d of gas from a Fm called Bou Dabbous.

The Eocene has attracted the attention of foreign firms in recent years. This followed Marathon's June 1992 discovery of gas and condensate in the Zarat block in the south. In 90 metres of water about 106 km north-east of Ezzaouia oilfield, the first wildcat there flowed at around 17.5 MCF/d of gas and 1,498 b/d of condensates. The US company said the reservoir's depth was 8,629-8,842 ft and there was a column of over 97 metres in the Eocene el-Gueria Fm. The column had a 25-metre oil zone and more than 67 metres of gas/condensate pay.

Offshore prospects appear to be moderately promising, but more so for natural gas than for oil. The country has a broad continental shelf in the Gulfs of Gabes, Tunis and Hammamet. There is only a relatively narrow shelf to the north in the Mediterranean proper. It is in the broad shelf that several E&P companies have been interested.

A territorial settlement with Libya over the "7th

November" block in the Gulf of Gabes has led to creation of Joint Oil Co. (JOC) shared by Libya's NOC and ETAP. This is rich in oil and gas, being developed for JOC. The geological features of one structure there, Omar, are similar to Libya's nearby oilfield of el-Bouri which has a large gas cap.

The Pelagian Basin is a major petroleum province in Tunisia. It is proving to be more rich in natural gas than in oil. The basin straddles the coast and includes the Gulfs of Gabes and Hammamet, together with adjacent onshore areas. The hydrocarbon habitat is similar both onshore and offshore.

Candax of Canada in early 2006 made an interesting gas/condensate find with its Chaal-I in the onshore Pelagian Basin. The well tested the Ali Ben Khalifa prospect in the Late Triassic/Liassic Lower Nara Fm. Reserves of there were put at 60 BCF (2P) and 844 BCF.

Traps were produced by anticlinal folding and the source is believed to be Late Cretaceous to Early Tertiary shales. Reservoirs are provided by Cretaceous carbonates, both limestones and dolomites with rare sandstones, and Tertiary sandstones and limestones.

The offshore Amilcar block of BG, which contains the largest reserves of natural gas in Tunisia, lies in the Pelagian Basin. In this block are the Miskar field, the country's biggest producer of gas, and several other structures. Miskar produces from Cretaceous Fms called Abiod, R-1 and Bireno at an average depth of 10,500 ft. Miskar's gas reserves have been estimated at about 20 BCM.

The biggest among the other fields operated by BG is Hasdrubal. This field's reserves are estimated at 250-260 BCF of gas and 24.9m barrels of condensate, lying in a nummulitic limestone reservoir (see gmt15TunisFieldsApr12-10).

In the Gulf of Hammamet, an interesting oil discovery was made in January 1998 by Agip from a Miocene Fm called Umm Douil and a Paleocene Fm called el-Haria. This is part of the Pelagian Basin. Baraka-1 tested 4,353 b/d of 43? API oil and 4.48 MCF/d of gas at 2,670 metres.

In 1982, Marathon discovered an oil and gas reservoir in an Albrian-Cenomanian Fm called Zebbag, in 8 metres of water. This lies in the Djeffara Basin about 17 km south-east of Zarzis. The firms then estimated the field's recoverable reserves at 16m barrels of oil and condensates and more than 100 BCF of natural gas.

The onshore section of the Pelagian Basin, first explored by BG, is proving to be gas-prone as well. Preussag Energie of Germany (whose assets in Tunisia were in 2003 bought by OMV of Austria) discovered natural gas in several small structures in the Kerkennah Ouest Block B, which it acquired from BG in 1997.

The largest among these is the Chergui field, whose reservoir in a Mid-Eocene nummulitic limestone called "Reineche" has been reported to contain more than 70 BCF of recoverable reserves.

Another onshore Pelagian Basin find was made in early 1998 by Premier Oil of the UK. It tested 3,600 b/d of 42? API oil and 3.7 MCF/d of gas in carbonates of the Upper Cretaceous Bireno Fm at 3,350-3,423 metres. Premier also made a find in its appraisal well, el-Jem-2, which was tested at 245 b/d of condensate and 13 MCF/d of gas from an Upper Cretaceous Fm, Douleb.

Most prospective areas in Tunisia are gas-prone and oil reserves are not likely to be of the size found in Libya or Algeria. Oil exploration is maturing and prospects for major discoveries in the established areas are low.

As with Algeria and Morocco, there may be scope for a deep over-thrust play associated with the Atlas Mountains, but the area for such a play in Tunisia is much reduced.

There is exploration on more than 50 permits - onshore and offshore. There are 55 exploration and production sharing agreements (EPSAs) in effect in Tunisia. The number of companies involved in them and in new exploration is big, relative to the size and prospectivity of Tunisia. Exploration permits in force, mostly onshore, cover more than 150,000 sq km.

Tunisia boasts the highest exploration success rate in North Africa. Tunisia produced 2.9 BCM of natural gas in 2008, compared to the 86.5 BCM in Algeria. But international oil companies (IOCs) say while the volumes are low, Tunisia's favourable business climate compares well with the tougher environment in its neighbours. Ian Perks, CEO of BG Tunisia, a unit of London-listed gas major BG, has said: "It ticks all the boxes that companies are looking for in a place to invest. It's got political stability, good economic growth, sound economic policy, sanctity of contract, we have a very good relationship with all the stakeholders here".

In a sign of the increased interest, investment in Tunisian E&P has gone up from just over $100m in 2005 to $400m in 2008. The largest producer of gas in Tunisia, BG supplies 40% of local demand and it put its investment by the mid-2009 at more than $3bn. Agip of Italy, OMV of Austria and British energy services firm Petrofac Plc, which is a partner in an offshore concession, are among the firms operating in Tunisia. They are likely to be joined by others.

Tunisia's business-friendly climate contrasts with the challenges in Algeria and Libya, where IOCs face toughening terms and more assertive NOCs. Tunisian prospects under exploration or earmarked for exploration in the Sahara desert are part of the same geological structure as the world-class fields in Algeria and Libya. Craig McMahon, lead analyst for the Middle East and North Africa with consultancy Wood Mackenzie, says: "Tunisia actually boasts the highest exploration success rate in North Africa for the last 10 years".

ETAP is so confident about increasing production that it says from the end of 2012 it will become a net exporter of gas, pumping 4 MCM/d via a marine pipeline to Italy. Analysts say that growing domestic demand could eat up much of the increased output, leaving little for export. But selling gas in Tunisia is profitable too because prices are comparable to those on the international market. BG's Perks says: "For us, whether we export or whether we sell domestically, it's not the main driver for us, it's the economics that's the driver. We're very bullish about the economy here. It's been resilient to the financial crisis and so [we have] a growing domestic market, we're looking to supply".

Was denkt ihr?

Gruss Beauty

aber hoffe auch langsam das der kurs mal ein bisschen höher steigt...

Optionen

| Boardmail an "freitrinken" |

Wertpapier: ADX Energy Ltd |

Schön zu sehen bei Xstate:

http://www.xstate.com.au/files/files/451_Tunisia_2.jpg

{kind=link}

Seite 12 "Why the Pelagian Basin?":

http://www.xstate.com.au/files/files/...resentation_November_2011.pdf

Optionen

| Boardmail an "Japetus" |

Wertpapier: ADX Energy Ltd |

sein.

Aber man muß abwarten.

ADX hat ja nur Karten und 10 Mitarbeiter :D

Wenn erstmal 3 Quellen produzieren sieht das vlt. anders aus.

zunächst zu #9772: Nichts zu danken, ich finde es gut, wenn sich jemand näher mit den Lizenzen beschäftigt!

Nachtrag "Italian offshore":

GR.15.PU (Pantelleria)

Dort befinden sich u.a. ein Teil von Lambouka sowie Galliano und East Galliano. Der Status dieses Permits ist seit Juli 2008 übrigens "suspended", d.h. IMO darf dort momentan nicht ohne weiteres gebohrt werden (s. unten Vermerk "Sospensione decorso temporale"):

http://unmig.sviluppoeconomico.gov.it/unmig/.../dettaglio.asp?cod=667

Die Hintergründe dazu findest Du im Prospectus von Xstate auf S. 6 (unter "Title Risk") sowie ab S. 106ff im Detail.:

http://www.xstate.com.au/files/files/253_PROSPECTUS_FINAL_3_web.pdf

d 364 C.R-.AX

http://unmig.sviluppoeconomico.gov.it/unmig/...d=346&numerofasi=4

http://www.ad-hoc-news.de/...ionslizenz-in-italien--/de/News/22292193

Ob hier bereits gebohrt werden darf, weiß ich nicht, siehe den Vermerk auf der UNMIG-Seite ganz unten "Ricezione parere da Min. Ambiente: parere negativo".

d 363 C.R-.AX

http://unmig.sviluppoeconomico.gov.it/unmig/...d=345&numerofasi=4

Dieser ist noch nicht gewonnen, der Konkurrent ist hier wie kürzlich erwähnt Northern Peteroleum (d 362 C.R-.NP).

--------------------

Ich denke aber, dass sowieso Kerkouane für ADX im Vordergrund steht aufgrund der bereits angekündigten bzw. durchgeführten Projekte und den von Shell geerbten Bohrergebnissen. Außerdem hat mir in diesem Zusammenhang ein Satz im letzten Halbjahresbericht gefallen, mit dem ADX einen zusätzlichen (vielleicht den eigentlichen?) Grund nennt, warum es hinter den Italien-Permits her ist, und zwar ganz einfach den Schutz der Kerkouane Lagerstätten (hatte ich bereits erwähnt, aber hier der Vollständigkeit halber). In diesem Fall müsste dort also gar nicht unbedingt gebohrt werden, jedenfalls nicht kurzfristig.

"Since more acreage is being taken up by other companies in the area (i.e. Shell, Repsol, ENI) another reason for the application is to get protection acreage for prospects and leads which may extend from the Tunisian Kerkouane permit into neighbouring Italian waters.""

Optionen

| Boardmail an "Japetus" |

Wertpapier: ADX Energy Ltd |

Ich habe natürlich den Smiley gesehen, aber der Vollständigkeit halber sei angemerkt (Du wirst das wissen, aber vielleicht nicht jeder), dass es beim Wert einer Lizenz auch vor der ersten Produktion viele Zwischenstufen gibt.

aktuell:

Kerkouane: 3 Explorationsbohrungen durchgeführt, 3 Appraisal Projekte vor der Tür, "no dry holes" im Permit

westlich angrenzende Permits (Shell/NP/Repsol): erstmal mühsame Seismik und Exploration

Optionen

| Boardmail an "Japetus" |

Wertpapier: ADX Energy Ltd |

(Winstar ist onshore in Tunesien und Rumänien aktiv)

http://www.newswire.ca/en/story/941935/...provides-operational-update

"Tunisian natural gas sold for $14.75 per mcf or $88.50 per boe during Q4 2011. Winstar is indeed fortunate to have increased natural gas sales at a time when Tunisian natural gas prices are five to six times more lucrative than North American natural gas prices."

Ergebnis der 2 Bohrungen in Rumänien: 1 x positiv, 1 x negativ

Optionen

| Boardmail an "Japetus" |

Wertpapier: ADX Energy Ltd |

http://www.stockanalysis.com.au/samples/sample1.pdf

Recommendation: ADX is getting closer to a flow test of its Sidi Dhaher oil discovery in Tunisia. A flow of 200 barrels per day or more would be a good result.

The stock has a lot of stale bulls locked in to its register, so a strong rally is unlikely ahead of test results. [...]

Initial Target Price $ 0.17

--------------------------------------------------

IMO sind die Einschätzungen un Annahmen im realistischen Rahmen, obwohl man zu dem ein oder anderen Detail anderer Meinung sein könnte. Beispielsweise setzt der den Kerkouane Prospect (nicht Permit) aktuell mit Null an, obwohl Shell dort schon gebohrt und Gas gefunden hat (ähnlich Dougga).

Optionen

| Boardmail an "Japetus" |

Wertpapier: ADX Energy Ltd |

"If you go back to 12/01/2010

there was never any reconfirmation regading the LOI and signing of the rig back in 2010 same applies this time around.

IMO the footsteps of the big players (trading volumes) in both VIL and ADX clearly suggest these stocks are being acculumulated and set up , so weather the news comes tomorrow or next week it dosent matter because the intial test results will be the company maker .

cheers"

:cool:

Optionen

| Boardmail an "Schottenboerse" |

Wertpapier: ADX Energy Ltd |

-----------------------

Meinst Du das ernst?

Nun gut:

Der wesentliche Satz lautet (in Erwiderung auf genau die so geäußerte und von mir angesprochene Frage eines anderen users):

"Wenn Du zurückgehst auf den 12.01.2010 da war nie eine Bestätigung des LOI und das gleiche trifft auch jetzt zu.

Und weiter sieht der user "koko" im derzeitigen Handel von ADX und VIL ein Sammeln (einsammeln) und aufbauen (von Positionen), so daß (letztlich) egal ist, ob die news morgen oder nächste Woche kommen, denn die ersten Ergebnisse werden der Macher sein.

:o)

"Wenn Du zurückgehst auf den 12.01.2010 da war nie eine Bestätigung des LOI und das gleiche trifft auch jetzt zu.

Und weiter sieht der user "koko" im derzeitigen Handel von ADX und VIL ein Sammeln (einsammeln) und aufbauen (von Positionen), so daß (letztlich) egal ist, ob die news morgen oder nächste Woche kommen, denn die ersten Ergebnisse werden der Macher sein.

:o)