Mag auf vier Beinen

Seite 1 von 1 Neuester Beitrag: 12.12.08 11:19 | ||||

| Eröffnet am: | 08.04.08 19:15 | von: scioutnescio | Anzahl Beiträge: | 14 |

| Neuester Beitrag: | 12.12.08 11:19 | von: sturmhp | Leser gesamt: | 3.689 |

| Forum: | Hot-Stocks | Leser heute: | 1 | |

| Bewertet mit: | ||||

Mag ist eine kanadische Firma, die von einem Geologen gegründet wurde und im Kongo Geschäftsinteressen hat. Sie steht auf vier Beinen:

1.§Forstwirtschaft: 68 ha Eucalyptusplantage

2.§Energie: Beteiligung an einem Kraftwerk mit 1.424 MW und Planungen zum Bau von weiteren Wasserkraftwerken (250 und 100 MW)

3.§Pottasche: Der Markt dafür boomt. Es liegt eine abschließende Machbarkeitsstudie vor. Die Kapazität soll – zunächst – 600.000 t/Jahr betragen. Die abzubauenden Vorkommen an Pottasche enthalten auch

4.§Magnesium: Geplant ist der Bau einer Schmelze mit einer Kapazität von 72.000 t/Jahr.

Vorteile: Die Magnesiumschmelze wird mit Strom aus dem eigenen Kraftwerk versorgt und erlaubt daher eine kostengünstige Produktion. Nicht weit von dem Produktionsstandort befindet sich ein Tiefseehafen, der es erlaubt, die Produkte in die ganze Welt zu verschiffen.

Risiko: Zwar hat Mag erst vor kurzem eine Minenlizenz für 25 Jahre erhalten, doch ist bei einer Investitionsentscheidung das politische Risiko einzubeziehen.

http://www.magindustries.com

MagIndustries $80-million MagMinerals private placement

2008-04-04 17:16 ET - Private Placement

The TSX Venture Exchange has accepted for filing documentation pertaining to an offering of $80-million of securities in the capital of MagMinerals Potash Corp. (formerly MagMinerals Corp.), a wholly owned subsidiary of MagIndustries Corp.

The offering was structured as an offering of up to $100-million of common shares in a newly formed entity, MagMinerals Holdings Corp. (MagHoldings), at a price of $4 per share. MagHoldings then used the proceeds from the offering to immediately subscribe for $80-million of subscription receipts in the capital of MagMinerals at a price of $4 per subscription receipt. The agents in the offering include: Cormark Securities Inc., Paradigm Capital Inc., Desjardins Securities Inc., Jennings Capital Inc. and Ambrian Securities PLC. The agents will receive a cash commission of $4-million in connection with the offering. Following the closing of the offering, the company will hold an 83.3-per-cent interest in MagMinerals.

In connection with the offering, MagMinerals has agreed to use its best efforts to cause a liquidity event to occur before the date which is six months following the completion of the offering. Such liquidity event will involve the completion of a reorganization to, among other things, cause MagMinerals Inc. (Barbados) (the entity which holds the potash assets) to become a wholly owned subsidiary of MagMinerals; causing MagMinerals to become a reporting issuer in one or more provinces of Canada; and causing the common shares of MagMinerals to become listed on a Canadian exchange.

Optionen

| Boardmail an "Röttgen" |

Wertpapier: Magindustries |

1. Steve Martin von CrestStreet Asset Management am 18.4.08:

They refurbish and replace existing turbines in power plants and there is a power crisis in Africa right now. A bigger play is their massive potash deposit in the Congo. Recently spun out a small portion of that development into a private company. Raised money to start funding the first stage, which was about $480 million for the entire phase 1. They are left with $400 million, about $2 a share.

2. Ravi Sood von Lawrence Asset Management am 21.04.2008:

Potash play. A very large extremely profitable potash project in West Africa, Magminerals will be spun out as an independent company and will be valued about $4 per share giving a huge premium on today's price. Also have residual operations of forestry and power generation worth about $1.50. Gives close to $5.50/$6 per share of value. You won't capture all this as it will probably trade at discount, but it gives a huge upside from the current price.

Seit meiner Vorstellung vor knapp acht Wochen: 33% im Plus - und das wird sich fortsetzen!!!

Mining

MagIndustries Corp. announced Monday after market close that it had granted a total of 3,925,000 options to 19 officers, directors and employees of the company.

The options, which vest over the next 18 months, have an exercise price of C$3.28/share and expire in five years.

Desjardins Securities analyst Daniel Shteyn said the issue will probably be viewed positively if anything by investors.

"Given that the exercise price is fairly close to the current market price, we do not believe that the options will have a significantly dilutive impact on the float," he said in a note to clients.

"Furthermore, the options will serve to further align management and shareholder interests, which we see as an important positive given the company's reliance on key management personnel."

He left his "top pick" rating and $4 price target for MagIndustries shares unchanged.

Macquarie just came out with a research report today with a twelve month-target of $7 for MAA.

Das heißt: Obwohl es seit meiner Vorstellung vor 9 Wochen bereits um fast 50% nach oben gegangen ist, giebt es noch genug Luft!!!

Hinzu kommen zwei wichtige News aus den letzten Tagen. Zwei große Investoren kaufen sich zu 5$ / Aktie ein. Außerdem gibt es einen Abnahmevertrag für die 2011 beginnende Pottascheproduktion mit Ameropa. Beginnend 2011 mit 600000 Tonnen und Anstieg auf 1,2 Mio Tonnen bis 2013. Die Erlöse eines Jahres mit Vollproduktion entsprechen der aktuellen Marktkapitalisierung. Dazu kommen dann noch die Erlöse aus der Forstwirtschaft, Energieerzeugung und ab 2014 auch für Magnesium.

Übrigens wird sich in Kürze die gesellschaftsrechtliche Struktur von Mag ändern. Der Pottaschezweig wird ausgegründet und getrennt an der Börse notiert.

Bruce Campbell von Campbell and Lee Investment Management:

"Potash on the west coast of Africa. Will deliver potash to Brazil cheaper than anyone else can do it. It will be the world’s next new potash mine."

Nach einem Rücksetzer haben wir jetzt wieder absolute Kaufkurse. Die Ausgründung der Pottasche Gesellschaft ist zunächst gestoppt. Man hat keine Schulden und über 100 Mio cash. Daher soll gewartet werden bis der Markt sich etwas erholt hat.

MagIndustries Potash Unit Announces Updated 43-101 Reserve Report to Support Expanded Operations

10:52 AM ET, August 21, 2008

OTTAWA, ONTARIO, Aug 21, 2008 (Marketwire via COMTEX) -- MagIndustries Corp. ("MagIndustries" or the "Company") (MAA) is pleased to report that it has received an updated National Instrument 43-101 Technical Report entitled "Updated Reserve and Resource Estimate for MagMinerals Mengo Permit Area, Kouilou Region, Republic of Congo" (the "Technical Report") in respect of the property owned by its wholly-owned subsidiary MagMinerals Potash Corp. ("MagPotash"). The Technical Report updates the National Instrument 43-101 Technical Report filed on February 28, 2008 (see the Company's press release dated February 28, 2008).

The Technical Report is based on new rock mechanical modeling and a new solution mining cavern configuration. The Technical Report reports on the potash reserves and resources available to support MagPotash's planned Kouilou Potash mining and processing plant (the "Project") located 25km from the port city of Pointe Noire, Republic of Congo. The Project is intended to be built in two phases, Phase 1 and Phase 2, with each module specified at 600,000 tonnes per year (tpy) for a total capacity of 1.2 million tpy of potash.

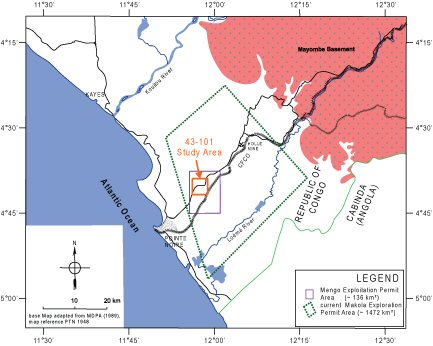

The new rock mechanical modeling allows a redefinition of the mineable Horizon 4 carnallitite layer resulting in a larger thickness available for mining and a hexagonal cavern configuration, which allows closer cavern spacing. These changes result in an increase of the previously stated reserves and resources. In the original report proven reserves were estimated to be 17.9 million tonnes of KCl with probable reserves estimated to be 3.1 million tonnes of KCl. The revised estimate of proven and probable reserves is 33.5 million tones of KCl which are sufficient to support 28 years of production at a rate of 600,000 tonnes of K60 potassium chloride (KCl) for the first two years of production and 1,200,000 tonnes of K60 KCl per year for the remaining 26 years. At a production rate of 600,000 tonnes of K60 per year the KCl reserves are adequate for a Project lifetime of 54 years. At a production rate of 1,200,000 tonnes of K60 per year the KCl reserves are adequate for a Project lifetime of 27 years. These reserves lie within a 25 square kilometer (sq km) portion of the 136 sq km Mengo Exploitation Permit which was granted in March 2008.

The study area represents approximately 18% of MagPotash's Mengo Exploitation Permit area of 136 sq km. MagPotash retains exclusive rights to a further 1,472 sq km of potentially developable area through the Makola Exploration Permit as outlined in the map below:

http://media3.marketwire.com/docs/map0821.jpg

{kind=link}

The potash deposits occur in the form of carnallitite rock which underlies most of the Makola Exploration Permit area. Carnallite is a magnesium-potassium-chloride mineral or a double-salt with the chemical formula KMgCl3-6H2O. The carnallitite rock occurs in multiple, horizontal horizons ranging in thickness from 0.5 meters ("m") to 24 m with an average content of about 70% carnallite. Four horizons, located between 400m and 800m below the surface, have been considered for commercial development.

The Technical Report is based on the results of 13 drill holes, 23 km of seismic surveys, as well as down-hole geophysical surveys completed by the Company. The Technical Report also incorporates economic data from a preliminary feasibility study completed by NOVOPRO Projects Inc. for Phase 2 of the Project, which assumes that Phase 2 will be in operation two years after the onset of Phase 1. The NOVOPRO study estimates a construction cost for Phase 2 of $423 million and that the economies of scale resulting from a doubling of production volume from 600,000 tpy to 1.2 million tpy will reduce operating costs per tonne from $83 per tonne for Phase 1 alone to $73 per tonne for the 1.2 million tpy Project.

Financial modeling based on a conservative potash price forecast published by Fertecon Limited in 2007 which implies an average net realized price to MagPotash of $464 per tonne for the first five years of the Project, and taking into account the financing costs (Phase 1 capital expenditures of US$ 723 million, financing and development cost of US$257 million and Phase 2 capital expenditures of US$423 million, with a debt to equity ratio for Phase 1 of 70:30) show that even for pessimistic cases the Project is capable of servicing its debt and breaking even.

For the base case, the Project's internal rate of return is estimated at 19% and at a discount rate of 12%, the net present value is estimated at US$1.2 billion. On the total Project costs of US$1.4 billion pay back is achieved in approximately six years, on the cumulative cash flows from operations from 2011 to 2016. Relative to the net cash flows from operations in 2014, assumed for the purposes of the Technical Report to be the first full year of production at 1.2 million tpy, pay back is approximately four years.

Ercosplan Ingenieurgesellschaft Geotechnik und Bergbau mbH ("Ercosplan") notes that further engineering studies and pre-production drilling will increase the database and therefore may contribute to a further upgrade of the reserve and resource base in support of future potash plant expansions. Ercosplan also note that the reserves and resources mentioned above are open in all directions.

Ercosplan, the company of the authors of the Technical Report, and formerly the engineering department of the East German Potash Enterprise, has over 50 years experience in the potash industry. Ercosplan was responsible for planning and supervising the core sampling program.

The authors of the Technical Report, Dr. Henry Rauche, EurGeol, and Dr. Sebastiaan van der Klauw, EurGeol, are the Qualified Persons with respect to the technical reporting and have reviewed and approved the contents of this press release.

die Bewertungen und nachrichten sind ja alle positiv !

Warum ist der Wertpapierkurs dann so am fallen ?

Jetzt kommt bestimmt die allegemeine Antwort, weil die Rohstoffpreise so rückläufig sind ...

Das ist aber alles halb so schlimm, weil keine Eile besteht.

und das Blatt wird sich wieder wenden.

Danke für die Antwort.

Für die Zukunft bin ich von Düngemittel, Potash, Kalisalz absolut überzeugt. Entsprechend glaube ich auch, dass Magindustires oder Western Potash wieder bessere Börsenzeiten sehen werden.

Für mich stellt sich nur die Frage des richtigen Zeitpunkts seinen Einstandskurs weiter zu senken und Nachkauforders zu tätigen, dabei muss man aber aufpassen nicht eine Übergewichtung von Rohstoff-Explorer-Werten im Depot zu bekommen.

Einen kurstechnischen Widerstand / Gegenraktion konnte ich die letzten 5 Tage nicht erkennen. Mal abwarten wo der Boden gebildet wird. Fällt der Kurs noch unter 1 Dollar ?

Hallo MagIndustries Aktionäre,

in dieser Diskussionsrunde ist es leider etwas ruhig geworden. Wahrscheinlich seid Ihr ebenfalls vom Kursverlauf geschockt

Wertpapier MAGINDUSTRIES Kurs am 09.12.2008:

An der Nasdaq wurden 100.850 Stück gehandelt Schlusskurs 0,14 $

An der Börse Frankfurt ist heute ein Geldkurs bei 0,088 € (15.000 Stk.), jedoch wie gewohnt kein Handel.

Seid Ihr von dem Explorer noch überzeugt ? Wo sind Eure Meinungen.

Auf langfristig steigende Kurse

Wertpapierkurs MagIndustries am 12.12.08

nasdaq 0,25$ , frakfurt 0,15 Geld +51%

Selbstverständlich wieder kein Handel in Deutschland. Wer in diesen Wert einsteigen will, sollte das über Trades an der amerikanischen Börse tun...